PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063906

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063906

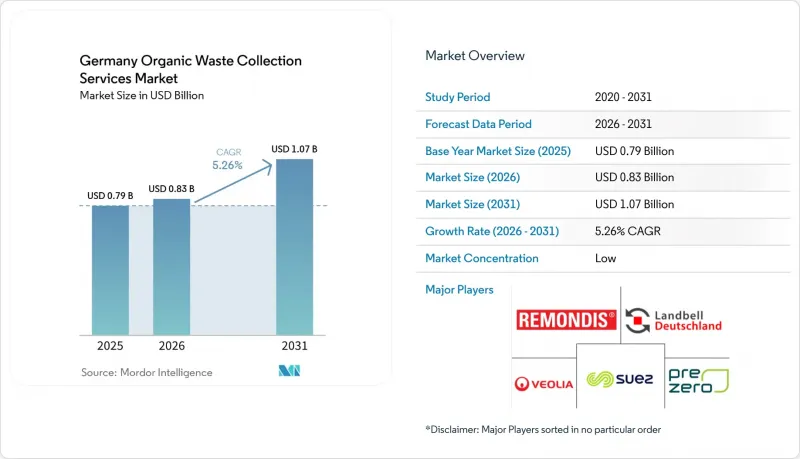

Germany Organic Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany organic waste collection services market size is projected to be USD 0.79 billion in 2025, USD 0.83 billion in 2026, and reach USD 1.07 billion by 2031, growing at a CAGR of 5.26% from 2026 to 2031.

This report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), by End-User (Residential, Commercial, and More), by Collection Method (Door-To-Door Collection, Drop-Off / Bring Systems, and Others), and by Technology & Equipment (Manual Collection Systems, Semi-Automated Systems, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Germany Organic Waste Collection Services Market Trends and Insights

Biowaste Ordinance (BioAbfV) Tightening Quality of Input Streams

The May 2025 amendment to Germany's Biowaste Ordinance established binding contamination thresholds and gave processors explicit authority to reject non-compliant loads, transferring quality risk upstream to collection operators. This forces operators to deploy optical sorting, depackaging, and bin-screening systems to preserve gate acceptance and avoid costly re-routing to residual streams. Pilot audits show that microplastic contamination in finished compost rises when collection purity slips. This jeopardizes soil-application approvals and triggers rework costs, directly harming collection route profitability through rejected loads and penalty fees. Municipal responses vary by district, with some authorities banning biodegradable plastic bags in brown bins and others implementing bin inspections and staged penalties before non-collection, creating uneven compliance costs across service footprints. Operators that invested early in depackaging systems gained a competitive advantage by meeting stricter processor acceptance standards and avoiding load rejections. The market is therefore moving toward quality assurance as a central performance lever where traceability, inspection, and technology integration decide margins more than tonnage growth. Enforcement heterogeneity will persist as some municipalities tighten inspections faster than others, sustaining regional cost differentials that shape near-term bidding strategies.

Circular Economy Act (KrWG) Driving Recycling Over Disposal

Germany's Circular Economy Act establishes a five-tier hierarchy that prioritizes prevention and recycling over energy recovery and landfill, and mandates separate collection of organic waste, which continues to push municipalities to expand brown-bin access and improve source separation. The National Circular Economy Strategy, adopted in 2024, reinforced this direction by targeting a 10% per-capita reduction in municipal waste by 2030. Recent balances show household organic waste rose to 10.7 million tonnes in 2024, up 5.9% from 2023, confirming organic separation as a fast-growing municipal fraction by weight. Emissions trading increases the cost of non-segregation for local authorities because residual-waste incineration can require certificates, adding cost to routes that lack effective diversion of organics. Packaging reform is indirectly supportive because higher recycling expectations increase the salience of correct sorting at home, which can reduce foreign-material inflows into organic bins when communication is effective. Annual municipal reporting also keeps pressure on laggards by publicizing separation rates, nudging investment into container fleets, and promoting public education and route density where returns are visible. The market benefits from this policy alignment over a multi-year horizon because long-lived container and fleet investments lock in capability and scale effects around separation and purity.

Contamination in Collected Organic Waste Streams

Plastic contamination remains the primary quality constraint for processors, and controls continue to exhibit notable rejection rates, underscoring the need for strict enforcement and improved sorting at source. The ordinance reduced acceptable plastic levels in household biowaste to 1%. It empowered plants to reject loads with more than 3% foreign material, shifting financial risk to operators who must either add pre-treatment or absorb re-routing costs. Jurisdictions have increased enforcement with inspections and penalties that escalate from warnings to non-collection, showing that visible deterrents can improve compliance. Other districts rely on non-collection for contaminated bins and charge residual-waste fees for subsequent disposal, shifting responsibility to households and businesses but potentially raising friction with ratepayers. Removing foreign material often results in a meaningful share of the organic fraction being lost as collateral, worsening value capture for processors and emphasizing curb-side prevention over plant-based remediation. As compostable packaging rules phase in over time, systems must still keep non-accepted materials out of organic bins to protect downstream quality certifications and agricultural acceptance.

Other drivers and restraints analyzed in the detailed report include:

- Municipalities Expand "Brown Bin" Infrastructure for Biowaste

- Biogas & Compost Integration into Germany's Renewable Energy Mix

- High Collection & Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Yard and landscape waste held 48.2% of the market share in 2025, while pre- and post-consumer food waste is projected to grow at a 7.41% CAGR through 2031, outpacing the overall expansion rate and signaling a gradual shift in the composition of collected waste. The market benefits from clearer rules and enforcement around packaged food waste that push more commercial volumes into depackaging lines before digestion, and operators that invest in such capabilities experience fewer rejections and more stable plant acceptance. Household organics have grown in recent balances, but yard-waste seasonality constrains further volume gains relative to food waste. Composters continue to blend green waste with biowaste to maintain stable processing characteristics, and quality controls increasingly police contamination to protect soil outlets that remain essential for market stability. As digester operators demand more consistent, high-energy-density substrates, commercial food waste becomes a more attractive target, provided depackaging performance holds contamination below mandated control values.

Across municipalities, policy still influences composition through brown-bin access, communications, and frequency schedules that support clean capture of both food and yard streams. Agricultural residues represent a smaller but growing segment, driven by commercial collection from urban agriculture projects, peri-urban farms participating in municipal organics programs, and institutional composting partnerships. Large-scale agricultural waste from rural operations typically remains outside municipal tender systems, is processed through on-farm digesters, and is then directly land-applied. The municipal-adjacent agricultural collection is forecast to expand as circular-economy frameworks incentivize the integration of diverse organic feedstocks into regional biogas and composting infrastructure. Food waste will likely continue to outpace yard waste because revenue models at biogas plants favor its methane yield, and expanding biomethane injection capacity pulls in consistent feedstock from commercial accounts that meet strict contamination rules. This shift can also help protect compost quality by steering the most contamination-prone, plastic-laden inputs into pre-treated digestion routes where depackaging is standard, limiting plastic carryover into composted material and maintaining downstream farm acceptance. The market, therefore, aligns its waste-type mix with energy and soil end-markets, using quality controls to allocate volumes where they generate the best value.

Residential end-users accounted for 73.1% of 2025 activity, supported by widespread brown-bin programs and generally high connection rates where participation is mandatory. The fastest growth is in the commercial food service segment, projected at a 7.92% CAGR through 2031, driven by tighter separation requirements, stronger compliance oversight, and sustainability targets that formalize previously ad hoc arrangements. The market is seeing more contracts from restaurants, hotels, supermarkets, and institutional kitchens as handling requirements for food waste and transport tracking shift from guidance to enforcement. Industrial food processors contribute steady volumes with relatively reliable composition that digester operators value, and longer-term acceptance arrangements can reduce revenue volatility for collectors who serve these sites. Agricultural and other small categories remain marginal in municipal systems, keeping the commercial food-service vector as the main swing factor, diversifying revenue beyond residential accounts.

Enforcement rigor remains the driver of commercial growth as municipalities pilot technology-enabled bin inspections and collection controls that can extend to business premises, prompting more customers to adopt contracted service under clear quality terms. This approach supports more reliable plant acceptance because commercial sources can adapt faster than dispersed households to separation rules that protect digester uptime and compost quality certifications. The market benefits from predictable volume and stronger contamination control when commercial accounts are onboarded under auditable protocols, improving route economics and stabilizing processor relationships. Residential volumes remain the anchor, but marginal growth shifts to commercial streams where policy and technology reduce non-compliance risk and improve collection efficiency. Over time, mixed municipal-commercial portfolios help operators smooth yard-waste seasonality and rely more on year-round food waste that supports steadier digester operations.

List of Companies Covered in this Report:

- REMONDIS SE & Co.

- PreZero Stiftung & Co. KG

- Veolia Environnement S.A.

- Landbell Group GmbH

- SUEZ Group

- ALBA Group

- Interzero Holding

- Nehlsen AG

- Bartscherer & Co. Recycling GmbH

- AVEA GmbH & Co. KG

- Ihlenberger Abfallentsorgungsgesellschaft mbH (IAG)

- Schneemann Recycling GmbH

- Berliner Stadtreinigungsbetriebe AoR

- SARIA SE & Co. KG

- Zentek GmbH & Co. KG

- Geocycle GmbH

- FCC Environment GmbH

- Urbaser S.A.U.

- Stena Recycling GmbH

- KS-Recycling GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biowaste Ordinance (BioAbfV) Tightening Quality of Input Streams

- 4.2.2 Circular Economy Act (KrWG) Driving Recycling Over Disposal

- 4.2.3 Municipalities Expand "Brown Bin" Infrastructure for Biowaste

- 4.2.4 Biogas & Compost Integration into Germany's Renewable Energy Mix

- 4.2.5 Strong Municipal Role in Waste Collection

- 4.2.6 High Household Participation in Waste Segregation

- 4.3 Market Restraints

- 4.3.1 Contamination in Collected Organic Waste Streams

- 4.3.2 High Collection & Logistics Costs

- 4.3.3 Limited Economic Viability in Rural Regions

- 4.3.4 Limited Standardization of Collection Practices Across Municipalities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Anaerobic Digestion Integrated with Germany's Biogas Infrastructure

- 4.6.2 In-vessel Composting for High-Quality Agricultural Compost

- 4.6.3 Optical Sorting & Contaminant Removal

- 4.6.4 Smart Bin Tagging & Pay-As-You-Throw (PAYT) Systems

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Fee-Based Waste Systems on the Market

- 4.9 Insights on Shift Toward Zero-Waste Municipal Systems

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial (HoReCa, Retail)

- 5.2.3 Industrial (Food Processing & Manufacturing)

- 5.2.4 Others (Agri-waste)

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Drop-Off / Bring Systems

- 5.3.3 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 REMONDIS SE & Co.

- 6.4.2 PreZero Stiftung & Co. KG

- 6.4.3 Veolia Environnement S.A.

- 6.4.4 Landbell Group GmbH

- 6.4.5 SUEZ Group

- 6.4.6 ALBA Group

- 6.4.7 Interzero Holding

- 6.4.8 Nehlsen AG

- 6.4.9 Bartscherer & Co. Recycling GmbH

- 6.4.10 AVEA GmbH & Co. KG

- 6.4.11 Ihlenberger Abfallentsorgungsgesellschaft mbH (IAG)

- 6.4.12 Schneemann Recycling GmbH

- 6.4.13 Berliner Stadtreinigungsbetriebe AoR

- 6.4.14 SARIA SE & Co. KG

- 6.4.15 Zentek GmbH & Co. KG

- 6.4.16 Geocycle GmbH

- 6.4.17 FCC Environment GmbH

- 6.4.18 Urbaser S.A.U.

- 6.4.19 Stena Recycling GmbH

- 6.4.20 KS-Recycling GmbH & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

- 7.3 Shift Toward Decentralized Organic Waste Processing