PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063429

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063429

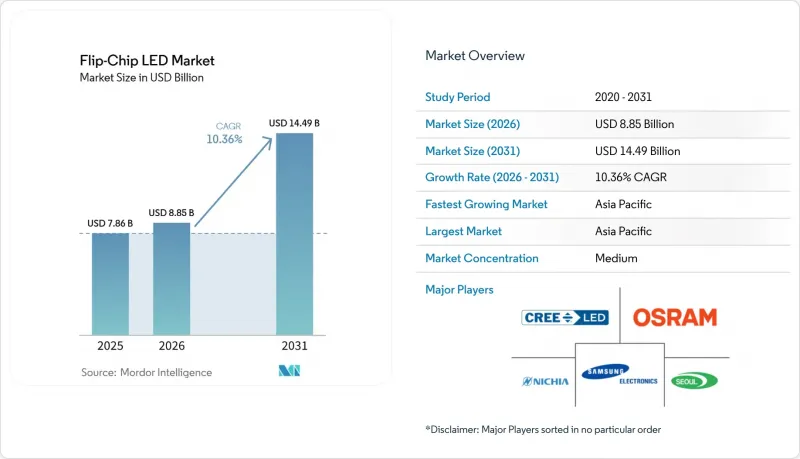

Flip-Chip LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the flip-Chip lED market size is expected to increase from USD 7.86 billion in 2025 to USD 8.85 billion in 2026 and reach USD 14.49 billion by 2031, growing at a CAGR of 10.36% over 2026-2031.

This report is Segmented by Material System (GaN, Algainp, and Other Material Systems), Wavelength/Color (Blue, White, Red, Green, and Other Wavelengths/Colors), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Displays and Signage, Backlighting, and Other Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Flip-Chip LED Market Trends and Insights

Accelerated Mini-LED Adoption in Large-Format Displays

Demand for premium televisions and monitors has shifted to direct-lit mini-LED backlighting with more than 10,000 local dimming zones, driving a sharp rise in high-density flip-chip die shipments. Eliminating wire bonds lets manufacturers position emitters closer together, which is critical when thousands of dice populate a single module. Better thermal paths permit each pixel to operate at higher current without early lumen depreciation, enabling HDR peak luminance above 2,000 nits. Flip-chip mini-LEDs also reduce module thickness by 15-20%, resulting in slimmer bezels and lower shipping costs. These advantages reinforce the Flip-Chip LED market leadership position in premium display backlights.

Rapid Penetration in Automotive Adaptive Lighting Modules

Adaptive driving beam systems require pixelated arrays that modulate individual emitters in milliseconds, and flip-chip bonding maintains current density and heat flux within compact headlamp enclosures. Automotive-qualified packages, such as the LUXEON Altilon SMD-A, achieve luminous intensity above 1,200 lumens while meeting stringent AEC-Q102 reliability targets. European ECE Regulation 123 mandates glare-free high beams on new vehicle types from 2026, accelerating procurement of flip-chip LED arrays that deliver precise beam shaping. Volume contracts awarded to Seoul Semiconductor and others confirm that adaptive lighting demand boosts the Flip-Chip LED market well into the forecast horizon.

Capital-Intensive Flip-Chip Packaging Lines

Equipment sets for high-volume flip-chip assembly require die bonders, underfill dispensers, and reflow ovens that collectively cost USD 15-25 million, a hurdle that delays capacity expansion in emerging markets. Tool lead times stretched to 12-18 months during 2025, and backlogs at Besi and ASM Pacific Technology exceeded six quarters, constraining second-tier packagers. Process windows are narrower than for wire bonds, demanding cleanroom upgrades and inline metrology that raise operational expense by 30-40%. These capital barriers slow new-entrant participation, tempering Flip-Chip LED market growth in cost-sensitive geographies.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates Across Asia-Pacific and Europe

- Lower Total-Cost-of-Ownership Versus Wire-Bond LEDs

- Competitive Pressure from Vertical Thin-Film LEDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gallium nitride controlled 52.19% of 2025 revenue, underscoring its status as the workhorse substrate for blue and white emitters that dominate general illumination. The wide bandgap, high thermal conductivity, and mature epitaxial recipes of GaN underpin efficient emission across visible wavelengths, reinforcing its primacy in the Flip-Chip LED market. Scaling to 300 millimeter GaN-on-silicon wafers may cut die cost per lumen in the coming years, further solidifying the material's value proposition.

Other material systems, chiefly ultraviolet, infrared, and short-wave infrared, are forecast to grow at a 10.85% CAGR. Water purification modules using ultraviolet-C flip-chip emitters and non-invasive biosensing devices employing indium phosphide infrared dice illustrate how specialty materials outpace the broader Flip-Chip LED market. Defense and aerospace requirements for shock-resistant packages further expand demand for niche wavelengths that flip-chip bonding supports through superior mechanical robustness.

Blue Dice supplied 41.52% of revenue in 2025, leveraging decades of process refinement to achieve commercial efficacy beyond 150 lumens per watt at a 85 °C junction temperature. These devices underpin phosphor-converted white light and serve as the baseline backlight for LCDs, guaranteeing continued bulk volume for the Flip-Chip LED market. Red phosphide retains importance in signaling and horticulture but expands more slowly due to temperature-sensitive efficiency.

Green emitters are set to grow at a 10.91% CAGR following a 2025 laboratory breakthrough that delivered 65% external quantum efficiency using aluminum-treated quantum wells. Closing the historic green gap elevates micro-LED display performance, as green sub-pixels dominate perceived luminance. This technical leap positions green flip-chip LEDs for rapid share gains, reinforcing overall Flip-Chip LED market momentum toward high-resolution direct-view panels.

Geography Analysis

Asia-Pacific controlled 42.72% of 2025 revenue and is projected to grow at an 11.14% CAGR through 2031, powered by capacity expansions in China, Taiwan, and South Korea. San'an Optoelectronics operates the world's largest MOCVD fleet and broadened flip-chip output after acquiring Lumileds, an integration that secures automotive customer pipelines. Taiwan's Epistar and Lextar pivoted toward mini-LED and micro-LED, capitalizing on the same high-density attributes that differentiate the Flip-Chip LED market. Japan's Nichia and South Korea's Samsung continue to lead breakthroughs in efficacy that quickly migrate into mass production.

Europe and North America jointly contributed a significant share of 2025 revenue. The European Union's Stage 4 Ecodesign rules accelerated retrofits, while ECE Regulation 123 guarantees future demand for adaptive headlights that rely heavily on flip-chip arrays. North American manufacturing rationalized in 2025 when Cree Lighting outsourced assembly while retaining engineering oversight, illustrating how local producers adjust cost structures while safeguarding intellectual property. Despite some reshoring initiatives, most headlamp LED modules destined for U.S. and European vehicles still originate from Asia-based packagers, reinforcing cross-regional supply interdependence within the Flip-Chip LED market.

Middle East and Africa, South America, and other emerging regions together held a small share of 2025 revenue but show above-average growth. Smart-city rollouts in Saudi Arabia and the United Arab Emirates specify flip-chip streetlights capable of withstanding 50 °C ambient temperatures. Sub-Saharan retrofit programs financed under multilateral energy-access schemes replicate Asia's early LED adoption curve, promising steady upside for the Flip-Chip LED market once supply chain constraints ease. South American demand is concentrated in Brazil and Argentina, where harmonization with European automotive lighting standards opens a direct channel for adaptive headlamp modules.

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Penguin Solutions Inc. (Cree Inc.)

- ams-OSRAM AG (Osram Opto Semiconductors GmbH)

- Seoul Semiconductor Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Epistar Corporation

- LG Innotek Co., Ltd.

- Lumileds Holding B.V.

- Lextar Electronics Corporation

- Genesis Photonics Inc.

- HC SemiTek Corporation

- Lattice Power Corporation

- Toyoda Gosei Co., Ltd.

- Everlight Electronics Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Kinglight Co., Ltd.

- Amkor Technology

- Siliconware Precision Industries (SPIL)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Mini-Led Adoption In Large-Format Displays

- 4.2.2 Rapid Penetration In Automotive Adaptive Lighting Modules

- 4.2.3 Energy-Efficiency Mandates Across Asia-Pacific and Europe

- 4.2.4 Lower Total-Cost-Of-Ownership Versus Wire-Bond LEDs

- 4.2.5 Micro-LED Pilot Production Driving Wafer-Level Flip-Chip Demand

- 4.2.6 Defense and Aerospace Push For High-G Hard-Mounted Emitters

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Flip-Chip Packaging Lines

- 4.3.2 Competitive Pressure From Vertical Thin-Film LEDs

- 4.3.3 Sub-P0.5 Repairability And Yield Losses

- 4.3.4 Indium Bump Reliability Under Thermal Cycling

- 4.4 Regulatory Landscape

- 4.5 Technology Analysis

- 4.6 Industry Value Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material System

- 5.1.1 GaN

- 5.1.2 AlGaInP

- 5.1.3 Other Material Systems

- 5.2 By Wavelength / Color

- 5.2.1 Blue

- 5.2.2 White

- 5.2.3 Red

- 5.2.4 Green

- 5.2.5 Other Wavelengths / Colors

- 5.3 By Power Class

- 5.3.1 Low Power

- 5.3.2 Mid Power

- 5.3.3 High Power

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.2 Automotive Lighting

- 5.4.3 Displays and Signage

- 5.4.4 Backlighting

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Penguin Solutions Inc. (Cree Inc.)

- 6.4.4 ams-OSRAM AG (Osram Opto Semiconductors GmbH)

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 San'an Optoelectronics Co., Ltd.

- 6.4.7 Epistar Corporation

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lumileds Holding B.V.

- 6.4.10 Lextar Electronics Corporation

- 6.4.11 Genesis Photonics Inc.

- 6.4.12 HC SemiTek Corporation

- 6.4.13 Lattice Power Corporation

- 6.4.14 Toyoda Gosei Co., Ltd.

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Refond Optoelectronics Co., Ltd.

- 6.4.17 Nationstar Optoelectronics Co., Ltd.

- 6.4.18 Kinglight Co., Ltd.

- 6.4.19 Amkor Technology

- 6.4.20 Siliconware Precision Industries (SPIL)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment