PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939154

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939154

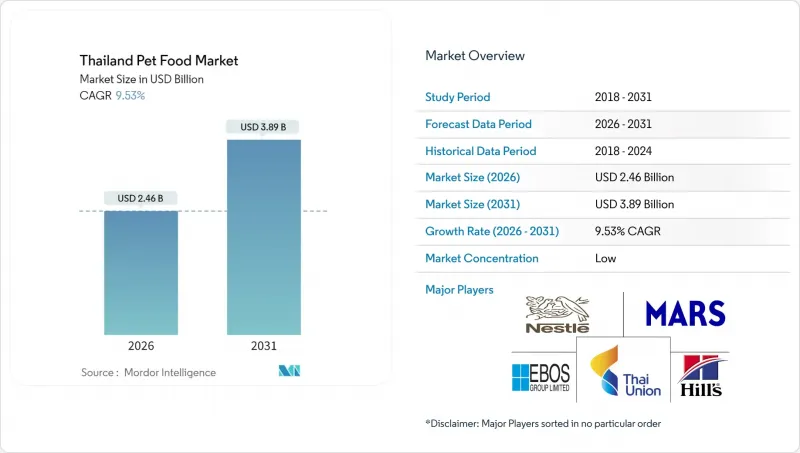

Thailand Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Thailand pet food market size in 2026 is estimated at USD 2.46 billion, growing from 2025 value of USD 2.25 billion with 2031 projections showing USD 3.89 billion, growing at 9.53% CAGR over 2026-2031.

This growth is based on Thailand's dual identity as a large domestic consumer market and the world's second-largest pet food exporter. Robust export earnings highlight sustained overseas demand, while rising urban pet ownership and premiumization nurture local consumption. Large players exploit economies of scale derived from Thailand's manufacturing hub status, yet smaller firms seize niche opportunities in therapeutic diets and novel proteins. Regulatory shifts, such as updated labeling rules, add compliance costs but also raise the quality bar, supporting long-term market confidence.

Thailand Pet Food Market Trends and Insights

Premiumization of Dog and Cat Food Formulations

Premium pet food formulations incorporating human-grade ingredients and functional additives are reshaping Thailand's domestic market as pet owners increasingly view their animals as family members. Premium recipes featuring human-grade meats, probiotics, and condition-specific nutrients now command price premiums of 15-20%. Mars Petcare co-develops Thai-tailored formulas with veterinary researchers, supporting breed-specific and life-stage diets. Thai Union's Strategy 2030 designates premium pet food as a pillar for tripling pet care revenue to 20% of the company's total corporate sales. Local firms respond with region-sourced proteins, intensifying R&D investment. Consumers value transparent sourcing and functional benefits, sustaining steady trade-up momentum.

Booming Online Grocery and Quick-Commerce Platforms

E-commerce penetration in Thailand's pet food sector is driven by platforms like Lazada and Shopee, as well as emerging quick-commerce services that offer same-day delivery in major urban areas. The online channel's 11.4% CAGR significantly outpaces traditional retail, reflecting the changing consumer behaviors accelerated by digital natives entering the pet ownership market. Live commerce and influencer marketing have become crucial tools for customer acquisition, with pet influencers commanding substantial followings and influencing purchase decisions through product demonstrations and testimonials. Mars unveiled Thailand's first innovative online pet adoption portal.

Volatile Raw-Material Prices

Raw material price volatility significantly impacts Thailand's pet food manufacturers, particularly for imported ingredients such as soybeans, corn, and specialized protein meals, which comprise 60-70% of production costs. The Thai government's 2024 adjustment of soybean meal import policies, which maintains 2% in-quota tariffs but sets high out-of-quota rates, reflects ongoing efforts to balance domestic agricultural protection with feed industry cost management. Currency depreciation increases input costs but supports export earnings, thereby intensifying margin management complexity, particularly for smaller brands with limited hedging capacity.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Modern Trade and Pet Specialty Chains

- Government Incentives for Domestic Meat and Seafood Co-Products

- Limited Cold-Chain Infrastructure for Fresh/Frozen Pet Food

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Thailand pet food market size for food products dominated the total value with 72.10% share in 2025, reflecting sustained consumer reliance on dry and wet staples. Within this group, veterinary diets are set to post an 11.55% CAGR, underpinned by rising pet insurance coverage and clinician trust. Thailand pet food market share for veterinary diets remains modest but expands rapidly as chronic conditions gain visibility in urban clinics. Manufacturers differentiate through clinical trials, probiotic inclusions, and novel marine proteins. Wet diets face shelf-life hurdles outside core urban areas, yet in Bangkok, these formulations flourish due to high palatability and moisture benefits.

Treats, supplements, and nutraceuticals attract health-conscious owners seeking preventive care. Human-grade dental and jerky snacks carry premium price points and align with bonding occasions. Government incentives for domestic co-products lower animal protein costs, widening gross margins. Companies invest in freeze-dry technology to extend shelf life without artificial preservatives. Continuous R&D on functional ingredients, such as joint-support peptides, bolsters product differentiation and sustains the Thailand pet food market.

The Thailand Pet Food Market Report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, and More), Pets (Cats, Dogs, and Other Pets), and Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Alltech Inc.

- Dechra Pharmaceuticals PLC

- Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- DoggyMan H. A. Co., Ltd.

- General Mills Inc.

- Thai Union Group PCL

- Mars, Incorporated

- Nestle S.A.(Purina)

- Virbac

- EBOS Group Limited

- Spectrum Brands Holdings Inc.

- Pets at Home Group plc

- ADM

- Diamond Pet Foods (Schell and Kampeter, Inc.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Consumer Trends

5 SUPPLY AND PRODUCTION DYNAMICS

- 5.1 Trade Analysis

- 5.2 Ingredient Trends

- 5.3 Value Chain and Distribution Channel Analysis

- 5.4 Regulatory Framework

- 5.5 Market Drivers

- 5.5.1 Premiumization of dog and cat food formulations

- 5.5.2 Booming online grocery and quick-commerce platforms

- 5.5.3 Expansion of modern trade and pet specialty chains

- 5.5.4 Government incentives for domestic meat and seafood co-products

- 5.5.5 Human-grade functional ingredients in treats

- 5.5.6 Rise in pet insurance driving demand for therapeutic diets

- 5.6 Market Restraints

- 5.6.1 Volatile raw-material prices

- 5.6.2 Limited cold-chain for fresh/frozen pet food

- 5.6.3 Low consumer awareness outside Bangkok

- 5.6.4 Fragmented regulatory oversight on supplements

6 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 6.1 Pet Food Product

- 6.1.1 Food

- 6.1.1.1 By Sub Product

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.1.1.1 Kibbles

- 6.1.1.1.1.1.2 Other Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.2 Wet Pet Food

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1 By Sub Product

- 6.1.2 Pet Nutraceuticals/Supplements

- 6.1.2.1 By Sub Product

- 6.1.2.1.1 Milk Bioactives

- 6.1.2.1.2 Omega-3 Fatty Acids

- 6.1.2.1.3 Probiotics

- 6.1.2.1.4 Proteins and Peptides

- 6.1.2.1.5 Vitamins and Minerals

- 6.1.2.1.6 Other Nutraceuticals

- 6.1.2.1 By Sub Product

- 6.1.3 Pet Treats

- 6.1.3.1 By Sub Product

- 6.1.3.1.1 Crunchy Treats

- 6.1.3.1.2 Dental Treats

- 6.1.3.1.3 Freeze-dried and Jerky Treats

- 6.1.3.1.4 Soft and Chewy Treats

- 6.1.3.1.5 Other Treats

- 6.1.3.1 By Sub Product

- 6.1.4 Pet Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.4.1.1 Derma Diets

- 6.1.4.1.2 Diabetes

- 6.1.4.1.3 Digestive Sensitivity

- 6.1.4.1.4 Obesity Diets

- 6.1.4.1.5 Oral Care Diets

- 6.1.4.1.6 Renal

- 6.1.4.1.7 Urinary tract disease

- 6.1.4.1.8 Other Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.1 Food

- 6.2 Pets

- 6.2.1 Cats

- 6.2.2 Dogs

- 6.2.3 Other Pets

- 6.3 Distribution Channel

- 6.3.1 Convenience Stores

- 6.3.2 Online Channel

- 6.3.3 Specialty Stores

- 6.3.4 Supermarkets/Hypermarkets

- 6.3.5 Other Channels

7 COMPETITIVE LANDSCAPE

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Brand Positioning Matrix

- 7.4 Market Claim Analysis

- 7.5 Company Landscape

- 7.6 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.6.1 Alltech Inc.

- 7.6.2 Dechra Pharmaceuticals PLC

- 7.6.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 7.6.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 7.6.5 DoggyMan H. A. Co., Ltd.

- 7.6.6 General Mills Inc.

- 7.6.7 Thai Union Group PCL

- 7.6.8 Mars, Incorporated

- 7.6.9 Nestle S.A.(Purina)

- 7.6.10 Virbac

- 7.6.11 EBOS Group Limited

- 7.6.12 Spectrum Brands Holdings Inc.

- 7.6.13 Pets at Home Group plc

- 7.6.14 ADM

- 7.6.15 Diamond Pet Foods (Schell and Kampeter, Inc.)

8 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS