PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959294

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959294

Plant-based Colors from Food Waste Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

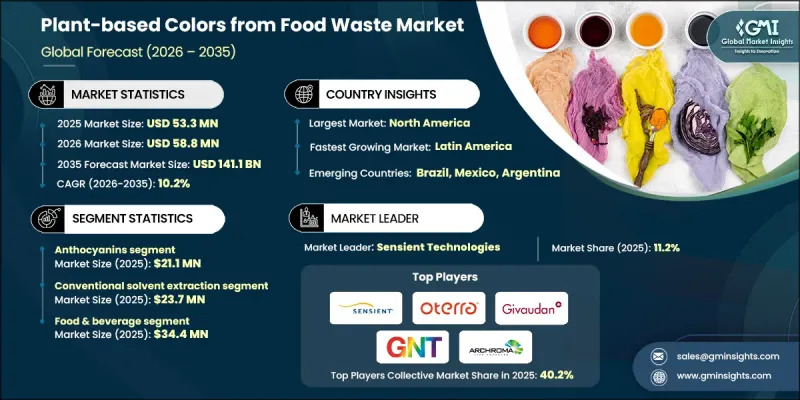

The Global Plant-based Colors from Food Waste Market was valued at USD 53.3 million in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 141.1 million by 2035.

The market focuses on natural pigments recovered from discarded plant materials generated during food processing and post-harvest handling. These colorants are extracted from underutilized plant fractions and transformed into commercially viable ingredients for multiple industries. Key pigment groups include anthocyanins, carotenoids, chlorophylls, and betalains, which are recovered through specialized processing techniques designed to preserve color intensity and functional stability. Converting plant-based waste streams into natural color solutions supports circular economy objectives by reducing landfill burden and lowering reliance on synthetic dyes. In addition to environmental benefits, these pigments often contain bioactive compounds with antioxidant and antimicrobial properties, enhancing their value proposition. The approach creates new revenue channels for agricultural and food-processing industries while improving resource efficiency. Rising consumer demand for transparency, clean-label formulations, and non-toxic ingredients is accelerating adoption across food, textile, cosmetic, and packaging applications. As sustainability becomes central to brand identity, plant-based colors sourced from food waste are gaining strategic importance in global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.3 Million |

| Forecast Value | $141.1 Million |

| CAGR | 10.2% |

Natural pigments derived from food waste are increasingly preferred as consumers seek environmentally responsible and biodegradable alternatives to artificial dyes. Clean-label positioning, regulatory shifts away from synthetic additives, and growing awareness of product safety are reinforcing this transition. Unlike conventional synthetic colorants, plant-based pigments align with eco-conscious branding and wellness-driven purchasing behavior. Their renewable origin and reduced environmental footprint make them attractive to manufacturers focused on sustainable innovation.

The conventional solvent extraction segment accounted for USD 23.7 million in 2025. This method remains widely utilized due to its operational simplicity, cost-effectiveness, and relatively low capital requirements. It continues to support large-scale pigment recovery, particularly in emerging markets where infrastructure constraints influence technology adoption. However, industry participants are increasingly evaluating advanced extraction approaches to improve yield efficiency, reduce solvent residues, and minimize environmental impact while maintaining pigment quality and stability.

The food & beverage segment generated USD 34.4 million in 2025. Strong growth in this sector is driven by consumer demand for ingredient transparency and traceable sourcing. Manufacturers are incorporating food waste-derived plant-based colors into product formulations to replace synthetic alternatives and meet regulatory standards. These natural pigments deliver vibrant visual appeal across beverages, dairy products, snacks, and confectionery applications while reinforcing sustainability narratives. As brands emphasize responsible sourcing and cleaner formulations, demand within the food and beverage industry continues to strengthen.

North America Plant-based Colors from Food Waste Market is projected to grow from USD 22 million in 2025 to USD 50.8 million by 2035. Regional expansion is supported by heightened consumer awareness regarding natural ingredients and strong industry commitment to environmental stewardship. Food, beverage, and cosmetic manufacturers are investing in technologies that convert agricultural by-products into high-value pigments to advance circular production goals. Regulatory initiatives aimed at reducing synthetic additive usage further stimulate market growth. Established supply chains and innovation-driven business models position North America as a key contributor to global revenue expansion.

Major companies operating in the Global Plant-based Colors from Food Waste Market include GNT Group, Sensient Technologies Corporation, Chr. Hansen Holdings (Oterra), Givaudan SA, Givaudan Sense Colour, Archroma (EarthColors), Prodalim (Upcycled Colors), E. & J. Gallo Winery (Natural Colorants Division), and KAIKU (UK). These organizations are actively developing advanced pigment extraction technologies and expanding sustainable ingredient portfolios to strengthen their competitive presence. Companies in the plant-based colors from food waste market are reinforcing their market position through investment in research and development to improve pigment stability, color intensity, and application versatility. Strategic collaborations with food processors and agricultural suppliers secure consistent raw material streams and enhance traceability. Many firms are adopting proprietary extraction technologies that increase yield efficiency while reducing environmental impact. Sustainability certifications and transparent sourcing practices are being leveraged to build brand credibility and consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Pigment Type

- 2.2.2 Extraction Technology

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural colors

- 3.2.1.2 Expansion of plant-based and clean-label products

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Competitive pressure from synthetic colors

- 3.2.3 Market opportunities

- 3.2.3.1 Integration into cosmetic and pharmaceutical industries

- 3.2.3.2 Collaborations with food processing companies

- 3.2.3.3 Innovation in functional colors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Pigment type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Pigment Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Anthocyanins

- 5.3 Betalains

- 5.4 Carotenoids

- 5.5 Chlorophylls

- 5.6 Phycobiliproteins

Chapter 6 Market Estimates and Forecast, By Extraction Technology, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional solvent extraction

- 6.3 Ultrasound-assisted extraction (UAE)

- 6.4 Microwave-assisted extraction (MAE)

- 6.5 Supercritical fluid extraction (SFE)

- 6.6 Enzyme-assisted extraction (EAE)

- 6.7 Pulsed electric field (PEF)

- 6.8 Pressurized liquid extraction (PLE)

- 6.9 Precision fermentation & biotechnology

- 6.10 Hybrid & integrated extraction systems

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Textile & fashion

- 7.5 Pharmaceutical & nutraceutical

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Sensient Technologies Corporation

- 9.2 Chr. Hansen Holdings (Oterra)

- 9.3 Givaudan SA

- 9.4 Givaudan Sense Colour

- 9.5 GNT Group

- 9.6 Archroma (EarthColors)

- 9.7 Prodalim (Upcycled Colors)

- 9.8 E. & J. Gallo Winery (Natural Colorants Division)

- 9.9 KAIKU (UK)