PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063910

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063910

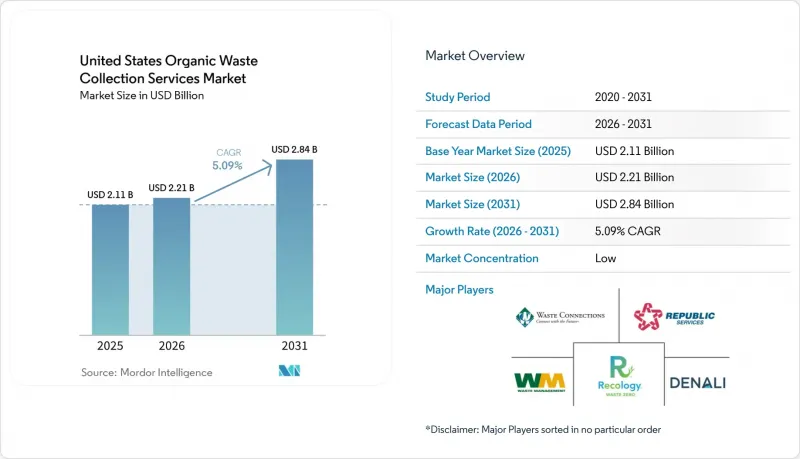

United States Organic Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states organic waste collection services market size is projected to expand from USD 2.11 billion in 2025 and USD 2.21 billion in 2026 to USD 2.84 billion by 2031, registering a CAGR of 5.09% between 2026 to 2031.

This report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), End-User (Residential, Commercial, and More), Collection Method (Door-To-Door Collection, Drop-Off / Bring Systems, and Others), and Technology & Equipment (Manual Collection, Semi-Automated, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

United States Organic Waste Collection Services Market Trends and Insights

Stringent Government Regulations and Mandatory Organic Waste Diversion Laws

California's SB 1383 mandated a 75% reduction in organic waste disposal by 2025 versus a 2014 baseline. It required 20% edible food recovery, compelling every jurisdiction to provide organic waste collection services to residents and businesses . Jurisdictions are implementing curbside organics, edible food recovery contracting, and the procurement of recovered organic products to maintain compliance and avoid penalties, thereby creating steady demand for collection and processing capacity across cities and counties. Washington's HB 2301 phases in organic waste diversion requirements for businesses through 2026 and sets firm timelines for residential curbside organics collection, standard bin colors, and product labeling controls to address contamination risks. Federal agencies are reinforcing this trajectory as the EPA, USDA, and FDA coordinate a national strategy to cut food loss and waste by 50% by 2030, which aligns with multistate action and gives municipalities a clear policy signal for program expansion in 2026. EPA's SWIFR program guidance and USDA cooperative agreements provide funding to reduce execution risk for new curbside rollouts and upgrades to back-end infrastructure.

Rising Landfill Tipping Fees and Disposal Costs

Tipping fees for municipal solid waste disposal rose 10% nationally in 2024 to USD 62.28 per ton, with the Northeast showing the highest fees and the South Central the lowest, which tightens the economic case for organics diversion across high-cost markets. Waste-to-energy states paid 28% more for landfill disposal than non-WTE states, indicating that constrained disposal capacity alters price signals and accelerates the adoption of alternatives, such as organics collection and processing. As municipalities update contracts, the widening cost gap between traditional disposal and organics programs supports budget-neutral or savings-oriented pitches for new curbside organics service, especially in dense metros with scarce landfill options. International examples reinforce the same thesis as policy and pricing shift behavior when residents face meaningful cost differentials between gray-bin disposal and organics recycling. In 2026, this price environment continues to steer large commercial generators and municipalities toward organics collection contracts that reduce landfill exposure and future liability for disposal escalators.

Limited Infrastructure Capacity for Organic Waste Processing and Treatment Facilities

EPA's national infrastructure assessment identifies a sizable funding requirement to expand composting and anaerobic digestion capacity, with USD 14-16 billion needed by 2030 to reach a projected national recycling rate of 61%. The funding envelope spans facility development, collection system expansion, and education, underscoring that collection growth depends on balanced investments across the chain rather than stand-alone projects. Capacity gaps are most acute in the South, Southwest, and Rocky Mountain regions, which underscores the need for targeted siting and permitting support where feedstock potential is high but facilities are sparse. In 2026, constrained throughput continues to limit new municipal rollouts and private contracts in several states, which slows diversion despite clear policy direction. Addressing this bottleneck requires blending public funding, procurement reforms, and private partnerships that bundle long-term feedstock commitments with data transparency to accelerate financing and delivery.

Other drivers and restraints analyzed in the detailed report include:

- Growing Environmental Awareness and Corporate ESG/Sustainability Commitments

- Technological Advancements in Collection Systems, Sorting Automation, and Processing

- High Capital and Operational Costs for Collection and Processing Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food waste, including pre-consumer and post-consumer streams, is projected to grow the fastest, with a 5.9% CAGR from 2026 to 2031, as compliance deadlines and business thresholds tighten across major states. The United States organic waste collection services market benefits from SB 1383 requirements that make year-round food scrap collection a universal service, which establishes program continuity and a predictable volume base for haulers and processors. Washington's HB 2301 establishes tiered diversion thresholds for businesses and requires residential curbside organics collection on a set timetable, thereby supporting improvements in route density and equipment utilization over time. Pre-consumer food waste from commercial kitchens, institutional cafeterias, and processors offers higher tonnage density and lower contamination risk, which aligns with specialized service models and predictable pickups for large generators. Partnerships linking collection with anaerobic digestion have expanded as industry groups and operators coordinate feedstock sourcing to enable efficient conversion to biogas and digestate. Yard and landscape waste continued to hold the largest share at 70.9% in 2025, driven by the long-standing maturity of municipal programs. However, incremental growth is limited by demographic shifts and the rise of multi-family housing, where yard generation is lower.

In 2026, residential post-consumer food waste collection gains coverage in major metros through policy mandates and voluntary rollouts, expanding household access and building familiarity with source separation over time. Agricultural Residues remain a smaller share, as many materials are managed on-site or move through specialized brokers into nutrient and energy pathways that are not always visible to municipal systems. Others, including biosolids and industrial organics, grow steadily as compliance frameworks and beneficial use standards drive consistent processing routes that reduce landfill exposure and produce marketable outputs. The United States organic waste collection services market will continue to shift toward higher food waste penetration as education, contamination controls, and equipment upgrades improve performance at scale. Food waste's contribution to the United States organic waste collection services market size is reinforced by transparent reporting expectations in corporate ESG programs that reward verifiable diversion at the facility level.

List of Companies Covered in this Report:

- Waste Management, Inc. (WM)

- Republic Services

- Waste Connections

- Denali

- Recology

- Synagro

- CompostNow

- Agri-Cycle Energy

- Compost Crew

- Black Earth Compost

- Bootstrap Compost

- Groot Industries

- Atlas Organics

- Vanguard Renewables

- Anaergia Technologies

- RNG Energy Solutions LLC

- PurposeEnergy

- Convertus Group

- Remix Organics

- AgRecycle

- Action Carting Environmental Services, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Government Regulations and Mandatory Organic Waste Diversion Laws

- 4.2.2 Rising Landfill Tipping Fees and Disposal Costs

- 4.2.3 Growing Environmental Awareness and Corporate ESG/Sustainability Commitments

- 4.2.4 Technological Advancements in Collection Systems, Sorting Automation, and Processing

- 4.2.5 Circular Economy Adoption and Waste-to-Wealth Paradigm Shift

- 4.2.6 Renewable Energy Incentives and Carbon Credit Monetization Opportunities

- 4.3 Market Restraints

- 4.3.1 Limited Infrastructure Capacity for Organic Waste Processing and Treatment Facilities

- 4.3.2 High Capital and Operational Costs for Collection and Processing Systems

- 4.3.3 Low Participation Rates in Residential and Commercial Collection Programs

- 4.3.4 Insufficient Community Outreach, Education, and Behavior Change Programs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 RFID Smart Bins for Waste Tracking

- 4.6.2 AI Revolutionizes Waste Sorting

- 4.6.3 IoT Optimizing for Fleet Routes

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Fleet Modernization & Electrification in Waste Collection

- 4.9 Analysis of Biomethane Impact on Organic Waste Collection

- 4.10 Collaboration Between Municipalities and Private Operators is Gaining Traction

- 4.11 Growing Focus on Methane Capture from Organic Waste to Meet Climate Targets

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Waste Type

- 5.1.1 Food Waste

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial Food Service

- 5.2.3 Industrial (Food Processing & Manufacturing)

- 5.2.4 Others (Agri-waste)

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Drop-Off / Bring Systems

- 5.3.3 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Waste Management, Inc. (WM)

- 6.4.2 Republic Services

- 6.4.3 Waste Connections

- 6.4.4 Denali

- 6.4.5 Recology

- 6.4.6 Synagro

- 6.4.7 CompostNow

- 6.4.8 Agri-Cycle Energy

- 6.4.9 Compost Crew

- 6.4.10 Black Earth Compost

- 6.4.11 Bootstrap Compost

- 6.4.12 Groot Industries

- 6.4.13 Atlas Organics

- 6.4.14 Vanguard Renewables

- 6.4.15 Anaergia Technologies

- 6.4.16 RNG Energy Solutions LLC

- 6.4.17 PurposeEnergy

- 6.4.18 Convertus Group

- 6.4.19 Remix Organics

- 6.4.20 AgRecycle

- 6.4.21 Action Carting Environmental Services, Inc.

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

- 7.3 Shift Toward Decentralized Organic Waste Processing