PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073659

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073659

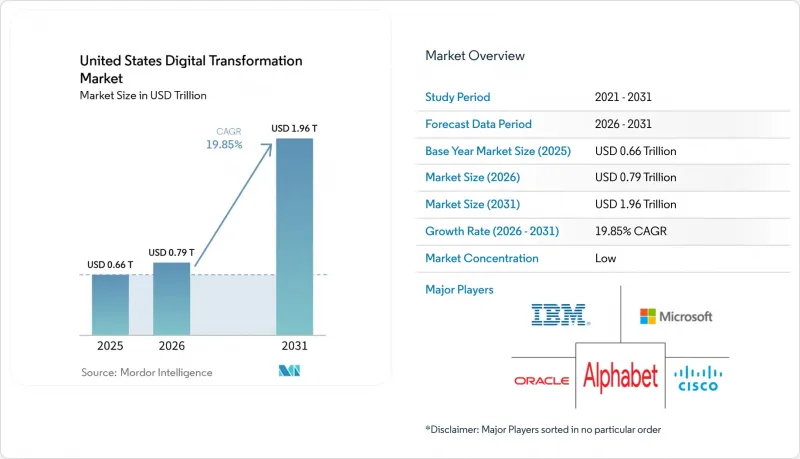

United States Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states digital transformation market size was valued at USD 0.66 trillion in 2025 and estimated to grow from USD 0.79 trillion in 2026 to reach USD 1.96 trillion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise, Hybrid), Enterprise Size (Large Enterprises, Small and Medium Enterprises), Type (Analytics, AI and ML, Extended Reality (XR), and More), End-User Industry (BFSI, Healthcare and Life Sciences, Manufacturing, and More) and by Region. The Market Forecasts are Provided in Terms of Value (USD).

United States Digital Transformation Market Trends and Insights

Surge in Federal Cloud-Smart & FedRAMP Programs

FedRAMP 20x removes agency-sponsorship for low-impact workloads and automates security reviews, enabling federal cloud migrations to finish 60% faster. Civilian IT outlays allocate USD 74 billion for modernization in 2025, with USD 12.7 billion ring-fenced for cybersecurity. Vendors that pre-certify solutions under the codified FedRAMP Authorization Act gain preferred-supplier status, driving spillover demand across state and local agencies.

Generative-AI Adoption for Hyper-Personalized CX

Seventy-eight percent of U.S. firms now embed generative AI, producing a 3.7X ROI as Fortune 500 groups scale OpenAI-powered chat and design tools. By end-2025, 25% of enterprises plan agent-based deployments that automate frontline tasks. Sector-specific large-language models in healthcare, finance, and retail sustain compliance while boosting service quality.

State-Level Privacy Patchwork (CPRA etc.)

Nineteen states have enacted comprehensive privacy statutes, and enforcement teams in California, Texas, and Virginia elevate compliance risk. Compliance spending rises 30-50% for multi-state businesses, with SMEs bearing higher proportional costs in the absence of a single federal framework.

Other drivers and restraints analyzed in the detailed report include:

- CMS-Backed "Digital Front Door" Funding in Healthcare

- IoT & Digital-Twin Uptake from U.S. Reshoring Wave

- Legacy Mainframe Lock-in across Tier-1 Banks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for a dominant 67.40% of the United States digital transformation market share in 2025, underpinned by enterprise investments in cloud, cybersecurity, and analytics platforms. The services arena, however, is forecast to post a 20.74% CAGR as firms turn to consultancies for integration, AI model tuning, and managed operations. A widening data-science skills gap-cited by 53% of IT leaders-reinforces demand for external expertise.

Demand for continuous optimization is reshaping services portfolios from one-time installs to outcome-based contracts. Providers bundle change-management and AI-governance advisories that accelerate time-to-value. As digital maturity grows, the United States digital transformation market size for services is expected to close the revenue gap with solutions by 2031.

On-premise platforms retained 50.12% of the United States digital transformation market size in 2025, reflecting strict data-sovereignty rules in BFSI and healthcare. Cloud solutions, climbing at a 20.35% CAGR, benefit from FedRAMP streamlining and hybrid-cloud blueprints. Oracle-Google interconnects let firms run OCI databases alongside Google Analytics without cross-cloud fees.

Hybrid architectures combine on-premise control with elastic public-cloud compute, mitigating latency and compliance concerns while supporting AI workloads. By 2031, equilibrium between deployment models is plausible as cloud security hardens and mission-critical workloads gradually exit legacy stacks.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Mid-sized Enterprises (SMEs)

- By Type

- Analytics, AI and ML

- Internet of Things (IoT)

- Cyber-security

- Cloud and Edge Computing

- Extended Reality (XR)

- Blockchain

- Industrial Robotics

- Additive Manufacturing / 3-D Printing

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Transportation and Logistics

- Oil, Gas and Utilities

- Telecom and IT Services

- Government and Public Sector

- Others

- By Region

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Microsoft Corporation

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Cisco Systems, Inc.

- Oracle Corp.

- Amazon Web Services, Inc.

- Accenture plc

- Adobe Inc.

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- ServiceNow, Inc.

- Salesforce, Inc.

- Cognizant Technology Solutions

- Capgemini SE

- Infosys Ltd.

- Deloitte Touche Tohmatsu Ltd.

- PwC LLP

- DXC Technology Co.

- Tata Consultancy Services Ltd.

- Schneider Electric SE

- Siemens AG

- NTT DATA Corp.

- Ericsson AB

- KPMG LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Federal Cloud-Smart and FedRAMP Programs

- 4.2.2 Generative-AI Adoption for Hyper-Personalized CX

- 4.2.3 CMS-Backed "Digital Front Door" Funding in Healthcare

- 4.2.4 IoT and Digital-Twin Uptake from U.S. Reshoring Wave

- 4.2.5 ESG Data-Platform Investments Driven by SEC Climate Rules

- 4.2.6 5G SA Roll-outs Unlocking Edge-Computing Use Cases

- 4.3 Market Restraints

- 4.3.1 State-Level Privacy Patchwork (CPRA etc.)

- 4.3.2 Legacy Mainframe Lock-in across Tier-1 Banks

- 4.3.3 Cloud-Security Talent Shortage Inflating TCO

- 4.3.4 Pandemic-Era Technical Debt Hindering Integration

- 4.4 Value / Supply-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Current Market Scenario and Evolution of Practices

- 4.7 Key Metrics

- 4.7.1 Technology Spending Trends

- 4.7.2 Number of IoT Devices

- 4.7.3 Cyber-attack Volume

- 4.7.4 Cloud-Adoption Rate

- 4.7.5 Digital Competitiveness Ranking

- 4.8 Regulatory and Technological Outlook

- 4.9 Key Transformative Technologies

- 4.9.1 Quantum Computing

- 4.9.2 Manufacturing-as-a-Service (MaaS)

- 4.9.3 Cognitive Process Automation

- 4.9.4 Nanotechnology

- 4.10 Porter's Five Forces

- 4.10.1 Competitive Rivalry

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Bargaining Power of Suppliers

- 4.10.4 Threat of New Entrants

- 4.10.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By Type

- 5.4.1 Analytics, AI and ML

- 5.4.2 Internet of Things (IoT)

- 5.4.3 Cyber-security

- 5.4.4 Cloud and Edge Computing

- 5.4.5 Extended Reality (XR)

- 5.4.6 Blockchain

- 5.4.7 Industrial Robotics

- 5.4.8 Additive Manufacturing / 3-D Printing

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Manufacturing

- 5.5.4 Retail and E-commerce

- 5.5.5 Transportation and Logistics

- 5.5.6 Oil, Gas and Utilities

- 5.5.7 Telecom and IT Services

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Google LLC (Alphabet Inc.)

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Oracle Corp.

- 6.4.6 Amazon Web Services, Inc.

- 6.4.7 Accenture plc

- 6.4.8 Adobe Inc.

- 6.4.9 SAP SE

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Hewlett Packard Enterprise Co.

- 6.4.12 ServiceNow, Inc.

- 6.4.13 Salesforce, Inc.

- 6.4.14 Cognizant Technology Solutions

- 6.4.15 Capgemini SE

- 6.4.16 Infosys Ltd.

- 6.4.17 Deloitte Touche Tohmatsu Ltd.

- 6.4.18 PwC LLP

- 6.4.19 DXC Technology Co.

- 6.4.20 Tata Consultancy Services Ltd.

- 6.4.21 Schneider Electric SE

- 6.4.22 Siemens AG

- 6.4.23 NTT DATA Corp.

- 6.4.24 Ericsson AB

- 6.4.25 KPMG LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment