PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073139

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073139

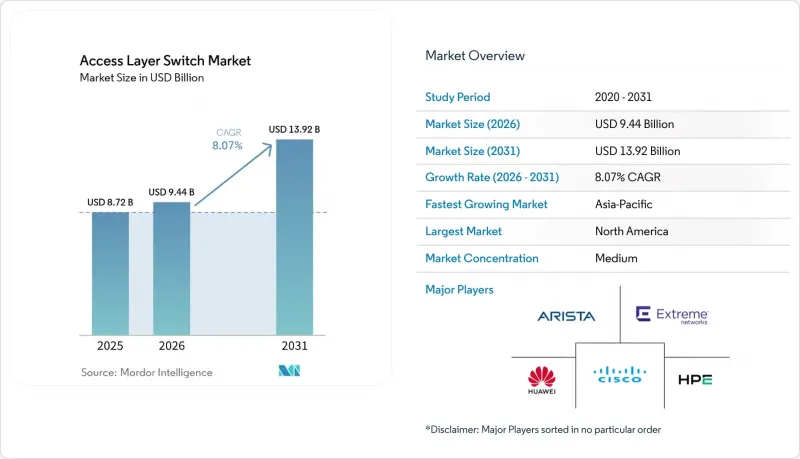

Access Layer Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the access layer switch market size is projected to expand from USD 8.72 billion in 2025 and USD 9.44 billion in 2026 to USD 13.92 billion by 2031, registering a CAGR of 8.07% between 2026 and 2031.

This report is Segmented by Port Speed (1 GbE and Below, 2. 5/5 GbE Multi-Gig, and More), Port Density (Small Form Factor, Mid-Range, High-Density, and More), End-User Enterprise Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Healthcare and Lifesciences, Manufacturing, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Access Layer Switch Market Trends and Insights

Accelerated Campus Digitalization in the Education Vertical

Universities are replacing legacy switches to power hybrid learning, IoT-enabled campuses, and research clusters that depend on multi-gigabit throughput. A 2025 survey of United States higher-education IT leaders found that 60% planned network upgrades within 2 years. UCLA deployed 2.5 GbE-enabled Catalyst 9000 switches across 419 buildings to support Wi-Fi 6E services for 45,000 students CISCO.COM. Washington University adopted HPE Aruba CX switches to enforce role-based segmentation at scale. Dynamic provisioning and cloud orchestration shorten refresh cycles, making academia a steady growth pocket for the access layer switch market.

Surge in Wi-Fi 6 and Wi-Fi 7 Access Point Roll-outs

Wi-Fi 7 reached mainstream status by late 2025 and now represents a sizable share of enterprise wireless spend. IEEE 802.11be radios demand multi-gig uplinks, and the IEEE 802.3bz standard lets enterprises reuse existing Cat 5e and Cat 6 cabling without disruptive rewiring. Arista and Dell introduced 2.5/5 GbE-ready campus switches that integrate wireless telemetry under a single software plane. Power-over-Ethernet budgets rose to 90 W per port under IEEE 802.3bt, further accelerating the retirement of 1 GbE-only platforms.

Supply Chain Volatility of Merchant Switch ASICs

Broadcom's near-monopoly in Tomahawk, Trident, and Jericho chips concentrates risk. TSMC lead times for advanced nodes stretched from six weeks in early 2024 to six months by late 2025, forcing vendors to ration inventory. Export-control uncertainty and multilayer PCB bottlenecks further strain availability. Alternative silicon from Marvell or Intel exists, yet redesign cycles exceed two years, maintaining dependency on Broadcom in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Edge Computing Workload Densification at Branch Sites

- Mandatory Network Access Control Compliance in Regulated Industries

- Skills Gap in Managing Policy-Driven Fabric Architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional 1 GbE and below ports held 52.18% market share in 2025, sustained by the installed base of legacy endpoints and the economic inertia of organizations deferring infrastructure refresh until end-of-support deadlines force action. The 2.5/5 GbE tier, anchored in IEEE 802.3bz, is forecast to outpace every other speed class with a 12.84 % CAGR through 2031. Enterprises treat multi-gig as a bridge between legacy 1 GbE endpoints and future 10 GbE fiber, preserving existing copper runs while meeting Wi-Fi 7 backhaul needs. Vendor roadmaps now default to multi-gig plus IEEE 802.3bt power budgets, signaling that 1 GbE will gradually enter maintenance mode.

Mature 10 GbE optics support uplinks and server access at falling price points, while 25/40 GbE and above remain concentrated in data-center racks that require east-west throughput. The access layer switch market size for multi-gig is projected to reach meaningful parity with 1 GbE by 2028, solidifying its role as the new default. At the same time, improved interoperability and vendor standardization are reducing deployment friction, accelerating enterprise-wide adoption of multi-gig infrastructure.

Mid-range 24-48-port devices dominated the market with 42.26% market share in 2025 wiring closets due to legacy device counts, yet refresh budgets increasingly tilt toward larger fixed-form-factor models that cut per-port power consumption. High-density 48-96-port switches are expected to grow at 9.26 % CAGR, benefiting from campus-aggregation consolidation and data-center top-of-rack designs that minimize cabling. This shift is also driven by the need to simplify network architecture and reduce the number of physical devices per site.

Extreme Networks and Arista offer modular port groups that mix 1 GbE, multi-gig, and 25 GbE in one chassis, enabling phased migrations without forklift upgrades. The access layer switch market share for high-density platforms is set to climb as organizations rationalize closets and seek operational economies of scale. Additionally, higher-density configurations help optimize rack space and support automation-driven network designs, making them increasingly attractive for modern campus deployments.

Complete Report Scope:

- By Port Speed

- 1 GbE and Below

- 2.5/5 GbE Multi-Gig

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE and Above

- By Port Density

- Small Form Factor (8-24 ports)

- Mid-Range (24-48 ports)

- High-Density (48-96 ports)

- Ultra-High-Density (100+ ports)

- By End-user Enterprise Size

- Large Enterprises

- SMEs

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare and Lifesciences

- Manufacturing

- Government and Defense

- Education

- Retail and E-commerce

- Other End User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 38.46 % of 2025 revenue due to entrenched campus modernizations, higher-education refreshes, and early zero-trust adoption across healthcare and federal agencies. Budget certainty and mature partner ecosystems underpin a predictable refresh cadence, although slowing replacement in small branches caps upside. In addition, widespread adoption of cloud-managed networking and advanced security frameworks continues to reinforce steady demand across enterprise campuses.

Europe follows closely, propelled by NIS2 and DORA mandates that require authenticated device access and continuous monitoring. Energy-efficient Ethernet goals tied to net-zero pledges spur PoE switch upgrades in corporate campuses, while public-sector approvals prolong deal cycles. Eastern European manufacturing corridors add incremental demand as industrial IoT pilots scale, further supported by EU funding programs aimed at digital infrastructure modernization.

Asia-Pacific is the fastest-growing geography at 9.54 % CAGR. India's Digital India program earmarked INR 1.5 trillion (USD 18 billion) for smart-city and broadband projects, while China's 14th Five-Year Plan prioritizes industrial internet build-outs. ASEAN's Smart Cities Network and Japan's Society 5.0 schemes likewise elevate regional spending. These multi-year directives ensure sustained momentum for the access layer switch market in the region, with greenfield deployments and rapid enterprise expansion driving incremental growth.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Extreme Networks, Inc.

- Dell Technologies Inc.

- Fortinet, Inc.

- TP-Link Technologies Co., Ltd.

- D-Link Corporation

- Alcatel-Lucent Enterprise (ALE International SAS)

- Ubiquiti Inc.

- Zyxel Communications Corporation

- Ruijie Networks Co., Ltd.

- Edgecore Networks Corporation

- Allied Telesis Holdings K.K.

- MikroTikls SIA

- Avaya LLC

- NETGEAR, Inc.

- Cumulus Networks

- Sophos Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Campus Digitalization in Education Vertical

- 4.2.2 Surge in Wi-Fi 6 and Wi-Fi 7 Access Point Roll-outs

- 4.2.3 Edge Computing Workload Densification at Branch Sites

- 4.2.4 Mandatory Network Access Control Compliance in Regulated Industries

- 4.2.5 Open-Networking Disaggregation Momentum in Telecom Access

- 4.2.6 Energy-Efficient Ethernet Adoption Targets under Net-Zero Mandates

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility of Merchant Switch ASICs

- 4.3.2 Skills Gap in Managing Policy-Driven Fabric Architectures

- 4.3.3 Rising Substitution by High-End WLAN for SMB Segments

- 4.3.4 Prolonged Capex Cycles in Public Sector Networks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Port Speed

- 5.1.1 1 GbE and Below

- 5.1.2 2.5/5 GbE Multi-Gig

- 5.1.3 10 GbE

- 5.1.4 25/40 GbE

- 5.1.5 100 GbE

- 5.1.6 400 GbE and Above

- 5.2 By Port Density

- 5.2.1 Small Form Factor (8-24 ports)

- 5.2.2 Mid-Range (24-48 ports)

- 5.2.3 High-Density (48-96 ports)

- 5.2.4 Ultra-High-Density (100+ ports)

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Manufacturing

- 5.4.5 Government and Defense

- 5.4.6 Education

- 5.4.7 Retail and E-commerce

- 5.4.8 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Arista Networks, Inc.

- 6.4.5 Extreme Networks, Inc.

- 6.4.6 Dell Technologies Inc.

- 6.4.7 Fortinet, Inc.

- 6.4.8 TP-Link Technologies Co., Ltd.

- 6.4.9 D-Link Corporation

- 6.4.10 Alcatel-Lucent Enterprise (ALE International SAS)

- 6.4.11 Ubiquiti Inc.

- 6.4.12 Zyxel Communications Corporation

- 6.4.13 Ruijie Networks Co., Ltd.

- 6.4.14 Edgecore Networks Corporation

- 6.4.15 Allied Telesis Holdings K.K.

- 6.4.16 MikroTikls SIA

- 6.4.17 Avaya LLC

- 6.4.18 NETGEAR, Inc.

- 6.4.19 Cumulus Networks

- 6.4.20 Sophos Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment