PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073015

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073015

Circular Economy Platform For The IT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

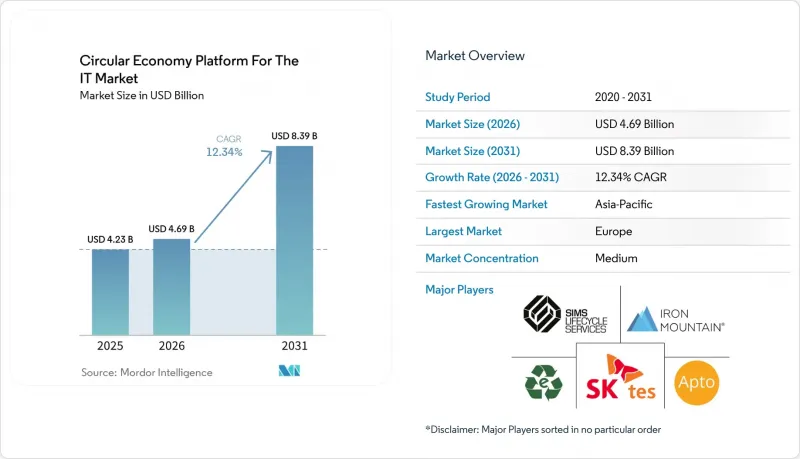

According to Mordor Intelligence, the circular economy platform for the IT market is projected to reach USD 4.23 billion in 2025, USD 4.69 billion in 2026, and USD 8.39 billion by 2031, growing at a CAGR of 12.34% from 2026 to 2031.

This report is Segmented by Offering (Software Platform, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Circular Economy Application (Asset Reuse and Redeployment, Refurbishment, ITAD, Recycling and Recovery, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Circular Economy Platform For The IT Market Trends and Insights

Rising Enterprise Demand for IT Asset Traceability

The circular economy platform for the IT market is seeing its strongest push from the need to track assets from deployment through data erasure and final disposition. Large enterprises with multi-site and multi-vendor estates cannot demonstrate compliance, ESG performance, or Scope 3 accountability when records are scattered across spreadsheets and disconnected service providers. One provider reported repurposing 8.8 million IT assets in FY2025, a scale that underscores the importance of consistent traceability as decommissioning moves across regions and device classes. Another platform positioned serialized asset discovery and parent-child relationship mapping across servers and drives to automate visibility, reflecting how traceability has become a core product differentiator rather than a background feature. When that level of visibility is in place, enterprises can treat retired hardware as a measurable recovery stream rather than a disposal cost line, which changes how procurement teams value platform adoption.

Regulatory Pressure on E-Waste Reporting and Audits

The circular economy platform for the IT market is also moving higher because e-waste reporting and audit rules are becoming more detailed across major economies. In July 2025, it was reported that nearly half of WEEE generated in the EU remained uncollected, only 40% was recycled, and just 23% of recycling facilities applied high-quality treatment standards, which is increasing pressure for tighter oversight.Italy brought Directive (EU) 2024/884 into national law with effect from January 2026, which changed parts of the WEEE framework and financing responsibilities under extended producer responsibility. Germany's system continues to require recurring producer reporting, and Regulation (EU) 2025/40 will apply from August 2026, meaning many enterprises now face overlapping documentation duties across jurisdictions. These layered timelines are increasing the demand for software and managed workflows that can keep reporting, registration, and audit records aligned without manual reconciliation.

Fragmented Asset Data Across Legacy IT Environments

The circular economy platform for the IT market still faces a major operational barrier: many enterprises lack clean, unified records of their installed hardware base. Serial numbers, ownership history, location data, and end-of-life status often reside across different ERP, ITAM, and regional systems, which slows onboarding and increases its cost. The issue is most visible in large organizations that expanded through acquisitions or system migrations, because they often need a discovery project before disposition workflows can even start. One provider's asset discovery layer was built to reconcile serial-level gaps between what is found in the field and what appears in client inventory systems, which shows how common this problem remains. Until upstream data quality improves, many buyers will continue to face an integration burden that delays value realization and limits platform usage after deployment

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Secure Data Sanitization Requirements

- Corporate ESG Targets Driving Circular Procurement

- Limited Standardization Across Global Take-Back Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms accounted for 68.74% of the circular economy platform share in the IT market in 2025, indicating that enterprises favored centralized systems that could tie together asset discovery, data erasure records, disposition routing, and ESG documentation. The market moved in this direction because manual processes and separate recycling engagements did not produce the serialized records required to meet current compliance expectations. As GDPR, WEEE, and related disclosure requirements demand clearer asset-level documentation, software-based control layers have become the simplest way to create a usable audit trail at scale. Buyers also value the ability to view device status, certificates, and recovery outcomes in one place, especially when hardware is spread across multiple business units and countries. This keeps software platforms at the center of the commercial model even when service delivery still happens through physical collection, repair, and remarketing operations.

Services are the fastest-growing offering type, and the circular economy platform for the IT market size for this segment is projected to expand at a 12.85% CAGR from 2026 to 2031. Enterprises are turning to managed service models when they lack internal ITAD expertise or when decommissioning cycles are becoming harder to manage due to AI server refresh activity. The installed base of AI servers has been identified as a major future ITAD challenge, underscoring the need for providers that can manage secure removal, grading, and recovery as an ongoing service. Service providers with recognized security and recycling credentials are also winning more enterprise tenders because buyers want a single accountable party for chain of custody, documentation, and jurisdiction-specific reporting.

Cloud held a 65.12% share in 2025, reflecting the appeal of lower upfront infrastructure costs and faster rollouts across distributed locations. The circular economy platform for the IT market adopted a cloud-first approach because many organizations wanted real-time asset tracking, automated reporting, and multi-site visibility without expanding their internal IT stacks. These benefits were especially relevant for mid-sized companies and newer technology businesses that needed structure but did not want to run an on-premises platform. At the same time, a full public cloud deployment does not suit every workflow because asset records, sanitization proofs, and customer data often reside in regulated environments. This is why deployment choice is increasingly shaped by compliance and data-handling needs rather than by pure architectural preference.

Hybrid is the fastest-growing deployment model, and the circular-economy platform for the IT market in this segment is projected to expand at a 12.92% CAGR from 2026 to 2031. Updated standards reinforced the need for program-level documentation and stronger operational controls, making hybrid deployment more suitable for organizations that need local control over sensitive records while still using cloud layers for reporting and partner coordination. Europe adds another pull factor because cross-border compliance and data management rules remain stricter, and China has also moved toward tighter controls through its national standard on electronic product information clearance. As a result, hybrid design is becoming the practical default for enterprise buyers that operate across regulated sectors or multiple jurisdictions.

Complete Report Scope:

- By Offering

- Software Platform

- Services

- By Deployment Model

- Cloud

- On Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By Circular Economy Application

- Asset Reuse and Redeployment

- Refurbishment

- ITAD

- Recycling and Recovery

- ESG and Compliance Reporting

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe accounted for 34.56% of the circular economy platform for the IT market share in 2025, maintaining its position as the largest regional market. The circular economy platform for the IT market is strongest in Europe because the region combines WEEE, broader sustainability disclosure pressures, and tighter producer accountability within a single operating environment. A July 2025 evaluation found that collection and treatment results still fall short of policy goals, and that gap reinforces the case for tighter controls and better reporting systems. Italy's January 2026 transposition of Directive (EU) 2024/884 and Germany's reporting framework add country-level administrative pressure on top of the wider EU framework. This combination keeps Europe ahead because enterprises in the region have fewer practical ways to manage end-of-life IT assets without formal platform support.

North America remained the second-largest region, supported by federal procurement requirements, enterprise decommissioning demand, and stronger media sanitization expectations. The circular economy platform for the IT market in the United States is also being lifted by the updated NIST sanitization framework and by faster hardware turnover in hyperscale data centers. Asset lifecycle management revenue reached USD 232 million in Q1 2026, up 92% year on year, with organic data center decommissioning growth exceeding 100%, demonstrating how quickly enterprise and hyperscaler activity is scaling in the region. South America remains smaller and less standardized, but demand is growing as enterprises lean more heavily on refurbishment, redeployment, and controlled disposal to extend hardware value under tighter budgets.

Asia-Pacific is the fastest-growing region, and the circular economy platform for the IT market size there is projected to grow at a 13.12% CAGR through 2031. The market is expanding quickly across Asia-Pacific, but the drivers differ by country: Japan is building stronger commercial partnerships, China is tightening clearance and information-handling standards, and India is attracting new processing capacity. A mandatory national standard published in December 2025 for electronic product information clearance adds a clear compliance trigger for enterprise sanitization and disposal workflows in China. In Japan, a capital and business alliance signed in April 2026 is building a circular tech value chain spanning procurement, third-party maintenance, remarketing, and ITAD. India, Australia, and South Korea remain earlier in their adoption curves, while the Middle East and Africa are still nascent, with demand centered on smart-city, digital infrastructure, and data-center modernization programs in markets such as Saudi Arabia and the UAE.

- Sims Lifecycle Services, Inc.

- Electronic Recyclers International, Inc.

- Iron Mountain Incorporated

- TES-Amm (Singapore) Pte Ltd.

- Apto Solutions, Inc.

- SK Tes Pte. Ltd.

- ERS International AG

- Ingram Micro Inc.

- Jabil Inc.

- Flex Ltd.

- Hewlett Packard Enterprise Company

- HP Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Canon Inc.

- Kyocera Corporation

- Sharp Corporation

- Cisco Systems, Inc.

- Oracle Corporation

- SAP SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Demand for IT Asset Traceability

- 4.2.2 Regulatory Pressure on E-Waste Reporting And Audits

- 4.2.3 Expansion of Secure Data Sanitization Requirements

- 4.2.4 Corporate ESG Targets Driving Circular Procurement

- 4.2.5 AI Enabled Asset Grading and Refurbishment Workflows

- 4.2.6 Multi-Vendor Fleet Complexity Increasing Platform Adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented Asset Data across Legacy IT Environments

- 4.3.2 Limited Standardization across Global Take-Back Programs

- 4.3.3 Trust Gaps Around Data Destruction and Chain of Custody

- 4.3.4 Channel Conflict with Incumbent ITAD and Resale Partners

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software Platform

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Medium Enterprises

- 5.4 By Circular Economy Application

- 5.4.1 Asset Reuse and Redeployment

- 5.4.2 Refurbishment

- 5.4.3 ITAD

- 5.4.4 Recycling and Recovery

- 5.4.5 ESG and Compliance Reporting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sims Lifecycle Services, Inc.

- 6.4.2 Electronic Recyclers International, Inc.

- 6.4.3 Iron Mountain Incorporated

- 6.4.4 TES-Amm (Singapore) Pte Ltd.

- 6.4.5 Apto Solutions, Inc.

- 6.4.6 SK Tes Pte. Ltd.

- 6.4.7 ERS International AG

- 6.4.8 Ingram Micro Inc.

- 6.4.9 Jabil Inc.

- 6.4.10 Flex Ltd.

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 HP Inc.

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Canon Inc.

- 6.4.16 Kyocera Corporation

- 6.4.17 Sharp Corporation

- 6.4.18 Cisco Systems, Inc.

- 6.4.19 Oracle Corporation

- 6.4.20 SAP SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment