PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063844

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063844

Organic Waste Collection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

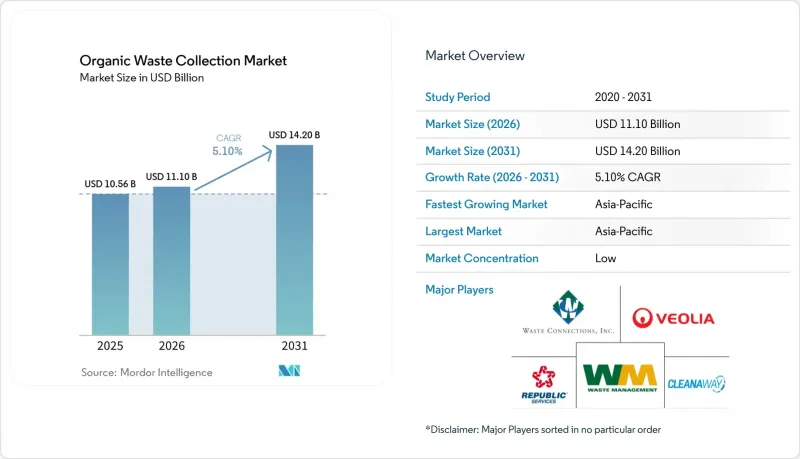

According to Mordor Intelligence, the organic waste collection market size is expected to grow from USD 10.56 billion in 2025 to USD 11.10 billion in 2026 and is forecast to reach USD 14.20 billion by 2031 at 5.10% CAGR over 2026-2031.

This report is Segmented by Waste Type (Food Waste, Yard Waste, and More), End-User (Residential, Commercial Food Service, and More), Collection Method (Door-To-Door, Drop-Off, Bulk, and Others), Technology (Manual, Semi-Automated, Fully Automated), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts in Value USD Billion and Volume (Tons)

Global Organic Waste Collection Market Trends and Insights

Stringent Government Regulations Mandating Organic Waste Segregation and Diversion from Landfills

Regulatory mandates are driving organics diversion by requiring separate biowaste collection and food waste reduction. The European Union's Waste Framework Directive, effective October 16, 2025, mandates a 10% reduction in food waste during processing and manufacturing and a 30% per capita reduction at retail and consumption by 2030, alongside consistent biowaste collection across Member States. In the United States, the February 2025 National Strategy for Reducing Food Loss and Waste allocates USD 275 million for organics recycling infrastructure under the Solid Waste Infrastructure for Recycling framework, supported by education and outreach grants. France will require gas suppliers to source biogas production certificates from 2026, ensuring demand for biomethane from organic waste. The Netherlands' 2026 biomethane grid-blending obligation will drive infrastructure investment, favoring low-contamination feedstock. However, uneven implementation persists, as an audit found low biowaste collection rates in three of four European Union Member States in 2022-2023, highlighting the need for enforcement, infrastructure, and public engagement.

Rising Urbanization Driving Higher Volumes of Municipal Organic Waste Generation

Population growth in large cities is concentrating organic waste streams in areas where route-based collection is operationally feasible, and capital spending can be justified, thereby expanding the addressable base for the organic waste collection market. UN DESA reports that cities housed nearly half of humanity in 2025, and that urban land area per person has expanded since 1975, which increases haul distances and creates new siting challenges that favor efficient routing and well-planned transfer points. The expected expansion of megacities across Asia increases waste generation, strengthening the economics of fully automated side-loading vehicles, smart containers, and performance-based service contracts in dense multi-user districts. The World Bank's work on solid waste management documents high levels of uncollected waste in lower-income settings, suggesting that the need for scalable, lower-cost organics collection models is most acute where city growth outpaces public budgets and collection coverage. As built-up areas expand faster than population, municipalities must plan for longer transport legs and more intermediate storage, which increases the value of contamination control and predictable scheduling to maintain feedstock quality for composting and digestion facilities. Regions with rapid urban growth and policy momentum, therefore, present the strongest conditions for new or expanded programs, which leads to a larger and more stable pipeline for the organic waste collection market.

Contamination of Organic Waste Streams Reducing Processing Efficiency

Contamination increases preprocessing requirements, reduces product quality, and constrains end-market applications, thereby limiting the value captured from compost and digestate and increasing disposal risk if facilities reject loads. Evidence from national studies shows that food and garden waste streams face contamination challenges that have trended upward in recent years, underscoring the need for targeted outreach, bin standards, and feedback loops to address behaviors. Local experience in the United States confirms that targeted crew intervention and tagging can significantly reduce curb contamination, benefit downstream facilities, and support steady operations when co-digestion or composting is part of the municipal treatment mix. Processing operators communicate that contamination thresholds drive acceptance decisions, which places a premium on reliable source segregation and clear material standards within service agreements to avoid expensive rejections and re-routing. Federal agencies flag plastics and persistent chemicals as ongoing barriers, and they are working to synthesize science and provide technical assistance, which should support more consistent practices and standards across jurisdictions. These dynamics favor providers that combine service design with data-driven outreach and clear customer feedback, which can produce measurable reductions in contamination and higher-value outputs over time.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Circular Economy Principles and Waste-to-Energy Initiatives

- Growing Environmental Awareness and Corporate Sustainability Commitments

- Lack of Public Awareness and Low Participation Rates in Source Segregation Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Yard and Landscape Waste accounted for 52.2% of the organic waste collection market in 2025, reflecting long-standing seasonal programs and the relatively lower contamination inherent to outdoor green waste streams collected through well-understood municipal routes. Food Waste, covering pre-consumer and post-consumer sources, is projected to grow at a 5.78% CAGR through 2031 as separate food waste collection requirements in European Member States and the United Kingdom mature and expand to more local jurisdictions, increasing the share of putrescible material served by dedicated routes and service days. India has mandated four-stream source segregation under rules that take effect in 2026, elevating wet waste to a specific category in city plans and gradually scaling food waste capture as compliance increases. Agricultural Residues create sizable regional opportunities tied to livestock and crop systems, with projects that combine manure and crop wastes to produce biogas and compost-grade outputs under controlled conditions and steady feedstock contracts. Bio-Sludge and Wastewater Organics continue to provide integration points for co-digestion at water resource recovery facilities, which can absorb collected food waste to increase gas yields where plant design and permit conditions allow.

Food Waste growth will be supported by the expansion of citywide residential programs and by commercial organics mandates that define collection service expectations and reporting cadence for food service operators, helping maintain growth momentum even as yard waste remains the largest stream by volume in many jurisdictions. Dedicated digestion assets and long-term composting outlets are needed to handle forecast increases in Food Waste tonnage, which favors haulers and municipalities that pre-negotiate off take or maintain equity in local processing capacity to stabilize tipping fee exposure. Commercial Organics that are not food-related remain small but valuable, since they often consist of homogeneous, single-source streams that are easier to process and can be contracted on stable schedules, thereby improving route density and fleet utilization. As mandates settle and enforcement increases, the organic waste collection industry will likely prioritize service tiers, container standards, and packaging controls that reduce contamination and increase the throughput and value of downstream products.

Residential households accounted for 54.1% of collected volumes in 2025, reflecting the reach of municipal curbside systems and cart-based programs that standardize pickups across neighborhoods and support regular participation through simple rules and clear bin colors. Commercial Food Service is the fastest-growing end-user group, with a 6.23% CAGR through 2031, as restaurants, institutional cafeterias, and hospitality venues consolidate high volumes at fewer pickup points, reducing the per-ton cost of service and supporting cleaner streams through staff training and account-level feedback. Jurisdictions that define bulk waste generators and require onsite processing or verified off site diversion create compliance-driven demand that locks in recurring service days, documented tonnage, and contamination oversight for large generators in food service and institutional settings. The organic waste collection market benefits from these rules because they create regular demand and measurable performance, which justify route investments and staff training that improve yield and data quality over time.

Food Processing and Manufacturing offers high-volume, homogeneous streams that are simpler to segregate and collect, which supports steady co digestion yields and consistent compost inputs when contamination is controlled at the source. Retail and Grocery networks are formalizing partnerships for redistribution, animal feed, and composting, which reduce edible waste while moving inedible materials into diversion channels that depend on reliable collection and predictable pickup windows. Schools and other public institutions are accessing dedicated grants to reduce food waste, which helps pay for bins, training, and initial collection services that transition pilot efforts into standing programs with measurable outcomes. As reporting expectations tighten across sectors, the organic waste collection industry will create value for end users by combining curbside or dockside pickups with digital verification, contamination alerts, and basic analytics that link training to improved diversion rates.

Geography Analysis

Asia-Pacific accounted for 33.2% of the organic waste collection market size in 2025 and is projected to be the fastest growing region at a 7.54% CAGR through 2031, driven by large population centers, mandatory source segregation rules, and national biomethane blending obligations that formalize offtake pathways for collected organics. Policy signals in China and India are strengthening alignment between collection programs and downstream gas markets, encouraging investment in digestion assets as cities build curbside or commercial pickup coverage in step with facility capacity. Japan's progress on food waste reduction in the business sector illustrates how mandatory measurement and clear targets can guide private investment and shape supplier expectations, benefiting service providers that can deliver consistent hauling with accurate reporting. Rapid growth in megacities across Asia supports route density and favors technology-enabled fleets, which raises the likelihood that fully automated vehicles and bin sensors will move from pilots to baseline practice over the forecast period.

Europe combines mature regulation with active investment in biomethane production and composting capacity, which provides strong signals for municipalities and private haulers to expand separate collection coverage and reduce contamination. The revised Waste Framework Directive establishes food waste reduction targets and separate biowaste collection, which anchors growth in residential and commercial organics programs and positions the region to absorb collected streams in line with capacity additions. Sector data confirm a rapid buildout of biomethane plants and long-term investment commitments. However, production and capacity additions need to accelerate to meet 2030 targets, suggesting that continued policy support and certificate systems will help bridge the gap. Audits show uneven implementation across some Member States, suggesting that enforcement, landfill pricing, and cost-recovery mechanisms need to be strengthened to unlock the full potential of the organic waste collection market. These findings support focused investments in collection coverage, communications, and contamination reduction to meet legal targets and stabilize feedstock flows to digesters and compost sites.

North America mixes strong state-level mandates with federal grant support and voluntary frameworks, which yield a patchwork of program maturity across states and provinces that is moving toward broader coverage. U.S. federal funding through the Solid Waste Infrastructure for Recycling program includes allocations for organics recycling infrastructure, which reduces capital hurdles and enables cities to scale collection services with better equipment and processing contracts. Large city rollouts demonstrate operational feasibility at scale when staffing, trucks, and processing are aligned and when resident education is steady, which supports the broader case for universal curbside coverage for organics over time. Canada is adding digestion capacity in key provinces through partnerships backed by long-term gas off take, which should strengthen the market for contracted organics collection services as new sites come online. The Middle East and Africa face higher rates of mismanagement and limited recycling and composting. Still, regional strategies to diversify energy supply and reduce food waste are taking shape, opening the door to targeted projects in urban centers that can combine organic collection with digestion under supportive feed-in tariffs and clean cooking policies. South America is advancing legal frameworks that monetize biomethane and bring landfill gas and organics to market under renewable and decarbonization rules, which aligns municipal collection expansions with long-term fuel demand.

- Republic Services

- Veolia

- Waste Management (WM)

- Waste Connections

- Cleanaway

- Sanimax

- Shapiro (Skip Shapiro Enterprises)

- Biotic Waste Limited

- Compost Crew

- Circular Services

- Emterra USA

- Keenan Recycling (Biffa Company)

- Grundon

- GAP Organics

- Monster Organics

- Recology

- Royal Waste Services

- Total Organics Recycling

- Groot Industries

- Denali

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent government regulations mandating organic waste segregation and diversion from landfills

- 4.2.2 Growing environmental awareness and corporate sustainability commitments

- 4.2.3 Increasing adoption of circular economy principles and waste-to-energy initiatives

- 4.2.4 Rising urbanization driving higher volumes of municipal organic waste generation

- 4.2.5 Economic incentives and subsidies for organic waste management programs

- 4.2.6 Expansion of composting infrastructure and biogas production facilities

- 4.3 Market Restraints

- 4.3.1 High initial capital investment for collection infrastructure and processing facilities

- 4.3.2 Lack of public awareness and low participation rates in source segregation programs

- 4.3.3 Contamination of organic waste streams reducing processing efficiency

- 4.3.4 Limited availability of cost-effective collection and transportation solutions in rural areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 AI-powered route optimization ROI

- 4.6.2 IoT sensor-based bin monitoring

- 4.6.3 Blockchain for waste tracking & credits

- 4.6.4 Mobile app adoption & customer retention impact

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Artificial Intelligence-Powered Waste Collection on Service Providers' Revenue Growth

- 4.9 Consumer behavior shifts toward zero-waste lifestyles influencing service demand

5 Market Size & Growth Forecasts

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Bio-Sludge & Wastewater Organics

- 5.1.5 Commercial Organics (Non-Food)

- 5.1.6 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial Food Service

- 5.2.3 Food Processing & Manufacturing

- 5.2.4 Retail & Grocery

- 5.2.5 Others

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Centralized Drop-Off Collection

- 5.3.3 Bulk Collection

- 5.3.4 Underground Collection

- 5.3.5 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Republic Services

- 6.4.2 Veolia

- 6.4.3 Waste Management (WM)

- 6.4.4 Waste Connections

- 6.4.5 Cleanaway

- 6.4.6 Sanimax

- 6.4.7 Shapiro (Skip Shapiro Enterprises)

- 6.4.8 Biotic Waste Limited

- 6.4.9 Compost Crew

- 6.4.10 Circular Services

- 6.4.11 Emterra USA

- 6.4.12 Keenan Recycling (Biffa Company)

- 6.4.13 Grundon

- 6.4.14 GAP Organics

- 6.4.15 Monster Organics

- 6.4.16 Recology

- 6.4.17 Royal Waste Services

- 6.4.18 Total Organics Recycling

- 6.4.19 Groot Industries

- 6.4.20 Denali

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion