PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073661

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073661

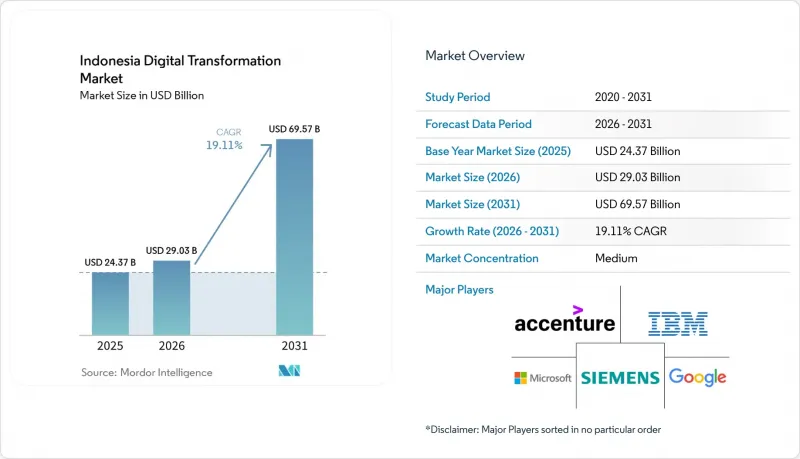

Indonesia Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia digital transformation market size is expected to grow from USD 24.37 billion in 2025 to USD 29.03 billion in 2026 and is forecast to reach USD 69.57 billion by 2031 at 19.11% CAGR over 2026-2031.

This report is Segmented by Type (Analytics, Artificial Intelligence and Machine Learning, and More), End User (Manufacturing, Oil Gas and Utilities, and More), Deployment Mode (On-Premise, and More), Enterprise Size (Large Enterprises, and More), Function (Operations and Production, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Digital Transformation Market Trends and Insights

Accelerated Cloud Infrastructure Rollouts by Hyperscalers

AWS has committed USD 5 billion to build data-center clusters in West Java, while Microsoft has earmarked USD 1.7 billion for additional capacity, creating localized regions that comply with the Personal Data Protection Law. These sovereign facilities satisfy data-residency rules and shorten latency for analytics, AI inference, and e-commerce workloads. Financial institutions are already capitalizing; Bank Jago moved core applications to Google Cloud, and Krom Bank migrated customer-facing services to AWS, gaining scalable computing power without compromising compliance. Edge nodes are being deployed across secondary cities so that factory-floor sensors and autonomous guided vehicles can process data in near real time. Enterprises report that the availability of local cloud zones has accelerated cloud migration velocity by roughly 40% year over year as fear of cross-border data transfer penalties subsides.

Rapid Proliferation of Mobile Devices and Super-Apps

Indonesia's mobile-first environment has become fertile ground for digital services, with smartphone adoption climbing across both metropolitan and second-tier cities. Super-apps such as Gojek's GoTo and regional rival Grab have evolved from ride-hailing platforms into integrated ecosystems encompassing payments, insurance, and B2B logistics. GoTo disclosed gross transaction value of 137.4 trillion rupiah in 2024, and the national QRIS system now links more than 22.4 million merchants, widening the reach of digital payments. The intertwined nature of commerce, payments, and on-demand services generates granular consumer data, enabling AI-driven segmentation that advertisers and retailers leverage for targeted campaigns. Partnerships between super-apps and cloud providers are also giving SMEs one-click access to inventory management, bookkeeping, and lending solutions embedded within familiar mobile interfaces.

Persistent Cyber-Security and Data-Sovereignty Concerns

Full enforcement of the Personal Data Protection Law in October 2024 introduced strict breach notification timelines and extraterritorial provisions that catch subsidiaries outside Indonesia. Financial institutions now require vendors to demonstrate compliance through third-party audits and localized key-management systems. Presidential Regulation 82/2022 further designates the banking, telecom, and energy sectors as vital information infrastructure and mandates periodic security assessments. While these measures mitigate systemic risk, compliance costs have risen, and enterprises face heightened scrutiny when moving sensitive workloads to the public cloud. Cyber-incident statistics from the central bank show that advanced persistent threats targeting critical sectors jumped 34.4% year over year in 2024, prompting demand for managed detection and response services tightly integrated into digital-transformation roadmaps.

Other drivers and restraints analyzed in the detailed report include:

- Government "Making Indonesia 4.0" Incentives

- 5G and LEO-Satellite Backhaul for Outer-Island Factories

- Shortage of Enterprise-Grade Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robotics recorded the fastest expansion within the Indonesia digital transformation market, advancing at a 22.05% CAGR over 2026-2031 as factories adopt collaborative robots for welding, pick-and-place, and quality inspection tasks. The Indonesia digital transformation market size attributable to industrial robots is set to more than triple as automotive, consumer-goods, and electronics plants retrofit legacy lines with AI-enabled vision systems. Simultaneously, cloud and edge computing held the largest slice of technology spending at 28.07% in 2025, powered by sovereign regions that satisfy data-localization rules. IoT deployments are maturing from proof-of-concept to scaled production monitoring, especially in food-processing facilities where humidity and temperature sensors have cut spoilage rates. Additive manufacturing remains niche but is gaining interest for spare-parts on-demand production, cutting lead times for remote mining operations.

Cloud databases, container orchestration, and AI platforms serve as the digital backbone connecting these point solutions. Cybersecurity tools embed zero-trust architecture into plant networks to safeguard programmable logic controllers from ransomware threats. Extended-reality applications for remote maintenance and workforce training lower travel costs and enhance safety. Blockchain pilots tracing palm-oil supply chains are moving into consortium governance models that encourage data-sharing among competitors without exposing proprietary information. The diverse technology mix underscores how the Indonesia digital transformation market continues broadening beyond initial cloud migrations toward full-stack digitization.

Manufacturing captured 23.78% of technology spend in 2025, reflecting early alignment with "Making Indonesia 4.0" productivity targets. Automated material-handling systems, digital twins, and predictive-maintenance analytics yielded tangible cost savings that justify ongoing investment. In contrast, the healthcare segment is scaling rapidly within the Indonesia connected healthcare ecosystem, with a forecast 23.62% CAGR, fuelled by telehealth reimbursement policies and hospital accreditation standards that require electronic health-record adoption. Start-ups are integrating AI chatbots into triage services, lightening the load on understaffed clinics across remote islands. Oil, gas, and utilities operators embed IoT sensors and digital twins to enhance safety and optimize asset uptime, while retail chains rely on super-app integration and cloud POS systems for omnichannel inventories.

The Indonesia digital transformation market size tied to healthcare stands to increase sharply as community health centers upgrade imaging and diagnostics. Banks and insurers apply machine-learning fraud detection to reduce claim denials, freeing budget for customer-experience automation. Public-sector agencies digitize citizen services, aligning back-office records with cloud-based workflow engines that improve transparency. Education institutions scale learning-management platforms, while media operators embrace OTT distribution and targeted advertising to monetize large subscriber bases. Each vertical is carving distinct digital roadmaps, yet all share a common dependence on reliable connectivity and secure data-handling frameworks.

Complete Report Scope:

- By Solution ype

- Analytics, Artificial Intelligence and Machine Learning

- Extended Reality (XR)

- Internet of Things (IoT)

- Industrial Robotics

- Blockchain

- Additive Manufacturing / 3D Printing

- Cybersecurity

- Cloud and Edge Computing

- Other Types - Digital Twin, Mobility and Connectivity

- By End User

- Manufacturing

- Oil, Gas and Utilities

- Retail and E-commerce

- Transportation and Logistics

- Healthcare

- Banking, Financial Services and Insurance (BFSI)

- Telecom and IT

- Government and Public Sector

- Other End Users - Education, Media and Entertainment, Environment

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Function

- Operations and Production

- Customer Experience and Front-office

- Finance and Accounting

- Human Resources

- Supply Chain and Procurement

List of Companies Covered in this Report:

- Accenture plc

- International Business Machines Corporation

- Microsoft Corporation

- Alphabet Inc. (Google LLC)

- Amazon Web Services Inc.

- SAP SE

- Oracle Corporation

- PT Telekomunikasi Indonesia (Persero) Tbk.

- Hewlett Packard Enterprise Company

- Cisco Systems Inc.

- Infosys Limited

- Siemens AG

- Apple Inc.

- Cognex Corporation

- Tata Consultancy Services Limited

- PT Multipolar Technology Tbk

- Salesforce Inc.

- Alibaba Cloud (Singapore) Private Limited

- Capgemini SE

- Fujitsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated cloud infrastructure roll-outs by hyperscalers

- 4.2.2 Rapid proliferation of mobile devices and super-apps

- 4.2.3 Government's "Making Indonesia 4.0" incentives

- 4.2.4 5G and LEO-satellite backhaul for outer-island factories

- 4.2.5 Rise of local AI-ASIC design start-ups

- 4.2.6 Millennial digital-native labour surge

- 4.3 Market Restraints

- 4.3.1 Persistent cyber-security and data-sovereignty concerns

- 4.3.2 Shortage of enterprise-grade talent

- 4.3.3 Fragmented regulatory compliance across provinces

- 4.3.4 Over reliance on imported industrial robotics

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Industry Ecosystem Analysis

- 4.10 Current Market Scenario and Evolution of Digital Transformation Practices

- 4.11 Key Metrics

- 4.11.1 Technology Spending Trends

- 4.11.2 Number of IoT Devices

- 4.11.3 Total Cyberattacks

- 4.11.4 Technology Staffing Trends

- 4.11.5 Internet Growth and Penetration

- 4.11.6 Digital Competitiveness Ranking

- 4.11.7 Fixed and Mobile Broadband Coverage

- 4.11.8 Cloud Adoption

- 4.11.9 AI Adoption

- 4.11.10 E-commerce Penetration

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution ype

- 5.1.1 Analytics, Artificial Intelligence and Machine Learning

- 5.1.2 Extended Reality (XR)

- 5.1.3 Internet of Things (IoT)

- 5.1.4 Industrial Robotics

- 5.1.5 Blockchain

- 5.1.6 Additive Manufacturing / 3D Printing

- 5.1.7 Cybersecurity

- 5.1.8 Cloud and Edge Computing

- 5.1.9 Other Types - Digital Twin, Mobility and Connectivity

- 5.2 By End User

- 5.2.1 Manufacturing

- 5.2.2 Oil, Gas and Utilities

- 5.2.3 Retail and E-commerce

- 5.2.4 Transportation and Logistics

- 5.2.5 Healthcare

- 5.2.6 Banking, Financial Services and Insurance (BFSI)

- 5.2.7 Telecom and IT

- 5.2.8 Government and Public Sector

- 5.2.9 Other End Users - Education, Media and Entertainment, Environment

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises (SMEs)

- 5.5 By Function

- 5.5.1 Operations and Production

- 5.5.2 Customer Experience and Front-office

- 5.5.3 Finance and Accounting

- 5.5.4 Human Resources

- 5.5.5 Supply Chain and Procurement

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 International Business Machines Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Alphabet Inc. (Google LLC)

- 6.4.5 Amazon Web Services Inc.

- 6.4.6 SAP SE

- 6.4.7 Oracle Corporation

- 6.4.8 PT Telekomunikasi Indonesia (Persero) Tbk.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Cisco Systems Inc.

- 6.4.11 Infosys Limited

- 6.4.12 Siemens AG

- 6.4.13 Apple Inc.

- 6.4.14 Cognex Corporation

- 6.4.15 Tata Consultancy Services Limited

- 6.4.16 PT Multipolar Technology Tbk

- 6.4.17 Salesforce Inc.

- 6.4.18 Alibaba Cloud (Singapore) Private Limited

- 6.4.19 Capgemini SE

- 6.4.20 Fujitsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment