PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073132

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073132

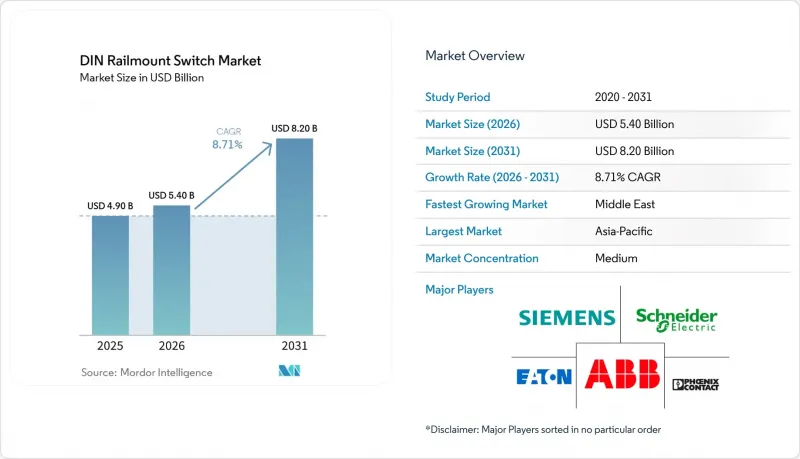

DIN Railmount Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the DIN railmount switch market size is expected to increase from USD 5.4 billion in 2026 to USD 8.2 billion by 2031, growing at a CAGR of 8.71% over 2026-2031.

This report is Segmented by Switch Type (Circuit Breaker, Isolator/Disconnect, and More), Voltage Rating (Up To 250 VAC, 251-500 VAC, Above 500 VAC), End-User Industry (Industrial Automation, Energy and Power, Building and Construction, and More), Sales Channel (Direct OEM, Distributors/Wholesalers, E-Commerce), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global DIN Railmount Switch Market Trends and Insights

Growing Industrial Automation Demand

Commercial real estate developers are integrating DIN rail-mounted smart circuit breakers with cloud-based energy management platforms to enable tenant-level sub-metering and demand response automation. A 2024 smart electrical panel offers per-circuit monitoring and remote load shedding via mobile apps, targeting residential and light commercial retrofits in regions with time-of-use tariffs that incentivize load shifting. A 2025 Wi-Fi-enabled load center allows facility managers to prioritize critical loads during outages and integrates with HVAC and lighting systems to optimize peak demand charges and reduce operating costs.

India's power transmission sector is projected to invest USD 96.7 billion through 2032 to modernize distribution infrastructure, focusing on smart meters and automated feeder switches that rely on DIN rail-mounted communication modules. A 2025 SF6-free primary switchgear platform uses dry-air insulation and modular DIN-rail-mounted auxiliary relays, reducing the installation footprint by 30% compared to gas-insulated systems. The convergence of building automation and electrical distribution is driving demand for hybrid devices combining circuit protection with Ethernet or Modbus connectivity, enabling predictive maintenance through current signature analysis.

Surge in Renewable Energy Integration

Utility-scale solar and wind installations increasingly standardize on DIN-rail residual-current devices, DC-rated breakers, and transfer switches to protect inverter strings from ground faults and maintain stable grid synchronization. ZIV Automation supplied 1,000 IEC 61850-enabled protective relays to Spanish renewable parks in 2025, enabling remote configuration and faster fault isolation. ABB emphasizes Type B residual current breakers for EV and renewable systems, given their ability to detect DC leakage that conventional AC devices miss. Dubai Electricity and Water Authority is allocating AED 7.6 billion (USD 2.1 billion) to 49 substations incorporating DIN-rail disconnects, reinforcing grid expansion. Siemens's SENTRON 3QD2 (2026) extends protection up to 1,000 VDC in combiner boxes. Net effect: higher-spec, DC-capable protection becomes baseline as renewable penetration rises, increasing per-install value of DIN-rail components while tightening compliance requirements.

Volatility in Raw Material Prices

Copper and silver typically account for 25%-35% of a breaker's bill of materials, making gross margins highly sensitive to commodity volatility. In 2024, silver exhibited intraday price swings of> 3%, forcing quarterly repricing and shortening quote validity windows. DaDa Electric reported copper-driven supply shocks that extended order lead times by ~6 weeks in 2025. Vexos cited ~180 basis points of margin erosion, accelerating a shift toward silver-cadmium oxide contacts, which are ~20% cheaper while maintaining arc-quenching performance. Mitigation levers include multi-year metal hedging contracts and substitution with copper-clad aluminum busbars; however, material changes trigger requalification under UL 508 and IEC 60947, extending time-to-market and adding compliance cost. Net effect: pricing power becomes conditional on contract structure and certification agility, not just scale.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart Buildings Infrastructure

- Increasing Adoption of Modular Electrical Components

- Compatibility Issues with Legacy Panels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Circuit breaker switches held 42.61% revenue share in 2025, reflecting their core role in motor control centers and distribution boards where overcurrent protection is non-negotiable. Growth, however, is shifting toward residual-current devices, projected to grow at a 10.80% CAGR, driven by compliance mandates such as NEC Article 625 and IEC 60364 for EV chargers and PV systems. This structurally elevates leakage-detection requirements, especially under DC-rich loads. Multifunction devices such as ABB's DS301C combine overcurrent and residual protection in a single 35 mm DIN module, reducing panel width by ~50% and simplifying wiring. Net implication: mix shift toward higher-value, compliance-driven protection devices increases revenue per panel despite stable unit volumes.

Rotary cam, isolator, and transfer switches remain application-specific, supporting lockout-tagout procedures and source switching, but benefit from standardized DIN-rail integration that simplifies installation and maintenance. Bender's MRCD platform provides 30 mA-300 mA sensitivity with Type B DC detection, addressing leakage risks in bidirectional EV chargers and inverter-fed systems. Siemens's SENTRON 3VU13 motor starter integrates thermal overload and phase-loss protection, reducing component count and commissioning time. Increasing DC harmonics from variable-frequency drives are accelerating migration from Type AC to Type A and Type S devices, aligning protection characteristics with modern load profiles and tightening safety compliance thresholds.

The up to 250 VAC class accounted for 57.23% of revenue in 2025, anchored in single-phase residential and light-commercial circuits that remain the installed base for DIN rail systems. However, demand above 500 VAC is expanding at 9.60% CAGR as data centers and industrial microgrids standardize on 480 VAC and 690 VAC to reduce I2R losses and improve transmission efficiency. This structurally shifts the mix toward higher-voltage protection components. Siemens's 3QD2 breaker extends protection to 1,000 VDC photovoltaic strings, addressing arc-quenching limitations in conventional AC devices. Net effect: while low-voltage volumes remain stable, revenue growth is increasingly driven by high-voltage and DC-capable protection, raising average selling prices and technical specifications.

Medium-voltage build-outs are increasingly converging with low-voltage architectures, blurring traditional panel segmentation. Eaton's USD 30 million Nebraska production line targets 13.8 kV-34.5 kV equipment, yet continues to integrate DIN-rail-mounted auxiliary relays for control functions. Schneider Electric's Ringmaster AirSeT switchgear replaces SF6 with dry-air insulation while retaining modular rail-based relay integration, supporting compliance without requiring workforce retraining. Hybrid switchboards now combine 690 VAC feeders with 13.8 kV transformer sections, leveraging a unified DIN-rail ecosystem to standardize spares, reduce maintenance complexity, and shorten service intervals.

Complete Report Scope:

- By Switch Type

- Circuit Breaker Switches

- Isolator / Disconnect Switches

- Transfer Switches

- Rotary Cam Switches

- Residual Current Switches

- Other Switch Types

- By Voltage Rating

- Up to 250 VAC

- 251-500 VAC

- Above 500 VAC

- By End-User Industry

- Industrial Automation

- Energy and Power

- Building and Construction

- Transportation

- Telecommunications

- Other End-User Industries

- By Sales Channel

- Direct (OEM)

- Distributors / Wholesalers

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific generated 34.96% of 2025 revenue, anchored by China's smart-factory mandates, India's grid expansion programs, and Southeast Asia's manufacturing scale-up. Policy-led electrification and automation are structurally increasing demand for DIN-rail-mounted protection and control devices across factories, utilities, and commercial infrastructure. China's push for digitally managed industrial plants and India's transmission and distribution upgrades are expanding the installed base, while ASEAN nations are attracting electronics and automotive assembly capacity that standardizes on modular rail systems. The Middle East is the fastest-growing region, with a 9.03% CAGR, led by Saudi Arabia's NEOM and the UAE's Dubai 2040 initiatives, both of which embed IEC-compliant switchgear across substations, buildings, and water infrastructure, sustaining long-term demand growth.

North America's growth is tied to data-center expansion, industrial reshoring, and grid hardening investments that require high-reliability, code-compliant switchgear. Rockwell Automation's planned Wisconsin facility and Siemens' U.S. manufacturing footprint in Texas and California reinforce domestic supply chains for breakers and control gear. These investments align with the rising demand for 480 VAC systems in hyperscale data centers and distributed energy resources. Europe is undergoing a technology-driven replacement cycle as SF6 phase-out regulations accelerate adoption of compact, environmentally compliant alternatives such as Schneider Electric's GM AirSeT, which integrates DIN-rail relays with dry-air insulation to meet sustainability mandates without compromising performance.

South America and Africa present asymmetric opportunities. In South America, mining operations are deploying hybrid solar-diesel microgrids that rely on DIN-rail transfer switches and protection devices to manage variable generation and remote operations. This creates demand for rugged, field-serviceable components with high DC tolerance. Africa's electrification initiatives offer long-duration growth potential as grid access expands, but execution risk remains elevated due to counterfeit product inflows and inconsistent enforcement of IEC standards. Net implication: while emerging markets expand volume, suppliers must balance growth with risk controls, including certification traceability, local partnerships, and anti-counterfeit strategies to protect brand integrity and compliance.

- ABB Ltd.

- Schneider Electric SE

- Siemens AG

- Eaton Corporation plc

- Rockwell Automation Inc.

- Phoenix Contact GmbH & Co. KG

- WAGO Kontakttechnik GmbH & Co. KG

- Legrand SA

- Hager Group

- Mitsubishi Electric Corporation

- Omron Corporation

- Carlo Gavazzi Holding AG

- Weidmuller Interface GmbH & Co. KG

- Finder SpA

- LS ELECTRIC Co., Ltd.

- E-T-A Elektrotechnische Apparate GmbH

- Altech Corporation

- IDEC Corporation

- Mersen SA

- LOVATO Electric S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Industrial Automation Demand

- 4.2.2 Surge in Renewable Energy Integration

- 4.2.3 Expansion of Smart Buildings Infrastructure

- 4.2.4 Increasing Adoption of Modular Electrical Components

- 4.2.5 Rising Safety Regulations for Low-Voltage Installations

- 4.2.6 Rapid Growth of E-Commerce Distribution Channels

- 4.3 Market Restraints

- 4.3.1 Volatility in Raw Material Prices

- 4.3.2 Compatibility Issues with Legacy Panels

- 4.3.3 Counterfeit Low-Cost Products Undermining Quality

- 4.3.4 Skilled Labor Shortage for Precision Panel Assembly

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Circuit Breaker Switches

- 5.1.2 Isolator / Disconnect Switches

- 5.1.3 Transfer Switches

- 5.1.4 Rotary Cam Switches

- 5.1.5 Residual Current Switches

- 5.1.6 Other Switch Types

- 5.2 By Voltage Rating

- 5.2.1 Up to 250 VAC

- 5.2.2 251-500 VAC

- 5.2.3 Above 500 VAC

- 5.3 By End-User Industry

- 5.3.1 Industrial Automation

- 5.3.2 Energy and Power

- 5.3.3 Building and Construction

- 5.3.4 Transportation

- 5.3.5 Telecommunications

- 5.3.6 Other End-User Industries

- 5.4 By Sales Channel

- 5.4.1 Direct (OEM)

- 5.4.2 Distributors / Wholesalers

- 5.4.3 E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Schneider Electric SE

- 6.4.3 Siemens AG

- 6.4.4 Eaton Corporation plc

- 6.4.5 Rockwell Automation Inc.

- 6.4.6 Phoenix Contact GmbH & Co. KG

- 6.4.7 WAGO Kontakttechnik GmbH & Co. KG

- 6.4.8 Legrand SA

- 6.4.9 Hager Group

- 6.4.10 Mitsubishi Electric Corporation

- 6.4.11 Omron Corporation

- 6.4.12 Carlo Gavazzi Holding AG

- 6.4.13 Weidmuller Interface GmbH & Co. KG

- 6.4.14 Finder SpA

- 6.4.15 LS ELECTRIC Co., Ltd.

- 6.4.16 E-T-A Elektrotechnische Apparate GmbH

- 6.4.17 Altech Corporation

- 6.4.18 IDEC Corporation

- 6.4.19 Mersen SA

- 6.4.20 LOVATO Electric S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment