PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063891

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063891

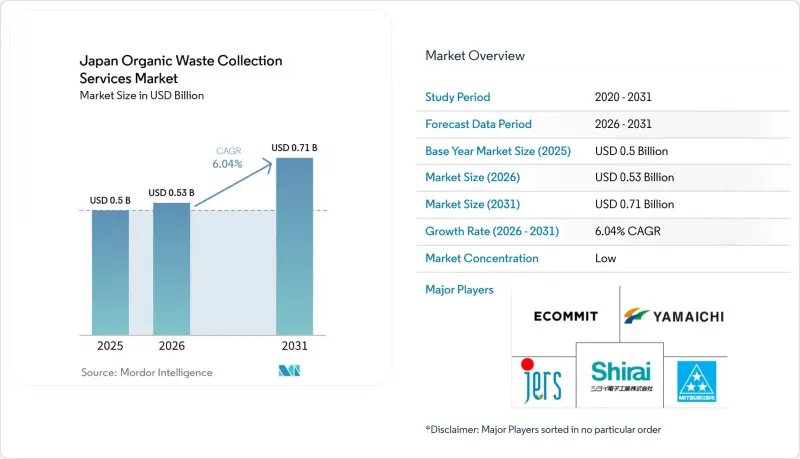

Japan Organic Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan organic waste collection services market size is projected to be USD 0.5 billion in 2025, USD 0.53 billion in 2026, and reach USD 0.71 billion by 2031, growing at a CAGR of 6.04% from 2026 to 2031.

This report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), by End-User (Residential, Commercial, and More), by Collection Method (Door-To-Door Collection, and More), by Technology & Equipment (Manual Collection Systems, Semi-Automated Systems, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Japan Organic Waste Collection Services Market Trends and Insights

Stringent Government Regulations on Waste Segregation and Recycling

Policy momentum accelerated in 2024 and 2025 with new resource-circulation measures and related enforcement that require clearer reporting on recycling implementation and tighter controls on treatment outcomes. These measures pressure organic waste collectors and processors to improve segregation quality and document outcomes with more detailed manifests and auditable data trails. Planned updates scheduled to take effect around 2026 are also expected to broaden permit regimes for higher-risk materials, reducing mis-sorting and contamination risks in organics flows at the point of intake. In parallel, food-loss and food-recycling policy updates effective in 2025 are pushing enterprises to separate edible surplus from inedible streams and to disclose volumes more consistently, thereby improving upstream quality for separate collection. Together, these shifts translate into higher demand for telemetry, tagging, and container-level verification, enabling haulers to demonstrate segregation quality while lowering treatment risk and supporting national circularity goals.

Growing Emphasis on Circular Economy Initiatives

Japan has elevated the circular economy to a national strategic pillar, framing organics as a priority feedstock for renewable energy and soil health outcomes. Municipal case studies demonstrate that systematic separation, collection, and localized processing can scale when programs are designed around clear rules, stable offtake, and practical cost controls. These models favor defined organic pathways that return compost and digestate-derived nutrients to nearby farms, enabling short-haul logistics and more resilient agricultural loops. The Japan organic waste collection service market gains from this policy alignment because municipalities now have clearer targets, better precedent templates, and a stronger rationale for budget proposals tied to organics recovery projects. The Ministerial Council on the Circular Economy also signaled harmonization with global disclosure and recycling standards, which nudges enterprises to upgrade data capture across their waste chains. This convergence encourages standardized reporting from haulers and processors, in turn strengthening the investment case for specialized collection services for food waste.

High Initial Investment Costs for Collection Infrastructure and Vehicles

Capital requirements for new waste treatment and recycling facilities continue to strain municipal finances, even when subsidies are available. Large-scale energy recovery and recycling plants often create multi-decade debt service commitments after accounting for grants, bonds, and general revenue allocations. Site preparation, footprint constraints, and phasing requirements can add to procurement burden and extend payback periods. On the fleet side, EV refuse vehicles and modern compaction bodies can improve emissions performance and routing outcomes, but higher upfront costs increased reliance on leasing and phased deployments. As a result, adoption curves can diverge between cash-rich urban districts and smaller municipalities facing shrinking tax bases. Operators are responding by rolling out modular equipment in phases and prioritizing pilots that deliver quick wins in the organics fraction, building support for subsequent capital phases.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Biomass Energy Generation from Organic Waste

- Expansion of Composting Facilities and Biogas Plants

- Limited Land Availability for Waste Processing Facilities in Urban Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food waste held 69.2% share in 2025 and is forecast to grow at a 6.78% CAGR through 2031, reflecting regulatory pressure and operational changes in how surplus is handled and disclosed. Policy updates are encouraging retailers and food-service operators to prioritize donating edible surplus, extend shelf life where feasible, and separate edible from inedible streams at source, thereby improving upstream quality for separate collection. These dynamics favor urban curbside programs and contracted pickups for supermarkets, convenience chains, and cafeterias that can maintain high segregation standards and stable volumes. In parallel, projects that convert fermentation residue to fertilizer or other usable outputs strengthen offtake certainty, improving the economics of recurring organics routes.

Yard and landscape waste, as well as agricultural residues, follow distinct logistics patterns. Yard waste is seasonal and aligns with periodic collections and compost-site throughput constraints. In rural prefectures, crop residues may be integrated into digesters or compost systems that feed nutrients back to farms, often through circular-agriculture pilots. Miscellaneous organic streams, such as fish-processing byproducts or brewery residues, can also be captured where local operators have a reliable offtake for feed, compost, or biogas applications. While priorities vary by region, the overall direction remains consistent: more defined collection points, clearer contamination rules, and more predictable offtake especially for food waste, which accounts for most revenue.

Residential generators accounted for 54.7% of demand in 2025 and continue to underpin base route density in cities and towns. Household incentives in select municipalities (such as subsidies for home processing containers) can reduce curbside volumes and contamination, improving routing and capacity planning. Commercial segments are expanding faster, at a 7.21% CAGR, as supermarkets, restaurant groups, and large canteens embed organic recovery into ESG programs and cost-control initiatives. Commercial contracts increasingly route food scraps to biogas plants and use structured arrangements to return electricity value to participating sites, strengthening long-term demand for scheduled pickups and contamination-light streams.

Industrial food processors show similar momentum as they pursue decarbonization milestones and seek credible emissions reductions through energy recovery and return-power models. Collection providers support these users by synchronizing pickups with production cycles and integrating weight-based audits that connect waste data to internal reporting dashboards. Residential volumes will remain important for route efficiency, while faster commercial growth signals deeper integration of organics capture into occupational kitchens and national retail chains. This trend is steering investments toward urban transfer points and stronger data systems to meet customer reporting expectations and improve benchmarking across multi-site operators.

List of Companies Covered in this Report:

- ECOMMIT Co., Ltd.

- Mitsuboshi Sangyo Ltd.

- Shirai Group

- JERS Corporation

- J&T Recycling Corporation

- Green Power Co., Ltd.

- Japan Food Ecology Center, Inc

- Yokohama City Visitors Bureau

- KITA

- NTT Business Solutions Corporation

- Veolia

- TOYO ENERGY SOLUTION CO., LTD.

- Bio Energy Corporation

- DAIEI KANKYO

- Genesis Co., Ltd.

- Joetsu Materials Corporation

- Japan Waste Co.,Ltd.

- Sanimax

- TAKEEI CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Government Regulations on Waste Segregation and Recycling

- 4.2.2 Growing Emphasis on Circular Economy Initiatives

- 4.2.3 Increasing Adoption of Biomass Energy Generation from Organic Waste

- 4.2.4 Expansion of Composting Facilities and Biogas Plants

- 4.2.5 Government Subsidies and Incentives for Organic Waste Management

- 4.2.6 Growing Corporate ESG Commitments and Sustainability Reporting Requirements

- 4.3 Market Restraints

- 4.3.1 High Initial Investment Costs for Collection Infrastructure and Vehicles

- 4.3.2 Limited Land Availability for Waste Processing Facilities in Urban Areas

- 4.3.3 Seasonal Variations in Organic Waste Generation Affecting Operational Efficiency

- 4.3.4 Shortage of Skilled Workforce in the Waste Management Sector

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 RFID Smart Bins for Waste Tracking

- 4.6.2 AI Revolutionizes Waste Sorting

- 4.6.3 IoT Optimizing for Fleet Routes

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Fleet Modernization & Electrification in Waste Collection

- 4.9 Analysis of Biomethane Impact on Organic Waste Collection

- 4.10 Collaboration Between Municipalities and Private Operators Gaining Traction

- 4.11 Growing Focus on Methane Capture from Organic Waste to Meet Climate Targets

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial (HoReCa, Retail)

- 5.2.3 Industrial (Food Processing & Manufacturing)

- 5.2.4 Others (Agri-waste)

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Drop-Off / Bring Systems

- 5.3.3 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 ECOMMIT Co., Ltd.

- 6.4.2 Mitsuboshi Sangyo Ltd.

- 6.4.3 Shirai Group

- 6.4.4 JERS Corporation

- 6.4.5 J&T Recycling Corporation

- 6.4.6 Green Power Co., Ltd.

- 6.4.7 Japan Food Ecology Center, Inc

- 6.4.8 Yokohama City Visitors Bureau

- 6.4.9 KITA

- 6.4.10 NTT Business Solutions Corporation

- 6.4.11 Veolia

- 6.4.12 TOYO ENERGY SOLUTION CO., LTD.

- 6.4.13 Bio Energy Corporation

- 6.4.14 DAIEI KANKYO

- 6.4.15 Genesis Co., Ltd.

- 6.4.16 Joetsu Materials Corporation

- 6.4.17 Japan Waste Co.,Ltd.

- 6.4.18 Sanimax

- 6.4.19 TAKEEI CORPORATION

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

- 7.3 Shift Toward Decentralized Organic Waste Processing