PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063744

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063744

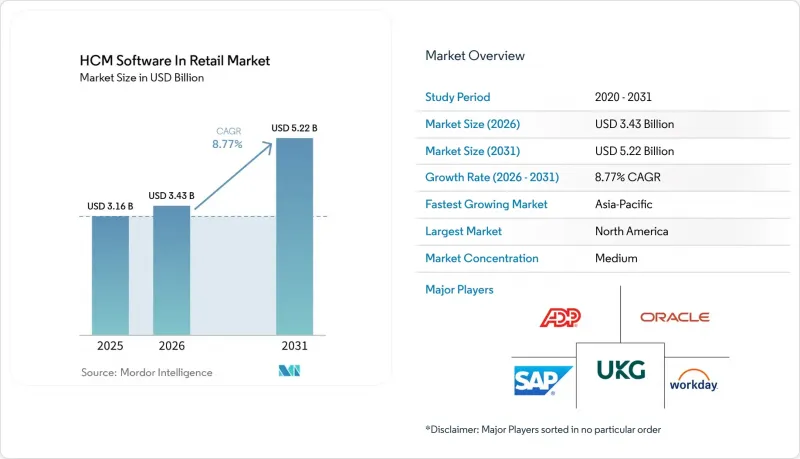

HCM Software In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hCM software in retail market size is expected to increase from USD 3.16 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.22 billion by 2031, growing at a CAGR of 8.77% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Function (Payroll Management, Workforce Management, Talent Management, Core HR, Learning and Development, and Other Functions), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Retail Market Trends and Insights

Rising Adoption of Cloud-Based HCM Suites

Retailers are shifting capex-heavy on-premises systems to subscription-based cloud suites to access quarterly feature drops, embedded analytics and automatic legislative updates. Workday cited faster retail deal cycles in its January 2026 commentary, attributing momentum to chains seeking mobile time tracking and compliance dashboards without onsite IT overhead. Private equity's USD 12.3 billion Dayforce take-private underscores investor conviction that multi-tenant SaaS economics outperform perpetual-license models. Mid-market adopters such as Belk unified payroll, benefits and scheduling across 300 stores after moving to Workday, eliminating legacy upgrade backlogs. Cloud vendors also shoulder liability for overtime and data-residency rules, an advantage as Hong Kong's "468" overtime regime and the EU Pay Transparency Directive come online in 2026.

Growing Focus on Mobile-First Self-Service HR Applications

Smartphone apps are shrinking manager-mediated workflows by letting associates swap shifts, update availability and view pay slips on demand. Sona's 2025 rollouts saved between 0.8%-4.0% of total payroll and returned 40 manager hours per week previously lost to manual schedule changes. Legion recorded 88% weekly active usage among frontline staff, cutting attrition by one-third thanks to real-time transparency. Geofenced clock-ins and biometric validation in isolved and Darwinbox apps curb time theft and support audit-ready attendance logs. Adoption trends skew toward Asia-Pacific, where CARSOME deployed Darwinbox's mobile payroll across 3,000 staff in four countries by February 2026.

Data Privacy and Cybersecurity Risks in Employee Information Systems

Employee records house social security numbers, pay data and health details prized by cybercriminals. Workday's August 2025 breach forced emergency patches across retail clients and reminded boards that HCM platforms sit on some of the most regulated personal data. GDPR fines can reach 4% of global turnover, so retailers operating in Europe now require vendors to store data within EU borders and document every transfer. The American Bar Association warns that adversarial inputs can manipulate AI screening bots, exposing companies to both hacking events and civil-rights suits in one incident.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use of AI-Driven Workforce Analytics

- Escalating Compliance Complexity Across Multi-State Retail Jurisdictions

- High Cost and Complexity of Migrating Legacy HR Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are expanding at an 11.01% CAGR through 2031, outpacing software's dominant 66.42% share in 2025. The HCM software in retail market size for services reflects the reality that platform subscriptions only launch the journey; localization, testing and ongoing regulatory tuning now drive spend. Consulting majors such as Accenture, Deloitte and PwC integrate HCM rollouts into wider digital transformations, while boutique integrators specialize in statutory payroll for markets like Indonesia and Mexico. Software remains sticky because payroll engines are the system of record, yet functionality converges fast, pushing value creation into advisory and optimization layers. Rolling Arrays' April 2026 commentary stressed that Southeast Asian clients judge providers on post-go-live discipline, not feature parity.

For retailers spanning 10-plus countries, services partners juggle localized tax tables, union rules and language packs, evolving into managed-service models that outsource payroll closing and compliance audits. IDC data show 60% of Asia-Pacific enterprises face operational disruption whenever regulators tweak labor codes, making SLA-backed support indispensable. Consequently, the HCM software in retail market increasingly values vendors able to package technology with regional service benches, a trend expected to deepen as EU pay-equity reports and U.S. fair-workweek laws proliferate.

Hybrid deployments are projected to grow at a 10.67% CAGR, eclipsing pure-cloud's early glamour by reconciling modern talent tools with entrenched payroll databases. Many chains keep SAP or Lawson payroll on-prem but layer Oracle Recruiting, SuccessFactors Learning or Workday Skills Cloud on top, routing data via integration hubs that demand rigorous end-to-end testing. The HCM software in retail market share for cloud still leads at 54.11% in 2025 because SaaS eliminates patching and eases store roll-outs, yet ROI can erode when deeply customized overtime logic must be rebuilt on a vanilla SaaS stack.

Retailers weighing their journey assess whether workforce management is a differentiator or utility. If differentiator, they accept change costs for best-of-breed suites. If utility, they opt for core-hybrid bridges like SAP's H4S4 that preserve payroll DNA while adding modern UX. Accenture cautions that hybrids require twice the test effort, as workflows cross system boundaries in every pay cycle. Still, this path lets risk-averse CFOs stage spend and upskill HR teams gradually, sustaining momentum without payroll failure headlines.

Geography Analysis

North America retained 38.22% of global revenue in 2025 due to sophisticated labor codes and early AI adoption. U.S. retailers grapple with 50 state wage laws plus city-level predictive scheduling, making compliance automation a board concern. Vendors respond with geo-coded rules engines and wage-theft alerts, features now standard in the HCM software in retail market. Algorithmic bias lawsuits also germinate here, injecting demand for explainable AI and fairness dashboards.

Asia-Pacific is the fastest riser at a 10.45% CAGR. India's organized retail booms alongside Southeast Asia's mobile-first workforce, while Chinese chains weave HCM directly into social-commerce and instant-delivery apps. ETHRWorld data show 65% of HR leaders in the region will boost AI budgets in 2026, yet only 11% feel fully prepared, opening doors for services partners. Government digitization pushes, such as Singapore's Digital Workforce initiative, further accelerate cloud HCM uptake.

Europe's growth rides on rule changes instead of store count expansion. The EU Pay Transparency Directive effective June 2026 forces every retailer above 100 employees to publish wage structures and justify gender pay gaps, a catalyst pushing the HCM software in retail market size upward as firms upgrade reporting pipelines. GDPR's data-residency demands splinter vendor choices, favoring platforms with EU-hosted data centers. South America, the Middle East and Africa contribute smaller shares but show spotty high growth in urban corridors where international franchises replicate North American compliance playbooks.

- Automatic Data Processing, Inc.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Ramco Systems Limited

- PeopleFluent, Inc.

- Cegid Group SA

- The Sage Group plc

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Paycor, Inc.

- Deel Inc.

- TriNet Zenefits, Inc.

- SumTotal Systems, LLC

- Paychex, Inc.

- Namely, Inc.

- SmartRecruiters, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud-Based HCM Suites

- 4.2.2 Growing Focus on Mobile-First Self-Service HR Applications

- 4.2.3 Increasing Use of AI-Driven Workforce Analytics

- 4.2.4 Escalating Compliance Complexity Across Multi-State Retail Jurisdictions

- 4.2.5 Surge in Micro-Fulfillment Retail Formats Requiring Agile Labor Scheduling

- 4.2.6 Integration of HCM with Point-of-Sale Platforms Enhancing Store Productivity

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Risks in Employee Information Systems

- 4.3.2 High Cost and Complexity of Migrating Legacy HR Systems

- 4.3.3 Algorithmic Bias Litigation Risk in AI Recruiting Tools for Retail

- 4.3.4 Seasonal Workforce Volatility Undermining ROI on Full-Suite HCM Investments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Function

- 5.4.1 Payroll Management

- 5.4.2 Workforce Management

- 5.4.3 Talent Management

- 5.4.4 Core HR

- 5.4.5 Learning and Development

- 5.4.6 Other Functions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Workday, Inc.

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Paycom Software, Inc.

- 6.4.8 Cornerstone OnDemand, Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Ramco Systems Limited

- 6.4.11 PeopleFluent, Inc.

- 6.4.12 Cegid Group SA

- 6.4.13 The Sage Group plc

- 6.4.14 Gusto, Inc.

- 6.4.15 Rippling People Center Inc.

- 6.4.16 HiBob Ltd.

- 6.4.17 Darwinbox Digital Solutions Private Limited

- 6.4.18 Paycor, Inc.

- 6.4.19 Deel Inc.

- 6.4.20 TriNet Zenefits, Inc.

- 6.4.21 SumTotal Systems, LLC

- 6.4.22 Paychex, Inc.

- 6.4.23 Namely, Inc.

- 6.4.24 SmartRecruiters, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment