PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940677

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940677

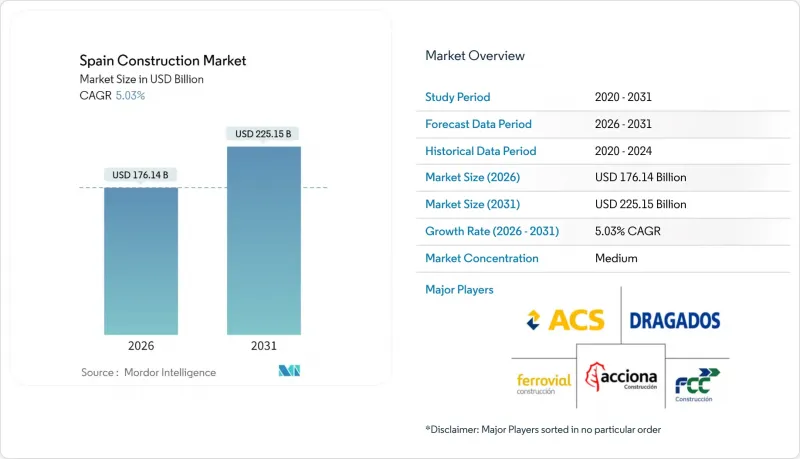

Spain Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Spain construction market is expected to grow from USD 167.70 billion in 2025 to USD 176.14 billion in 2026 and is forecast to reach USD 225.15 billion by 2031 at 5.03% CAGR over 2026-2031.

This expansion is propelled by Spain's access to USD 154 billion in NextGenerationEU resources, of which roughly 70% flows directly into construction-related programs spanning infrastructure, renewable energy, and building rehabilitation. Residential activity keeps demand resilient, while unprecedented public-sector spending anchors infrastructure outlays and crowds in private capital. Growing adoption of modern construction methods, extensive digitalization mandates, and the 2030 FIFA World Cup infrastructure program further widen the opportunity set. Nevertheless, labor scarcity and commodity-price volatility continue to weigh on margins, compelling firms to accelerate automation, off-site manufacturing, and strategic procurement actions.

Spain Construction Market Trends and Insights

EU-Funded Infrastructure Modernization

Spain secured USD 76.5 billion in grants, receiving an "excellent" rating from the European Commission for its recovery plan. Flagship rail schemes include the USD 919.6 million ADIF network renewal and the USD 3.3 billion Mediterranean Corridor upgrade, which converts single to double track and electrifies critical links. Complementary Connecting Europe Facility funding of USD 265.1 million supports 22 multimodal projects across eight regions. These works generate local employment, stimulate steel and concrete demand, and re-position Spain as a continental logistics hub.

Renewable-Energy Build-Out

National targets call for 62 GW of fresh renewable capacity by 2030, fuelling wide-ranging construction. The USD 770 million Teruel onshore wind contract for 125 GE Vernova turbines will deliver 760 MW and exemplifies portfolio scale-up. Iberdrola's USD 550 million smart-grid expansion, part-financed by EU funds, is projected to support 10,000 annual jobs. Energy-storage investments such as the Valdecanas pumped-storage upgrade (USD 118.8 million) raise grid resilience and secure stable EPC pipelines.

High Labor Cost & Skilled-Worker Shortages

Only 9.2% of Spain's construction workforce is under 29, down from 25.2% in 2008, constraining execution capacity for EU-funded projects. Vocational-training enrolment declined 45.6% over 15 years, widening gaps just as renewables and digitalization require specialized talent. The sector lobby pushes for expanded dual-training programs under the Fundacion Laboral de la Construccion, while recruiting abroad delivers incremental relief. Tight labor markets in Madrid and Catalonia drive wage escalation that jeopardizes bid competitiveness and strains fixed-price contracts.

Other drivers and restraints analyzed in the detailed report include:

- Housing-Demand Recovery Via Favorable Mortgage Rates

- Tourism-Led Commercial Real-Estate Rebound

- Volatile Cement & Steel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential construction held 36.80% of the Spain construction market share in 2025, sustained by unmet urban housing demand and a brisk foreign-buyer segment. Infrastructure, the fastest-growing component, is forecast to post a 6.78% CAGR through 2031 as Recovery-Plan disbursements front-load transport and energy upgrades. Metro Madrid line extensions, Mediterranean Corridor rail doubling, and Iberdrola grid expansions collectively shift contractor backlogs toward heavy civil works. Meanwhile, the 2030 FIFA World Cup injects marquee stadium and urban-mobility projects that further tilt growth toward infrastructure.

Despite the infrastructure's surge, residential pipelines remain robust in Madrid, Barcelona, and Valencia, where land scarcity and policy incentives favor vertical development. Energy-efficient building codes catalyze demand for heat-pump installations and high-performance envelopes, spurring specialized subcontractors. Commercial real estate capitalizes on revived tourism flows, while industrial space rides the wave of near-shoring and e-commerce logistics, showcasing the sector's diversified growth engines.

New construction dominated with a 67.05% slice of the Spain construction market size in 2025, powered by green-field rail, highway, and utility megaprojects. Renovation, however, is expanding at a 5.55% CAGR on the back of USD 3.8 billion in EU subsidies targeting 510,000 residential retrofit actions by 2026. Grants covering up to 80% of eligible costs and mandating 30% energy-use cuts amplify homeowner uptake. Catalonia leads with more than 300 subsidized schemes, while 597 public buildings across 499 municipalities secure separate retrofit funding.

The renovation surge addresses Spain's aging stock, with two-thirds of buildings older than 40 years. BIM-based energy audits and digital building permits streamline approval and encourage bundling of works, reducing unit costs. Contractors pivot to facade insulation, solar-ready roofing, and accessibility upgrades, creating niche opportunities for SME specialists. As utility bills climb, payback periods shrink, supporting a sustained retrofit wave beyond the grant window.

The Spain Construction Market Report is Segmented by Sector (Residential, Commercial, and Infrastructure), by Construction Type (New Construction and Renovation), by Construction Method (Conventional On-Site, and More), by Investment Source (Public and Private), and by Geography (Andalusia, Catalonia, Madrid, Valencia, and Rest of Spain). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ACS, Actividades de Construccion y Servicios, S.A.

- Dragados S.A.

- Acciona Construccion S.A.

- Ferrovial Construccion S.A.

- FCC Construccion S.A.

- Sacyr Construccion S.A.

- Elecnor S.A.

- Cobra Instalaciones y Servicios S.A.

- TSK Electronica y Electricidad S.A.

- Administrador de Infraestructuras Ferroviarias (ADIF)

- ADIF Alta Velocidad

- Obrascon Huarte Lain (OHLA) S.A.

- Grupo SANJOSE S.A.

- Aldesa Construcciones S.A.

- Vias y Construcciones S.A.

- COMSA Corporacion

- Copasa

- Grupo Ortiz

- Sorigue

- Rover Grupo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview (Macro-economy & Construction Activity)

- 4.2 Market Drivers

- 4.2.1 Recovery of housing demand supported by favourable mortgage rates

- 4.2.2 EU-funded infrastructure modernisation (NextGenerationEU)

- 4.2.3 Renewable-energy build-out (wind/solar & grid)

- 4.2.4 Tourism-led commercial real-estate rebound

- 4.2.5 Modular/industrialised construction adoption in public tenders

- 4.2.6 Water-scarcity adaptation projects (desalination, reuse)

- 4.3 Market Restraints

- 4.3.1 High labour cost & skilled-worker shortages

- 4.3.2 Volatile cement & steel prices

- 4.3.3 Stringent biodiversity impact assessments

- 4.3.4 Rising climate-risk insurance premiums

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.4.3 Architectural and Engineering Companies - Key Quantitative and Qualitative Insights

- 4.4.4 Building Material and Equipment Companies - Key Quantitative and Qualitative Insights

- 4.5 Government Initiatives & Vision

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Force Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing (Construction Materials) and Construction Cost (Materials, Labour, Equipment) Analysis

- 4.10 Comparison of Key Industry Metrics of the Spain with Other Countries

- 4.11 Key Upcoming/Ongoing Projects (with a focus on Mega Projects)

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.1.1 Apartments/Condominiums

- 5.1.1.2 Villas/Landed Houses

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Industrial and Logistics

- 5.1.2.4 Others

- 5.1.3 Infrastructure

- 5.1.3.1 Transportation Infrastructure (Roadways, Railways, Airways, others)

- 5.1.3.2 Energy & Utilities

- 5.1.3.3 Others

- 5.1.1 Residential

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By Construction Method

- 5.3.1 Conventional On-Site

- 5.3.2 Modern Methods of Construction (Prefabricated, Modular, etc)

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Geography

- 5.5.1 Andalusia

- 5.5.2 Catalonia

- 5.5.3 Madrid

- 5.5.4 Valencia

- 5.5.5 Rest of Spain

6 Competitive Landscape

- 6.1 Market Concentration & Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.3.1 ACS, Actividades de Construccion y Servicios, S.A.

- 6.3.2 Dragados S.A.

- 6.3.3 Acciona Construccion S.A.

- 6.3.4 Ferrovial Construccion S.A.

- 6.3.5 FCC Construccion S.A.

- 6.3.6 Sacyr Construccion S.A.

- 6.3.7 Elecnor S.A.

- 6.3.8 Cobra Instalaciones y Servicios S.A.

- 6.3.9 TSK Electronica y Electricidad S.A.

- 6.3.10 Administrador de Infraestructuras Ferroviarias (ADIF)

- 6.3.11 ADIF Alta Velocidad

- 6.3.12 Obrascon Huarte Lain (OHLA) S.A.

- 6.3.13 Grupo SANJOSE S.A.

- 6.3.14 Aldesa Construcciones S.A.

- 6.3.15 Vias y Construcciones S.A.

- 6.3.16 COMSA Corporacion

- 6.3.17 Copasa

- 6.3.18 Grupo Ortiz

- 6.3.19 Sorigue

- 6.3.20 Rover Grupo

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment