PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064512

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064512

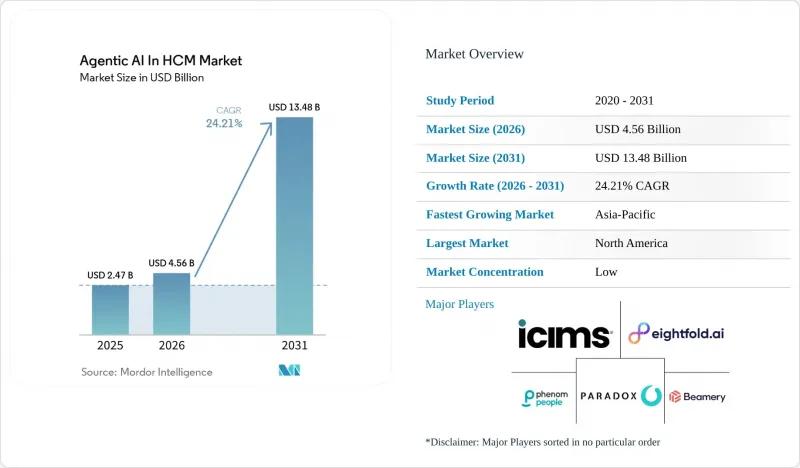

Agentic AI In HCM - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agentic AI in the HCM market size is expected to grow from USD 2.47 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 13.48 billion by 2031 at 24.21% CAGR over 2026-2031.

This report is Segmented by Component (Agentic AI Platforms and Orchestration Engines, and More), Function (Recruiting and Candidate Sourcing, More), Deployment Model (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In HCM Market Trends and Insights

Rising Labor Scarcity in High-Skill and Frontline Hiring

Persistent labor scarcity is pushing the agentic AI in the HCM market toward faster adoption because manual recruiting teams cannot keep pace with the volume and speed now required across frontline and specialized roles. U.S. JOLTS data showed 7.4 million job openings in December 2025, with openings-to-hire ratios in healthcare, manufacturing, and logistics still above pre-pandemic norms, signaling sustained hiring pressure rather than a short-term disruption. Companies also reported that unfilled U.S. vacancies stood at 4.5% of total labor demand in February 2025, while the hiring rate fell to a decade-low of 3.3% in December 2025, pointing to a structural mismatch in labor supply. This pressure matters because frontline employees account for a large share of the global workforce, and replacement costs per worker still range from USD 3,000 to USD 5,000 before productivity losses are counted. iCIMS reported in March 2026 that customers using Frontline AI achieved up to 75% lower time-to-fill and up to 10 times more hires per recruiter, which strengthens the business case for conversational sourcing agents in high-volume roles. The longer-term pull on the agentic AI in the HCM market is reinforced by demographic decline in working-age populations across mature economies, which makes faster hiring capacity more important to workforce continuity.

Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount

The agentic AI in the HCM market is also being driven by tighter cost discipline, since HR teams are being asked to improve output without expanding headcount. BCG reported in February 2026 that organizations applying AI in targeted HR workflows recorded 20-30% efficiency gains, and a GPT-based manager review tool cut review-writing time by 45% while improving review quality by 22% with 90% user satisfaction. Payroll administration places the same pressure on finances, with research indicating that employers lose 2-4% of total labor spend to payroll leakage, and that even a 1% loss can equal USD 15 million annually for a large employer. IBM's AskHR program showed that when agentic support is built on standardized workflows, HR teams can centralize service through a single entry point while reaching a 94% containment rate and cutting HR operating costs by 40% over 4 years. That model matters because McKinsey found in 2025 that only 18% of organizations with more than 1,000 employees used specialized HR shared services centers, leaving a significant process gap for software-led productivity gains. As a result, the agentic AI in the HCM market is increasingly tied to measurable labor efficiency rather than experimental automation budgets.

Data Privacy, Cross-Border Data Transfer, And AI Governance Burden

Compliance remains the clearest drag on the agentic AI in the HCM market because HR decisions touch highly sensitive data and often fall into higher-risk regulatory categories. The EU AI Act, Regulation (EU) 2024/1689, entered into force on August 1, 2024, and classified recruitment screening, candidate ranking, performance monitoring, and task allocation systems as high risk under Annex III. The framework requires conformity assessments, use-log retention, impact reviews, and worker-representative consultation, which increase costs and slow deployment of agentic AI in the HCM market. In the United Kingdom, the Information Commissioner's Office said in March 2026 that AI hiring tools without genuine human review can breach legal standards, and it warned that simple rubber-stamping does not qualify as meaningful oversight. Research in January 2026 showed that 77% of U.S. leaders cited data privacy as a top enterprise risk in the fourth quarter of 2025, up from 53% at the start of the year, which shows how governance concerns now shape buying criteria as much as functionality. This means the agentic AI in the HCM market will continue to expand, but vendors will need stronger localization, auditability, and oversight features to convert demand into deployed revenue.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Always-on Employee Self-service and HR Case Deflection

- Shift Toward Skills-Based Talent Decisions and Internal Mobility

- Integration Complexity Across Legacy HCM, Payroll, And Identity Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agentic AI platforms and orchestration engines accounted for 36.47% of the component segment in 2025, making them the largest component category in the agentic AI in HCM market. This leadership reflected the enterprise's preference to secure governance, routing, policy control, and escalation logic before expanding the number of live agents. These platforms gave buyers a way to manage task decomposition, human checkpoints, and identity control across recruiting, HR service, payroll, and mobility workflows. That foundation mattered because many deployments in 2025 and 2026 focused first on reducing execution risk rather than maximizing agent volume. The component mix, therefore, showed that infrastructure confidence came before broader expansion of use cases in the agentic AI market in the HCM market.

AI agents and workflow applications are projected to grow at a 27.39% CAGR from 2026 to 2031, making them the fastest-growing component segment. This phase marks the next step for agentic AI in the HCM market, where enterprises that built orchestration capacity in 2024 and 2025 are now filling it with task-specific agents for interviewing, policy navigation, payroll exception review, and internal mobility. Research in February 2026 showed that staffing firms using AI were 4 times more likely to outperform peers, while 55% said AI screening improved KPIs by more than 25%, and 46% achieved a 50% or greater reduction in screening time. Services remain relevant because large, multi-system deployments still require implementation support, workflow redesign, and ongoing tuning. Managed AI services are also gaining traction, as buyers want the benefits of agentic AI in the HCM industry without building deep internal AI operations teams. This leaves the component structure with a clear pattern where platforms establish control, applications drive scaling, and services support long-tail deployment complexity.

Workforce planning and analytics accounted for 22.83% of the market in 2025, making it the largest functional segment in the agentic AI HCM market. That position reflected the need for real-time labor allocation, budget visibility, and scenario planning amid tight hiring conditions and changing skill demand. The agentic AI in the HCM market size in this function benefited from executive demand for tools that connect workforce decisions more directly to financial outcomes. Only 12% of U.S. HR leaders engaged in workforce planning with a 3-year or longer horizon, while 73% remained focused solely on operational planning. AI-driven workforce planning launched in 2026 to link headcount and labor decisions to ERP and contingent workforce data, supporting stronger demand for analytics-centered automation. In practice, this function became the control room for the agentic AI in the HCM market rather than a reporting add-on.

Talent management and internal mobility are projected to expand at 25.41% CAGR from 2026 to 2031, making it the fastest-growing function. This rise shows that the agentic AI in the HCM market is moving closer to workforce redeployment and retention goals, rather than just external hiring efficiency. Recruiting and candidate sourcing still account for a large share of the deployment volume, especially in frontline roles where speed and application completion matter. Conversational ATS deployments delivered a 72% average application completion rate, 3.5-day average time-to-hire, and 95% candidate satisfaction rating in 2025. Employee service and HR operations are also improving through higher case containment, while payroll and time administration remain more tightly controlled due to a low tolerance for error. Across the agentic AI in the HCM industry, the function mix shows that buyers are broadening spend from efficiency-led workflows toward workforce value creation.

Geography Analysis

North America held a 39.73% share of the global agentic AI market in the HCM market in 2025, making it the leading regional cluster. The United States anchored this position through a mature HCM software ecosystem, deep enterprise cloud adoption, and a stronger willingness to fund AI programs at scale. Unfilled U.S. job vacancies stood at 4.5% of total labor demand in February 2025, which continued to put pressure on hiring efficiency and supported demand for AI-led sourcing and screening. In January 2026, 64% of U.S. organizations had changed their approach to entry-level hiring due to AI agent influence, up from 18% in the prior quarter, signaling rapid normalization of AI-assisted recruiting practices. The region is also defining procurement standards because buyers now evaluate governance, explainability, and ROI together rather than treating compliance as a later-stage issue.

Visible enterprise commitments support the North American lead. In March 2026, Adecco Group signed an unlimited, multi-year Agentforce 360 agreement with Salesforce to power more than 50% of revenues with agentic AI across 27,000 recruiters in more than 60 countries by the end of 2026. Early United Kingdom pilots had already produced 15% time savings. At the same time, state-level employment AI rules in the United States are expanding, which means the agentic AI in the HCM market share gained in North America will increasingly depend on vendor readiness for notification, impact review, and anti-discrimination controls. Canada remains smaller in scale, but it is moving steadily as SME hiring adoption improves. Mexico is also part of the broader regional opportunity, though enterprise depth remains lower than in the United States.

Europe remained the second-largest region in the agentic AI in the HCM market, but it operates under the most demanding governance conditions. The EU AI Act has raised the compliance floor across recruitment, performance, and workforce allocation systems, meaning deployment speed is often slower, but governance quality is higher. The United Kingdom is moving on its own track, and in March 2026, the Information Commissioner's Office said that AI-supported hiring decisions still require genuine human oversight rather than formal approval without the authority to intervene. Europe also shows a significant skills gap, with only 21% of European employees having received generative AI training, compared with 45% in the United States, underscoring the need for continued investment in productivity-oriented HR AI tools. Asia-Pacific is projected to grow at a 29.11% CAGR from 2026 to 2031, making it the fastest-growing regional segment of the agentic AI in the HCM market. Southeast Asia is strengthening through higher HR AI usage and budget intent, while India, Japan, and China each add demand through different combinations of labor pressure, technology investment, and enterprise modernization. South America, the Middle East, and Africa remain early-stage opportunities, but large enterprise bases, cloud HCM modernization, and national digital programs are gradually expanding the addressable base for agentic AI in the HCM market.

- Phenom People, Inc.

- Eightfold AI Inc.

- iCIMS, Inc.

- Paradox, Inc.

- Beamery Inc.

- Gloat Ltd.

- HireVue, Inc.

- Findem, Inc.

- Harver B.V.

- Personio SE & Co. KG

- Degree, Inc. d/b/a Lattice

- Darwinbox Digital Solutions Private Limited

- Textio, Inc.

- Peoplebox Inc.

- Peoplelogic, Inc.

- Humaans Software UK LTD

- Wisq Inc.

- Visier, Inc.

- VIVAHR, LLC d/b/a AvaHR

- Jobs and Talent, S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Labor Scarcity in High-skill and Frontline Hiring

- 4.2.2 Demand for Always-on Employee Self-service and HR Case Deflection

- 4.2.3 Shift Toward Skills-Based Talent Decisions and Internal Mobility

- 4.2.4 Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount

- 4.2.5 Need to Orchestrate Work Across Fragmented ATS, HRIS, Helpdesk, and Collaboration Stacks

- 4.2.6 Emergence of Agent Governance Layers That Make Multi-agent HR Automation Auditable

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Cross-border Data Transfer, and AI Governance Burden

- 4.3.2 Integration Complexity Across Legacy HCM, Payroll, and Identity Systems

- 4.3.3 Works Council and Employee Relations Pushback Against Autonomous HR Decisions

- 4.3.4 Weak Process Standardization That Limits Agent Reliability in Mid-market Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Agentic AI Platforms and Orchestration Engines

- 5.1.2 AI Agents and Workflow Applications

- 5.1.3 Professional Services

- 5.1.4 Managed AI Services

- 5.2 By Function

- 5.2.1 Recruiting and Candidate Sourcing

- 5.2.2 Employee Service and HR Operations

- 5.2.3 Talent Management and Internal Mobility

- 5.2.4 Learning and Development

- 5.2.5 Workforce Planning and Analytics

- 5.2.6 Payroll and Time Administration

- 5.3 By Deployment Model

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End User Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Phenom People, Inc.

- 6.4.2 Eightfold AI Inc.

- 6.4.3 iCIMS, Inc.

- 6.4.4 Paradox, Inc.

- 6.4.5 Beamery Inc.

- 6.4.6 Gloat Ltd.

- 6.4.7 HireVue, Inc.

- 6.4.8 Findem, Inc.

- 6.4.9 Harver B.V.

- 6.4.10 Personio SE & Co. KG

- 6.4.11 Degree, Inc. d/b/a Lattice

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Textio, Inc.

- 6.4.14 Peoplebox Inc.

- 6.4.15 Peoplelogic, Inc.

- 6.4.16 Humaans Software UK LTD

- 6.4.17 Wisq Inc.

- 6.4.18 Visier, Inc.

- 6.4.19 VIVAHR, LLC d/b/a AvaHR

- 6.4.20 Jobs and Talent, S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment