PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063658

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063658

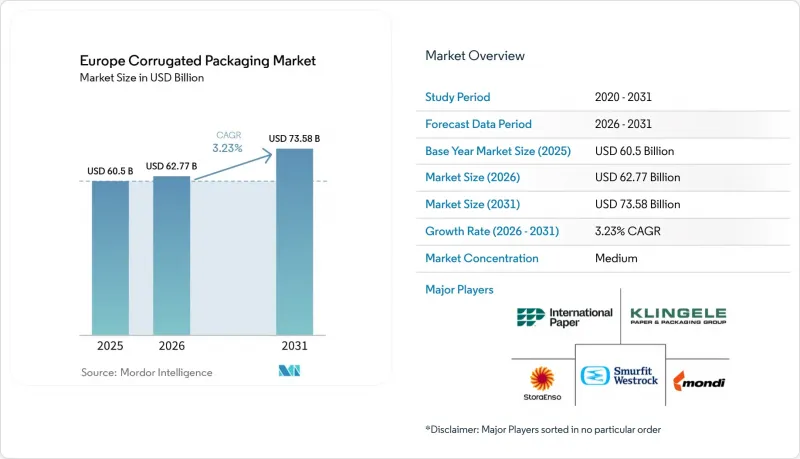

Europe Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe corrugated packaging market size is expected to increase from USD 60.50 billion in 2025 to USD 62.77 billion in 2026 and reach USD 73.58 billion by 2031, growing at a CAGR of 3.23% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, E Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Corrugated Packaging Market Trends and Insights

E-Commerce Boom Driving Demand for Lightweight Shipping Formats

Online retail platforms now specify lower-basis-weight boards that can withstand multiple automated sortation passes while reducing parcel freight costs. Amazon and Mondi released a 44-gram lighter mailer in 2025 that scales across millions of annual orders, saving thousands of tonnes of linerboard. Smurfit Westrock introduced a paper pallet wrap that substitutes plastic stretch film, widening corrugated's role in unit-load stabilization. Lightweight profiles from BHS Corrugated lower grammage by 20 g/m2 without sacrificing compression performance. Cost, sustainability, and Scope 3 reporting pressures make this driver most acute in the three largest e-commerce markets.

Shift Toward Plastic Substitution in FMCG Secondary Packaging

Fast-moving consumer goods owners are eliminating shrink wrap, trays, and clamshells as they work toward compliance with the EU Single-Use Plastics Directive. DS Smith reported that it would replace more than 1.2 billion plastic packs with fiber-based designs by 2025. Klingele's tie-up with Maistapack brought thermoformed fiber trays for fresh produce lines historically dominated by polystyrene. While demand lifts volume, Cepi cautioned in 2026 that accelerated substitution is draining recovered fibers to export markets, tightening domestic feedstock, and lifting input costs.

Rising Energy Costs Squeezing Mill Operating Margins

Natural-gas prices jumped above EUR 68/MWh (USD 73/MWh) in March 2026, with Italy paying EUR 111/MWh (USD 119/MWh) because of its gas-heavy power mix. Stora Enso's EUR 30 million (USD 32 million) Heinola upgrade cut emissions by 113,000 tCO2 yet required multi-year capex. Energy shocks compress margins fastest at independent mills that lack hedging or CHP capacity, prompting temporary curtailments in Southern Europe.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Recycled-Content Targets Under EU Rules

- Increasing Demand for Shelf-Ready Packaging in Retail Chains

- Volatility In Old Corrugated Container Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard owned 44.43% of Europe corrugated packaging market share in 2025. Widespread collection infrastructure and stable demand from grocery, beverage, and e-commerce channels anchor its dominance. Cepi's preliminary 2024 data showed containerboard output rising 4.3% year-on-year, confirming supply resilience. Virgin Kraft Linerboard is projected to grow at 5.62% annually through 2031, as pharmaceuticals and premium foods require higher wet-strength and greater barrier-coating compatibility. Semi-chemical fluting gains relevance in triple-wall export cartons, where stiffness per gram outweighs cost. The European corrugated packaging market for virgin grades will expand as converters mitigate fiber-quality variability.

Competitive pricing gaps between recycled and virgin sheets have narrowed due to volatile OCC costs, reducing the automatic cost preference for recycled liners. Mayr-Melnhof flagged import pressure from Asia and extra Scandinavian capacity as forces weighing on recycled margins. Regulatory recycled-content mandates still tilt purchasing toward post-consumer fibers, yet brands may accept virgin inputs when functional barriers or food-contact rules complicate recycling pathways. The material mix, therefore, hinges on end-use performance more than price alone, a nuance that reshapes procurement within the European corrugated packaging market.

B flute maintained 38.45% of overall volume in 2025, prized for its cushioning-to-weight balance. Brands are turning to E flute for direct-print retail-ready packs, propelling a 5.23% CAGR outlook through 2031. Digital white-ink launches eliminated historic print-quality gaps, making E flute viable for cosmetics and confectionery promotions. BHS Corrugated's eCom profile is optimized for E and F flute runs, reducing paper usage while maintaining compression strength.

C flute and A flute support heavy goods but lose share where freight space, carbon targets, and shelf density matter more than maximum stacking strength. Regulatory empty-space limits further favor thinner flutes because oversized containers risk retailer penalties. As retailers standardize shelf-ready dimensions, converters extend microflute capability to guarantee strength in compact forms, sustaining momentum for thin profiles in the Europe corrugated packaging market size forecasts.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- VPK Group NV

- Pro-Gest S.p.A.

- Klingele Papierwerke SE & Co. KG

- Model Holding AG

- Prinzhorn Holding GmbH

- Mayr-Melnhof Karton AG

- LEIPA Group GmbH

- Cartonajes International S.L.

- THIMM Group GmbH + Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom Driving Demand for Lightweight Shipping Formats

- 4.2.2 Shift Toward Plastic Substitution in FMCG Secondary Packaging

- 4.2.3 Increasing Demand for Shelf-Ready Packaging in Retail Chains

- 4.2.4 Automation of Corrugator Lines Enabling Shorter Lead-Times

- 4.2.5 Rapid Growth of Meal-Kit and Grocery Delivery Services

- 4.2.6 Mandatory Recycled-Content Targets Under EU Packaging and Packaging Waste Regulation

- 4.3 Market Restraints

- 4.3.1 Volatility In Old Corrugated Container (OCC) Prices

- 4.3.2 Rising Energy Costs Squeezing Mill Operating Margins

- 4.3.3 Competition From Reusable Plastic Crates in Fresh-Produce Logistics

- 4.3.4 Limited Corrugator Capacity Additions Due to Permitting Hurdles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

- 5.7 By Geography

- 5.7.1 Germany

- 5.7.2 France

- 5.7.3 United Kingdom

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Benelux

- 5.7.7 Nordic Countries

- 5.7.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi plc

- 6.4.3 International Paper Company

- 6.4.4 Stora Enso Oyj

- 6.4.5 Saica Group

- 6.4.6 VPK Group NV

- 6.4.7 Pro-Gest S.p.A.

- 6.4.8 Klingele Papierwerke SE & Co. KG

- 6.4.9 Model Holding AG

- 6.4.10 Prinzhorn Holding GmbH

- 6.4.11 Mayr-Melnhof Karton AG

- 6.4.12 LEIPA Group GmbH

- 6.4.13 Cartonajes International S.L.

- 6.4.14 THIMM Group GmbH + Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment