PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073368

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073368

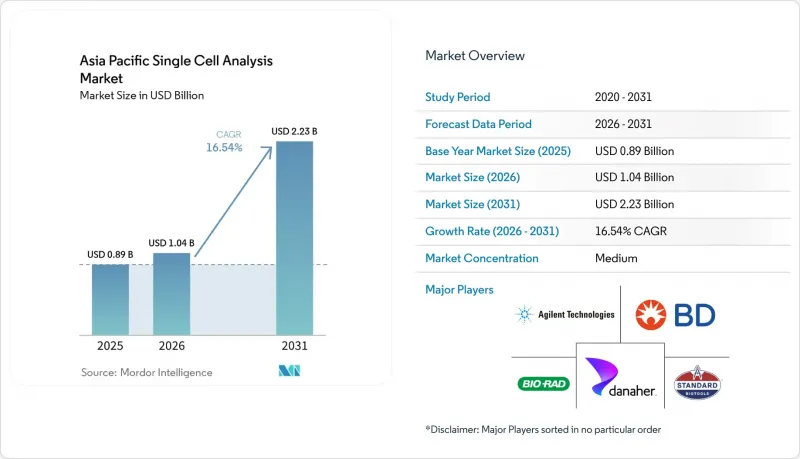

Asia Pacific Single Cell Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, asia pacific single cell analysis market size in 2026 is estimated at USD 1.04 billion, growing from 2025 value of USD 0.89 billion with 2031 projections showing USD 2.23 billion, growing at 16.54% CAGR over 2026-2031.

This report Segments the Industry Into Technique (Flow Cytometry, Next Generation Sequencing, Polymerase Chain Reaction (PCR), Microscopy, and More), Application (Research Applications, Medical Applications), End User (Academic and Research Laboratories, and More), and Country (China, Japan, India, and More).

Asia Pacific Single Cell Analysis Market Trends and Insights

Technological advancements in single-cell analysis products

Rice University engineers created a gravity-driven microfluidic chip that removes pump hardware yet still counts CD4+ T cells accurately, showing how engineering tweaks lower capital thresholds for emerging labs . BD's CellView Image Technology now sorts by visual features, unlocking richer phenotypes that traditional fluorescence could miss. China's Institute of Automation introduced FlowRACS 3.0, using deterministic lateral displacement to condense microbial strain screening from months to days. 10x Genomics' GEM-X Flex chemistry aims for one-cent per-cell reagent costs, signalling a decisive shift toward mass-scale affordability. Together these upgrades position the single cell analysis market for accelerated platform turnover and broader laboratory reach.

Increasing investments in cancer research

Illumina is bankrolling the Garvan Institute's TenK10K study, mapping 50 million human cells to uncover cancer-linked genomic fingerprints . South Korea's K-MASTER network screened 994 metastatic colorectal cancer cases and found 52.8% actionable mutations, underscoring direct clinical utility. Korean scientists applied single-cell RNA sequencing to chemotherapy-resistant bladder cancer and isolated resistance pathways now under therapeutic review. Spatial genomics and transcriptomics is connecting tumor micro-environment features with relapse risk, amplifying demand for integrated platforms in the single cell analysis market.

High cost of single-cell analysis instruments

BD's biosciences division logged USD 3.4 billion revenue in 2024 yet still moved to spin out, highlighting the capital-intensive nature of instrument R&D. 10x Genomics responded with Chromium Xo, a leaner model for budget conscious users. Consumable spend, service contracts, and staff training add hidden burdens, pushing universities toward shared core facilities. Core sharing tempers purchasing cycles and can slow experimental throughput, highlighting a price-elastic segment within the single cell analysis market.

Other drivers and restraints analyzed in the detailed report include:

- Rising prevalence of chronic diseases

- Growing adoption of spatial transcriptomics integrations

- Limited computational & bioinformatics expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and consumables supplied 57.62% of 2025 revenue as each run requires proprietary cartridges, beads, or reagent kits. The recurring model stabilizes vendor cash flow and anchors long-term customer relationships inside the single cell analysis market. Instruments, however, register a 17.08% CAGR through 2031 because new optical, microfluidic, and imaging features allow deeper phenotyping. BD's FACSDiscover A8 now maps over 50 parameters in real time, expanding the single cell analysis market size for high-dimensional cytometry. Automation agreements with robotics makers shorten setup times and lift reproducibility, factors that nudge laboratories toward upgrades. Software and services remain comparatively small but are strategic funnels that lock users into vendor ecosystems by handling data pipelines and compliance documentation.

The rising instrument curve is reinforced by active-pixel semiconductor designs from Chinese startup Aosuo Technology, which promises faster protein quantification at lower luminosity errors. Such advances encourage mid-tier hospitals to step up from shared facilities to in-house units, widening geographic reach of the single cell analysis market. Vendors bundling consumables with service contracts cushion price sensitivity and foster predictable reagent consumption. This synergy keeps consumables at the revenue core even as instrument fleets modernize.

Flow cytometry carried 34.12% technique share in 2025 by virtue of embedded lab infrastructure and decades-old protocols that technicians master early in their careers. Multilaser spectral systems boost channel counts without fluor overlap, supporting intricate immunophenotyping. Meanwhile, next-generation sequencing books the fastest 16.89% CAGR, reflecting plunging read costs and the allure of transcriptome-wide coverage. The single cell analysis market thus aligns along two poles: high-throughput sorting on one side and deep genomic insight on the other.

Hybrid systems are bridging the divide. Takara Bio's Shasta platform pre-enriches cells, then funnels them straight to automated NGS, collapsing sample-to-data time. Microfluidic slips from Toyohashi University push 95% cell viability in drug screens, signalling a future where gentle handling couples with sequencing depth. As sequencing output soars, laboratory planners must weigh data-storage overheads against biological payoff, a calculus that increasingly guides capital budgets within the single cell analysis market.

Complete Report Scope:

- By Product Type

- Instruments

- Reagents & Consumables

- Software & Services

- By Technique

- Flow Cytometry

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Microscopy

- Mass Spectrometry

- Microfluidics-based Platforms

- By Application

- Research Applications

- Medical/Clinical Diagnostics

- By Disease Area

- Oncology

- Immunology & Autoimmune Disorders

- Neurology

- Infectious Diseases

- Other Disease Areas

- By Workflow Stage

- Single-Cell Isolation & Preparation

- Library Preparation & Amplification

- Sequencing/Detection

- Data Analysis & Interpretation

- By End User

- Academic & Research Laboratories

- Biotechnology & Pharmaceutical Companies

- Hospital & Diagnostic Laboratories

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- 10x Genomics

- Agilent Technologies

- Beckton Dickinson

- Beckton Dickinson

- Bio-Rad Laboratories

- Standard BioTools (Fluidigm)

- Illumina

- Merck

- QIAGEN

- Thermo Fisher Scientific

- Takara Bio

- Bio-Techne Corp. (ProteinSimple)

- Menarini

- On-chip Biotechnologies Co. Ltd.

- Parse Biosciences

- Mission Bio Inc.

- Cytena GmbH

- Dolomite Bio

- Namocell

- RareCyte Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological advancements in single-cell analysis products

- 4.2.2 Increasing investments in cancer research

- 4.2.3 Rising prevalence of chronic diseases

- 4.2.4 Growing adoption of spatial transcriptomics integrations

- 4.2.5 Government-backed cell & gene-therapy manufacturing hubs

- 4.2.6 Academic-industry microfluidic collaborations reduce cost per cell

- 4.3 Market Restraints

- 4.3.1 High cost of single-cell analysis instruments

- 4.3.2 Limited computational & bioinformatics expertise

- 4.3.3 Regulatory uncertainty around multi-omics data privacy

- 4.3.4 Supply-chain dependence on US-made precision fluidic chips

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Reagents & Consumables

- 5.1.3 Software & Services

- 5.2 By Technique

- 5.2.1 Flow Cytometry

- 5.2.2 Next-Generation Sequencing (NGS)

- 5.2.3 Polymerase Chain Reaction (PCR)

- 5.2.4 Microscopy

- 5.2.5 Mass Spectrometry

- 5.2.6 Microfluidics-based Platforms

- 5.3 By Application

- 5.3.1 Research Applications

- 5.3.2 Medical/Clinical Diagnostics

- 5.4 By Disease Area

- 5.4.1 Oncology

- 5.4.2 Immunology & Autoimmune Disorders

- 5.4.3 Neurology

- 5.4.4 Infectious Diseases

- 5.4.5 Other Disease Areas

- 5.5 By Workflow Stage

- 5.5.1 Single-Cell Isolation & Preparation

- 5.5.2 Library Preparation & Amplification

- 5.5.3 Sequencing/Detection

- 5.5.4 Data Analysis & Interpretation

- 5.6 By End User

- 5.6.1 Academic & Research Laboratories

- 5.6.2 Biotechnology & Pharmaceutical Companies

- 5.6.3 Hospital & Diagnostic Laboratories

- 5.7 By Country

- 5.7.1 China

- 5.7.2 Japan

- 5.7.3 India

- 5.7.4 South Korea

- 5.7.5 Australia

- 5.7.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 10x Genomics

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Beckman Coulter Inc. (Danaher)

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Bio-Rad Laboratories Inc.

- 6.3.6 Standard BioTools (Fluidigm)

- 6.3.7 Illumina Inc.

- 6.3.8 Merck KGaA

- 6.3.9 Qiagen NV

- 6.3.10 Thermo Fisher Scientific Inc.

- 6.3.11 Takara Bio Inc.

- 6.3.12 Bio-Techne Corp. (ProteinSimple)

- 6.3.13 Menarini Silicon Biosystems

- 6.3.14 On-chip Biotechnologies Co. Ltd.

- 6.3.15 Parse Biosciences

- 6.3.16 Mission Bio Inc.

- 6.3.17 Cytena GmbH

- 6.3.18 Dolomite Bio

- 6.3.19 Namocell Inc.

- 6.3.20 RareCyte Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment