PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063982

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063982

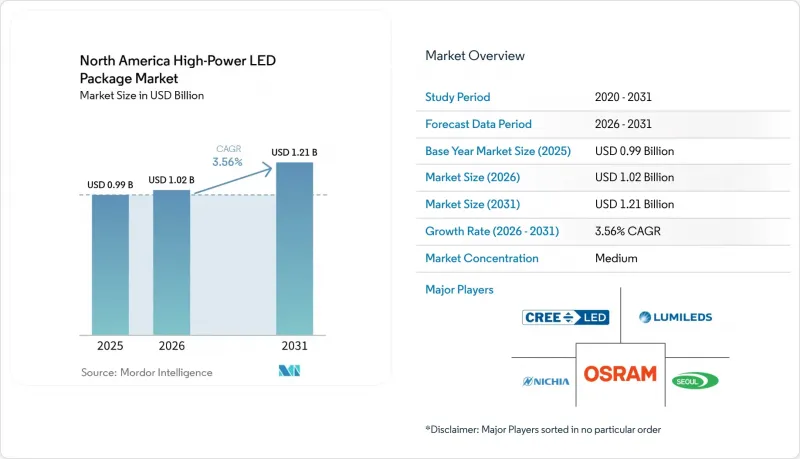

North America High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america high-power LED package market size is projected to expand from USD 0.99 billion in 2025 and USD 1.02 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031.

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, COB, and Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America High-Power LED Package Market Trends and Insights

Government-Mandated Phase-Out of Inefficient Lamps

Federal and state rules are forcing incandescent and fluorescent products off shelves on a compressed timeline, triggering a sharp pull in demand for high-power packages that can clear 120 lumens per watt within existing fixture envelopes. The U.S. Department of Energy rule, effective July 2028, and six state bans enacted between 2024 and 2027 anchor this shift, making 3-watt to 10-watt emitters the default choice for retrofit downlights and track heads. Distributors are liquidating legacy inventory ahead of cut-off dates, while luminaire brands are fast-tracking chip-on-board and multi-die modules that meet efficacy, lumen density, and color-quality targets. Vendors with in-house phosphor and thermal expertise benefit because compliance audits expose under-performing products to recall risk. The result is a structural growth tailwind that will persist through the middle of the forecast window.

Rapid LED Penetration in Automotive Headlamps

Adaptive driving beam approval is reshaping the front-lighting bill of materials. Passenger-car LED penetration already exceeds 70%, and pixel-level systems are moving from luxury to mass-market models under new regulatory headlamp glare rules. Matrix arrays place dozens of individually addressable dice onto compact substrates, favoring high-power packages with low thermal resistance and precise binning. LG Innotek's ultra-thin pixel module, which won a CES 2026 award, illustrates how shrinking form factors and vehicle-to-everything projections are turning lighting into a safety and communications asset. Tier-one suppliers holding 69.2% automotive share are leveraging patent pools and cross-licenses to secure design wins, locking in multi-year volume ramps as 2027 model launches approach.

Thermal Management and Reliability Challenges Above 1 A Drive

Driving packages at currents above 1 ampere elevates junction temperatures beyond 150 °C, cutting lifetime in half for every 10 °C rise. Designers must adopt ceramic boards, vapor chambers, or active cooling, which adds cost and weight. Thermal droop reduces efficacy from 150 lumens per watt at 350 mA to near 120 lumens per watt at 1.5 A, negating emitter-count savings. Interface material degradation and solder fatigue under cycling raise warranty exposure, so many luminaires derate to 70% of nameplate current. Until breakthroughs in substrate or phosphor materials lower heat at the source, high-current operation will remain cost-capped in cost-sensitive general lighting.

Other drivers and restraints analyzed in the detailed report include:

- 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- Dark-Sky Regulations Driving Low-Blue NightScape Packages

- Helium Shortage Disrupting GaN Wafer Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The above 10 watt tier of the North America high-power LED package market size is on a 4.11% CAGR path as sports venues, warehouses, and roadway operators favor single-package outputs above 10,000 lumens. Chip-on-board formats dominate because they mount bare dice directly onto metal-core boards, delivering thermal resistance under 2 K/W and supporting smaller heatsinks. In 2025 the 1 watt-3 watt tier retained 47.88% share, serving retrofit downlights that prize footprint compatibility with legacy housings.

Growth momentum is shifting as the DOE efficacy rule and 8K broadcast contracts encourage designers to consolidate flux into fewer optical points, cutting assembly labor and reflector count. Vendors such as Lumileds introduced LUXEON CS in March 2026 to exploit this trend, offering LES diameters from 6.3 mm to 22 mm and CRI options of 90 and 95. The 3 watt-10 watt range remains a transitional bracket for high-bay fixtures but lacks the clear economic edge enjoyed by either extreme.

List of Companies Covered in this Report:

- Nichia Corporation

- ams OSRAM International GmbH

- Lumileds Holding B.V.

- Cree LED Inc.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- Luminus Devices Inc.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Signify N.V.

- LITE-ON Technology Corporation

- Broadcom Inc.

- Foshan Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Mandated Phase-Out of Inefficient Lamps

- 4.2.2 Rapid LED Penetration in Automotive Headlamps

- 4.2.3 Stabilization of High-Power LED Package ASPs

- 4.2.4 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- 4.2.5 Dark-Sky Regulations Driving Low-Blue Nightscape Packages

- 4.2.6 PoE Smart-Lighting Designs Favoring High-Voltage CSP LEDs

- 4.3 Market Restraints

- 4.3.1 Thermal Management and Reliability Challenges Above 1 A Drive

- 4.3.2 Up-Front Cost Premium Versus Mid-Power LEDs

- 4.3.3 Helium Shortage Disrupting GaN Wafer Processing

- 4.3.4 Geopolitical Risk to Rare-Earth Red Phosphors Supply

- 4.4 Technology Outlook

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams OSRAM International GmbH

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Cree LED Inc.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Bridgelux Inc.

- 6.4.11 Luminus Devices Inc.

- 6.4.12 Epistar Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 NationStar Optoelectronics Co., Ltd.

- 6.4.15 Hongli Zhihui Group Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Signify N.V.

- 6.4.18 LITE-ON Technology Corporation

- 6.4.19 Broadcom Inc.

- 6.4.20 Foshan Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment