PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063909

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063909

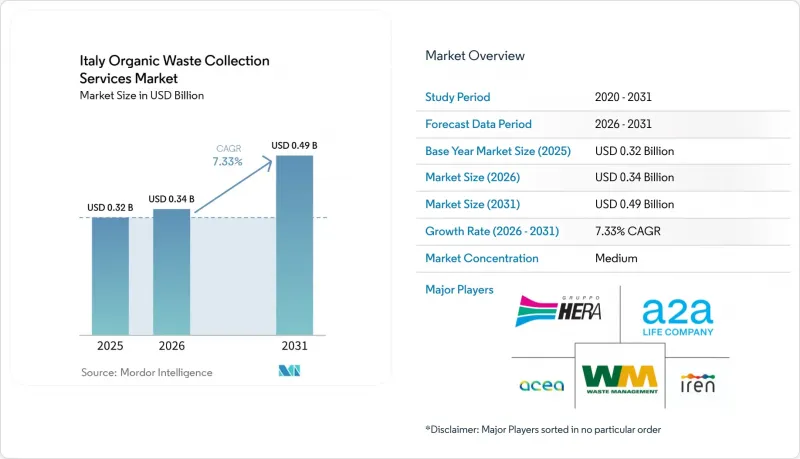

Italy Organic Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the italy organic waste collection services market size was valued at USD 0.32 billion in 2025 and is estimated to grow from USD 0.34 billion in 2026 to reach USD 0.49 billion by 2031, at a CAGR of 7.33% during the forecast period (2026-2031).

This report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), by End-User (Residential, Commercial, Industrial, and Others), by Collection Method (Door-To-Door, Drop-Off / Bring Systems, and Others), by Technology and Equipment (Manual, Semi-Automated, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Italy Organic Waste Collection Services Market Trends and Insights

High Municipal Compliance with Italy's "Raccolta Differenziata" Targets

Italy reached a 67.7% national separate collection rate in 2024, consolidating progress toward higher diversion of organic streams within differentiated collection systems. Regional leaders such as Emilia-Romagna and Veneto maintained performance levels above the national average, which enhances the quality and quantity of organic feedstock available for composting and anaerobic digestion. These outcomes are reinforced by long-term integrated service contracts that standardize door-to-door protocols and embed feedstock quality controls, which improve the operating environment for collection firms in high-compliance zones. In large cities where collection density and complexity are high, pairing infrastructure with user-facing tools and RFID helps reduce residual fractions while improving traceability of organic bins. Regions that combine higher-than-average separate collection with investment in digestion assets tend to host more biomethane plants, which tightens the link between upstream service design and downstream energy valorization. The cumulative effect is a more resilient base of captured organic material for operators in the Italy organic waste collection services market, which supports scale economics and revenue diversity across collection and treatment.

Expansion of Composting Infrastructure in Northern Italy

Northern regions operate more biological treatment sites than Southern territories, resulting in lower per-capita collection and transfer costs. In contrast, Central Italy records the country's highest per-capita management costs due to infrastructure gaps and longer transport distances, while Southern regions face similar cost pressures alongside lower treatment capacity. The current build-out trajectory reflects a continued shift from standalone composting toward integrated anaerobic digestion with aerobic stabilization, which increases energy revenues while preserving compost outputs from the same feedstock. A recent capacity expansion in Liguria illustrates the direction of travel, with a biodigester doubling its throughput, injecting biomethane into the national grid, and producing certified compost for agriculture. Strategic siting near agro-industrial clusters supports co-digestion of residues, boosting biogas yields and stabilizing plant economics year-round. As the North continues to lead on infrastructure density, service operators can plan collection routes around nearer facilities, which lowers unit costs and mitigates transport risks, a dynamic that remains a priority for municipalities in the Italy organic waste collection services market. Over the medium term, new digestion and composting projects in underserved provinces are positioned to rebalance regional flows of organics and reduce long-haul transfers.

High Contamination Levels in Collected Organic Waste Streams

Despite Italy's 67.7% separate collection rate, variations in purity remain a challenge. Industry monitoring indicates persistent contamination of the organic fraction with plastic films, glass fragments, and metals, particularly in large metropolitan areas where resident compliance varies. These impurities add pre-processing stages such as sieving, magnetic separation, and optical sorting, which raise energy inputs per tonne and reduce net compost yields for operators. AI-enabled monitoring is emerging as a practical response at sorting plants and along collection routes, where computer vision flags contamination types and patterns that can be acted on operationally and through targeted resident communications. Deployments at large facilities demonstrate how real-time compositional analysis improves fiber quality for paper grades, illustrating the step-change AI and sensors can deliver across multiple material streams, including organics. Point-of-disposal cameras and route-level analytics from industry suppliers are also demonstrating higher purity in corporate settings, which signals broader applicability as municipalities aim to scale variable tariffs and contamination fee adjustments. Over time, capital availability will determine the pace of adoption of contamination-control technologies in smaller municipalities, thereby influencing cost recovery and pricing in the Italian organic waste collection service market.

Other drivers and restraints analyzed in the detailed report include:

- Landfill Diversion Targets Driving Organic Waste Segregation

- Pay-As-You-Throw (PAYT) Adoption by Italian Municipalities

- Rising Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food waste accounted for 76.1% of collection service revenues in 2025, driven by mandated separation of household and commercial organics and strong capture rates in municipalities with door-to-door programs. Regulatory obligations under D.Lgs. 116/2020 continue to anchor the primacy of the organic fraction of municipal solid waste, with certified compostable bags and resident education sustaining participation in curbside programs. As the largest segment, food waste is also projected to grow fastest among major waste types, with an 8.21% CAGR through 2031, reflecting ongoing expansion of separate collection mandates and biomethane incentives that increase captured volumes. Treatment pathways increasingly favor integrated anaerobic digestion followed by downstream composting to maximize energy output while meeting agronomic criteria for soil products, an approach now widespread across leading regions. Plants such as the expanded biodigester at Cairo Montenotte demonstrate how municipal organic fraction of municipal solid waste and green waste are converted into biomethane and compost, creating dual revenue streams and more resilient processing economics that support collection contract stability. Food service establishments generate dense organic loads that benefit from daily collection during peak seasons, and tariff structures recognize their higher waste intensity by aligning costs with waste-generation profiles. The Italy organic waste collection services market is therefore anchored in the organic fraction of municipal solid waste, where routing, bin design, and contamination control have the largest impact on feedstock quality and contract performance.

Green pruning and landscape waste represent the second-largest stream, characterized by seasonal fluctuations that challenge logistics and service levels in parks and residential neighborhoods. Composting-only facilities remain important for high-lignin fractions, with co-digestion reserved for blends that achieve more favorable carbon-nitrogen balances in anaerobic digestion tanks. Policies encourage the co-digestion of agro-industrial by-products to diversify feedstock sources and stabilize energy output profiles throughout the year. National bioeconomy planning designates support for anaerobic digestion in Southern regions, which may accelerate integration of farm-level residues into municipal collection frameworks where contracts and logistics permit. Collection service revenues for agricultural residues are projected to expand as new digestion sites secure guaranteed feed-in channels and strengthen local cooperatives' participation in organics management. Niche streams such as market waste can command premium gate fees when sorted to high purity, creating selective opportunities for municipalities that enforce robust contamination and set-out standards.

Residential users accounted for the largest share of 68.9% in 2025, reflecting the wide reach of separate collection programs and door-to-door service in many municipalities within the Italy organic waste collection services market. Pay-as-you-throw pilots confirm that households respond to clear variable charges by shifting residual fractions into organics and recyclables, improving capture rates in a matter of weeks when the program is paired with RFID-tagged bins and communications. Multi-family buildings often require tailored solutions, including controlled-access communal containers with user authentication that manage throughput and reduce contamination risks. Domestic composting adds a complementary channel that diverts a portion of household organics from collection programs to local soil benefit, with industry monitoring estimating meaningful tonnage savings at the municipal level. In high-performing provinces, the growth pace moderates as programs approach saturation, which shifts focus to contamination control and route efficiency. Overall, residential organics remain the bedrock of captured volumes that underpin treatment bookings and biomethane production plans across the Italy organic waste collection services market.

Commercial food service is set to grow faster than the residential base, registering a CAGR of 7.86% over the forecast period, as tariff coefficients align costs with waste intensity and as municipalities expand dedicated circuits for restaurants and catering. Programs that meter customer set-ups with RFID and IoT achieve greater accountability, enabling variable tariffs to be translated directly into operating adjustments at the site level. EU-funded demonstrations show that introducing pay-as-you-throw for commercial users can increase separate collection rates and reduce residual waste, validating the business case for segment-specific contracts. Industrial generators in agro-food processing are increasingly integrated into co-digestion frameworks, where plants partner with producers to secure steady streams of organic residues. For operators, these end-user niches expand the Italian organic waste collection service industry footprint into more complex accounts that require tighter scheduling and quality control against contamination. Stronger data systems and clearer contractual clarity on contamination fees are key to protecting margins as programs scale.

List of Companies Covered in this Report:

- Gruppo Hera

- A2A Group

- Gruppo Iren

- Waste Management, Inc.

- Acea Group

- Vivilab

- Veolia Environnement

- REMONDIS SE & Co.

- PreZero Stiftung & Co. KG

- Sogliano Ambiente

- Porcarelli Group

- Contarina S.p.A.

- Gruppo Veritas

- RAP Palermo

- Blue Wings Composting

- Biorepack Consortium

- FCC Environment

- Urbaser

- Indaver

- Valli Gestioni Ambientali

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Municipal Compliance with Italy's "Raccolta Differenziata" Targets

- 4.2.2 Expansion of Composting Infrastructure in Northern Italy

- 4.2.3 Landfill Diversion Targets Driving Organic Waste Segregation

- 4.2.4 Pay-As-You-Throw (PAYT) Adoption by Italian Municipalities

- 4.2.5 EU Circular Economy Targets Accelerating Organic Waste Valorization

- 4.2.6 Biomethane Incentives Boosting Organic Waste Collection

- 4.3 Market Restraints

- 4.3.1 High Contamination Levels in Collected Organic Waste Streams

- 4.3.2 Rising Operational Costs

- 4.3.3 Limited Processing Capacity in Southern Regions

- 4.3.4 Limited Standardization of Collection Practices Across Municipalities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 RFID Smart Bins for Waste Tracking

- 4.6.2 AI Revolutionizes Waste Sorting

- 4.6.3 IoT Optimizing for Fleet Routes

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Fleet Modernization & Electrification in Waste Collection

- 4.9 Analysis of Biomethane Impact on Organic Waste Collection

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Waste Type

- 5.1.1 Food Waste (Pre and Post Consumer)

- 5.1.2 Yard & Landscape Waste

- 5.1.3 Agricultural Residues

- 5.1.4 Others

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial (HoReCa, Retail)

- 5.2.3 Industrial (Food Processing & Manufacturing)

- 5.2.4 Others (Agri-waste)

- 5.3 By Collection Method

- 5.3.1 Door-to-Door Collection

- 5.3.2 Drop-Off / Bring Systems

- 5.3.3 Others

- 5.4 By Technology & Equipment

- 5.4.1 Manual Collection Systems

- 5.4.2 Semi-Automated Systems

- 5.4.3 Fully Automated Systems

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Gruppo Hera

- 6.4.2 A2A Group

- 6.4.3 Gruppo Iren

- 6.4.4 Waste Management, Inc.

- 6.4.5 Acea Group

- 6.4.6 Vivilab

- 6.4.7 Veolia Environnement

- 6.4.8 REMONDIS SE & Co.

- 6.4.9 PreZero Stiftung & Co. KG

- 6.4.10 Sogliano Ambiente

- 6.4.11 Porcarelli Group

- 6.4.12 Contarina S.p.A.

- 6.4.13 Gruppo Veritas

- 6.4.14 RAP Palermo

- 6.4.15 Blue Wings Composting

- 6.4.16 Biorepack Consortium

- 6.4.17 FCC Environment

- 6.4.18 Urbaser

- 6.4.19 Indaver

- 6.4.20 Valli Gestioni Ambientali

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion