PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073024

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073024

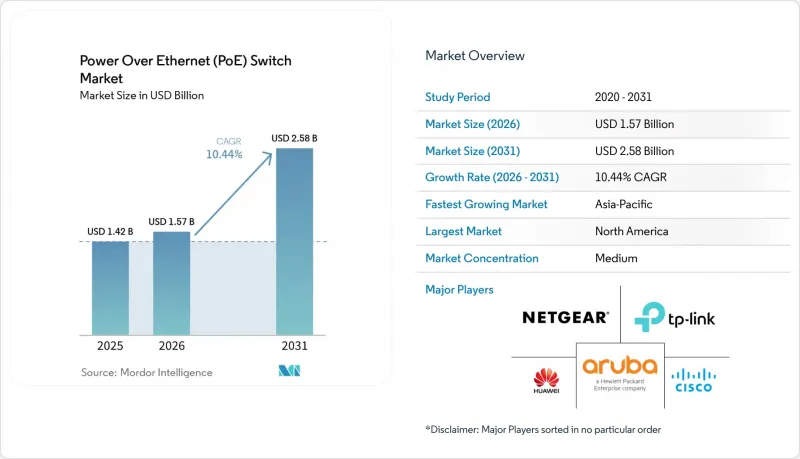

Power Over Ethernet (PoE) ++ Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the power over Ethernet (PoE) ++ switch market size is projected to expand from USD 1.42 billion in 2025 and USD 1.57 billion in 2026 to USD 2.58 billion by 2031, registering a CAGR of 10.44% over 2026-2031.

This report is Segmented by Power Output (Up Io 60 W, 60-90 W, and More), Switch Type (Unmanaged, Fully Managed Layer 2, and More), Port Density (5-8 Ports, 9-16 Ports, and More), Application (IP Surveillance and Security Cameras, and More), End-User Industry (Commercial and Enterprise, Residential, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Power Over Ethernet (PoE) ++ Switch Market Trends and Insights

Proliferation of IoT Endpoints and IP Surveillance Cameras

The growth of connected endpoints remains the clearest demand driver for the Power over Ethernet (PoE) ++ switch market, as every new camera, access point, sensor cluster, or smart-lighting node adds to the load on the access layer. Computer-vision cameras stand out in this mix because newer PTZ systems combine analytics, infrared illumination, and motion features that require much more power than older 1080p devices. Axis states that the Q6358-LE can draw up to 51 W, placing it firmly in the range where 802.3bt-capable source equipment is required for full operation. When surveillance operators replace installed cameras without replacing older switching gear, they often find that the bottleneck is not optics or bandwidth, but port-level power availability. That shifts refresh timing in practical ways, because the camera project starts first, but the switch upgrade follows immediately once the power gap becomes visible. In many building deployments, the camera cycle is therefore becoming the event that brings forward broader hardware spending in the Power over Ethernet (PoE) ++ switch market.

Wi-Fi 6/6E Access-Point Roll-Outs Requiring 60 W or More per Port

New Wi-Fi 6E and Wi-Fi 7 access points are raising baseline power expectations in the Power over Ethernet (PoE) ++ switch market, because they lose features when deployed on older 802.3af or 802.3at infrastructure. Cisco documentation for the Catalyst 9166 series shows that IEEE 802.3bt UPOE supports full tri-radio operation, a 5 Gbps Multigigabit port, and USB IoT output, while lower-power modes reduce capability. HPE Aruba guidance similarly positions 802.3bt Class 6 as the practical baseline for new Wi-Fi 6E deployments, which makes higher-power switching relevant even before buyers move into Wi-Fi 7 refresh cycles. Cisco and Juniper also document that Wi-Fi 7 platforms such as the CW9178I and AP47 require Type 4 delivery for full dual-4x4 multi-link operation, which pulls power design into the earliest stages of campus planning. A 48-port platform running 90 W per port can support a 4,320 W PoE budget, shifting closet-level planning from a typical access switch decision to a broader facility power decision. That is why wireless refresh cycles are now creating one of the strongest near-term upgrade paths for the Power over Ethernet (PoE) ++ switch market.

Higher BOM and Thermal Design Burden for 802.3bt Switches

A Type 4 switch is a more complex product than an older 802.3at platform, and that complexity continues to slow some upgrades in the Power over Ethernet (PoE) ++ switch market. Running simultaneous power and data over all 4 cable pairs at 90 W per port requires efficient DC-DC conversion, precision detection circuitry, stronger heat management, and larger internal power design. Cisco's C9350-48HX illustrates the scale of that requirement, because full-density 90 W delivery depends on three hot-swappable 1,600 W Titanium-rated power supplies and StackPower+ support. For SMB and mid-enterprise buyers, the cost of power supplies, cabling upgrades, and cooling adjustments can raise total deployment cost to 2-3 times that of a comparable 802.3at setup. That gap keeps a large part of the installed base in the PoE+ tier, especially in projects where wireless or camera demand has not yet crossed the threshold that forces higher wattage. The restraint is strongest outside large North American enterprise programs, where buyers are less willing to absorb a single-cycle jump in both hardware and infrastructure cost.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Building Retrofits Adopting PoE-Powered LED Lighting

- Energy-Efficiency Regulations Favoring Remote Power Monitoring

- Legacy Cabling Length and Gauge Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Up to 60 W retained 42.2% of the Power over Ethernet (PoE) ++ switch market size in 2025, because the installed base of VoIP phones, basic wireless access points, and older IP cameras still renews on legacy power classes. That large base gives the lower-wattage tier durability even as device requirements move upward, since many branch and floor-level refreshes still favor continuity and lower upfront cost. The 60-90 W segment is the fastest-growing tier in the Power over Ethernet (PoE) ++ switch market, with an 18.4% CAGR projected from 2026 to 2031. That growth is tied directly to Wi-Fi 6E and Wi-Fi 7 radios, AI-enabled PTZ cameras, and other endpoints that need Class 6 or Class 8 delivery for full features. The above 90 W category remains early in volume terms, but Cisco's UPOE+ path and the power profiles of newer multiradio platforms show that the upper boundary is already being tested in select deployments.

The Power over Ethernet (PoE) ++ switch market is also being shaped by edge-compute convergence, because the switch is no longer only a power source and transport layer. Cisco's C9350 platform brings a quad-core x86 CPU and 16 GB DDR5 memory into the access layer so that third-party containers can run on the switch while it also supplies high-wattage PoE to endpoint clusters. That shifts planning assumptions, since switch heat output and closet power availability begin to look closer to small edge-server environments than traditional access closets. In Europe, reporting and energy-monitoring obligations further favor managed 802.3bt platforms, because unmanaged alternatives cannot support the same level of per-port visibility needed in regulated settings.

Fully Managed Layer 2 accounted for 46.1% of the Power over Ethernet (PoE++) switch market share in 2025, reflecting how much of the enterprise installed base still depends on VLAN-based policy and Layer 2 intelligence at the access edge. This segment remains large because many branch offices, campus floors, and standard commercial deployments still prioritize operational familiarity over architectural change. Unmanaged and Smart or Hybrid Managed products continue to serve the SMB and mid-market base, where lower upfront cost and simple deployment still matter more than broad automation features. Fully Managed Layer 3 is the fastest-growing switch type in the Power over Ethernet (PoE) ++ switch market, at an 18.2% CAGR from 2026 to 2031. The main reason is the move toward EVPN-VXLAN campus fabrics, where routing and policy enforcement at the access layer help separate IT and IoT traffic without sending flows back through higher-tier devices.

Juniper's February 2025 EX4000 launch is a clear example of this direction, because it pairs 802.3bt PoE++, Mist AI telemetry, Virtual Chassis stacking, and fast boot times for modern access deployments. Another point of change is zero-trust enforcement at the port, which is becoming more important as building systems and user traffic share the same network edge. Fortinet positions its FortiSwitch line with FortiGate integration through FortiLink, allowing dynamic NAC policy and device profiling without the need for a separate appliance layer. That lifts the role of the Power over Ethernet (PoE++) switch industry beyond simple connectivity and makes switching a more central control point in government, healthcare, and other regulated deployments.

Complete Report Scope:

- By Power Output

- Up to 60 W (PoE/PoE+)

- 60 - 90 W (PoE++)

- Above 90 W (next-gen high-power)

- By Switch Type

- Unmanaged

- Smart/Hybrid Managed

- Fully Managed Layer 2

- Fully Managed Layer 3

- By Port Density

- 5-8 Ports

- 9-16 Ports

- 17-24 Ports

- 25-48 Ports

- Above 48 Ports

- By Application

- IP Surveillance and Security Cameras

- Wireless Access Points and WLAN Infrastructure

- VoIP and Unified Communication Devices

- LED Lighting Systems

- Building Automation and Smart Controls

- IoT Gateways and Edge Computing Devices

- By End-User Industry

- Commercial, and Enterprise

- Industrial and Manufacturing

- Government, Defense, and Smart Cities

- Residential

- Healthcare and Education

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Oceania

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 37.1% of the Power over Ethernet (PoE) ++ switch market share in 2025, and it remained the largest regional base because enterprise campuses and government facilities already have deep managed-switch penetration. The United States supported this lead through federal smart-building modernization programs and continued demand for higher-performance campus access networks. Canada added demand through managed services expansion and healthcare IT upgrades, which supported steady purchasing across institutional environments. Mexico contributed incremental volume from industrial zone builds and hospitality projects, where new properties can install higher-grade cabling and managed access networks from the outset. Sustainability compliance is also becoming a stronger buying factor in this region, because large facilities increasingly want managed PoE switches that can provide energy telemetry rather than only transport and power.

Asia-Pacific is the fastest-growing regional block in the Power over Ethernet (PoE) ++ switch market, and it is forecast to expand at a 12.9% CAGR through 2031. China is the main growth engine because smart-city, transportation, public security, and building automation projects are all adding demand for higher-power access-layer equipment. The Ministry of Industry and Information Technology set a target of more than 10 billion IoT device connections by 2028 and a core IoT industry size above CNY 3.5 trillion, equal to USD 486 billion at the 2025 IRS average exchange rate retained in the input, which reinforces the scale of downstream infrastructure demand. In March 2026, Sinopec's Tianjin subsidiary issued procurement for PoE-based lighting and video monitoring terminals, showing that industrial buyers are also joining the regional adoption curve. India and Japan broaden the picture, because India's digitalization and smart-city programs support Ethernet-led access networks while Japan adds higher-value factory automation use cases tied to robotic guidance and edge-AI cameras.

Europe kept a steady position in the Power over Ethernet (PoE) ++ switch market, because the policy framework for zero-emission new construction and lower primary energy use in existing non-residential buildings continues to support retrofit activity. Germany, the United Kingdom, and France remain the core premium smart-building markets, while Russia's separation from Western supply chains is shifting procurement patterns toward domestic and Chinese suppliers. South America is smaller in absolute value, but Brazil and Argentina are still seeing project-led uptake in Sao Paulo and Buenos Aires where international tenants increasingly specify LEED-aligned PoE infrastructure. Middle East and Africa remains the smallest regional block by volume, yet Gulf projects under Saudi Vision 2030 and UAE digital-city programs are creating above-average demand for surveillance and building-automation networks that favor higher-wattage PoE switching.

- Cisco Systems, Inc.

- Huawei Technologies

- Hewlett Packard Enterprise (Aruba)

- Netgear, Inc.

- TP-Link Technologies

- D-Link Corporation

- Ubiquiti Inc.

- Juniper Networks

- Zyxel Communications

- Extreme Networks

- Fortinet Inc.

- TRENDnet Inc.

- MikroTik

- Allied Telesis

- Belden (Hirschmann)

- Siemens AG

- Planet Technology

- Antaira Technologies

- Red Lion Controls

- Ruckus Networks (CommScope)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT Endpoints and IP Surveillance Cameras

- 4.2.2 Smart-Building Retrofits Adopting PoE-Powered LED Lighting

- 4.2.3 Wi-Fi 6/6E Access-Point Roll-Outs Requiring >=60 W Per Port

- 4.2.4 Energy-Efficiency Regulations Favoring Remote Power Monitoring

- 4.2.5 Edge-AI Cameras With Heaters and Pan-tilt Heads (More than 60 W)

- 4.2.6 ESG-Driven Copper-Cable Reduction Targets in Enterprise Networks

- 4.3 Market Restraints

- 4.3.1 Higher BOM Cost and Thermal Design for 802.3bt 90 W Switches

- 4.3.2 Legacy Cat5e/Cat6 Cabling Length and Gauge Limitations

- 4.3.3 Emerging USB-C Power-Delivery-Over-IP Alternatives

- 4.3.4 Supply-Chain Tightness for High-Efficiency DC-DC Converter ICs

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Output

- 5.1.1 Up to 60 W (PoE/PoE+)

- 5.1.2 60 - 90 W (PoE++)

- 5.1.3 Above 90 W (next-gen high-power)

- 5.2 By Switch Type

- 5.2.1 Unmanaged

- 5.2.2 Smart/Hybrid Managed

- 5.2.3 Fully Managed Layer 2

- 5.2.4 Fully Managed Layer 3

- 5.3 By Port Density

- 5.3.1 5-8 Ports

- 5.3.2 9-16 Ports

- 5.3.3 17-24 Ports

- 5.3.4 25-48 Ports

- 5.3.5 Above 48 Ports

- 5.4 By Application

- 5.4.1 IP Surveillance and Security Cameras

- 5.4.2 Wireless Access Points and WLAN Infrastructure

- 5.4.3 VoIP and Unified Communication Devices

- 5.4.4 LED Lighting Systems

- 5.4.5 Building Automation and Smart Controls

- 5.4.6 IoT Gateways and Edge Computing Devices

- 5.5 By End-User Industry

- 5.5.1 Commercial, and Enterprise

- 5.5.2 Industrial and Manufacturing

- 5.5.3 Government, Defense, and Smart Cities

- 5.5.4 Residential

- 5.5.5 Healthcare and Education

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Oceania

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies

- 6.4.3 Hewlett Packard Enterprise (Aruba)

- 6.4.4 Netgear, Inc.

- 6.4.5 TP-Link Technologies

- 6.4.6 D-Link Corporation

- 6.4.7 Ubiquiti Inc.

- 6.4.8 Juniper Networks

- 6.4.9 Zyxel Communications

- 6.4.10 Extreme Networks

- 6.4.11 Fortinet Inc.

- 6.4.12 TRENDnet Inc.

- 6.4.13 MikroTik

- 6.4.14 Allied Telesis

- 6.4.15 Belden (Hirschmann)

- 6.4.16 Siemens AG

- 6.4.17 Planet Technology

- 6.4.18 Antaira Technologies

- 6.4.19 Red Lion Controls

- 6.4.20 Ruckus Networks (CommScope)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment