PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064349

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064349

India High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

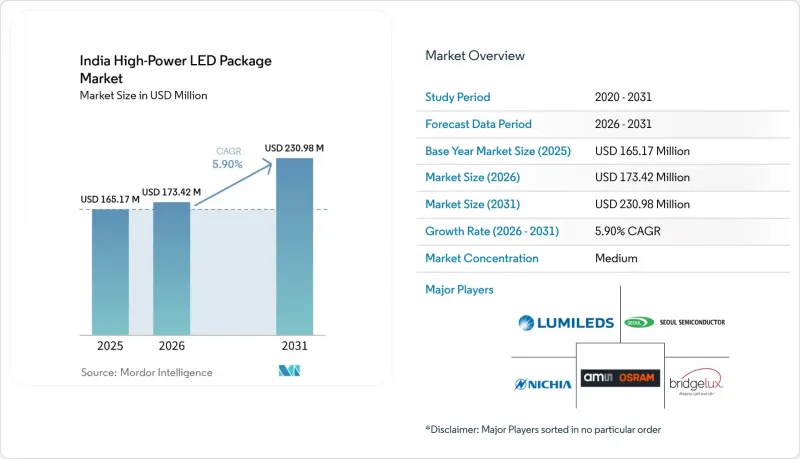

According to Mordor Intelligence, the india high-Power lED package market size is expected to increase from USD 165.17 million in 2025 to USD 173.42 million in 2026 and reach USD 230.98 million by 2031, growing at a CAGR of 5.9% over 2026-2031.

This report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-Die Packages (SMD / Discrete), Multi-Die Packages (SMD), COB (Chip-On-Board), and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

India High-Power LED Package Market Trends and Insights

Government Push Through UJALA and SLNP Programs

Bulk procurement under the Unnat Jyoti by Affordable LEDs for All and Street Lighting National Program has seeded a nationwide installed base of 36.87 crore LED bulbs and 1.34 crore streetlights, creating a predictable aftermarket for high-power replacements. Unit prices fell by 75% within the first 16 months of UJALA, normalizing LEDs as the default light source and widening the addressable base for domestic assemblers. As EESL pivots new tenders toward smart, dimmable luminaires, package suppliers must now integrate drivers and IoT controls to stay qualified. Municipalities that adopted SLNP fixtures face seven-to-ten-year replacement cycles, ensuring steady demand for 15 W-50 W packages with higher lumen maintenance. This dynamic favors vertically integrated firms that can meet Bureau of Indian Standards photometric and safety tests while keeping costs aligned with government price ceilings.

Rapid Urban Infrastructure Expansion and Smart City Projects

Smart Cities Mission allocations have financed LED retrofits across 100 cities, with Ahmedabad investing INR 5 billion (USD 56.7 million) to upgrade 210 000 poles and Kochi spending INR 300 million (USD 3.4 million) on 40 000 networked luminaires. These large contracts specify lumen maintenance above 50 000 hours and a color rendering index above 80, raising entry barriers for low-cost imports. Guwahati's 2025 project cut energy use by 60% while stretching maintenance intervals to 50 000 hours, validating the total-cost-of-ownership case for premium packages. Decentralized tendering across states rewards regional distributors that can customize thermal designs for local climate zones. As city contracts increasingly require integrated sensors, suppliers with in-house driver and RF capabilities gain a competitive edge.

High Import Dependence for Epitaxy and Packaging Equipment

Indian manufacturers still source most MOCVD reactors, lithography lines, and wire-bonders from overseas suppliers such as Aixtron, Veeco, and ASM Pacific, constraining upstream value addition. A single reactor costs USD 3-5 million, while a full fab can exceed USD 100 million, placing such investments beyond the reach of mid-sized lighting firms. Halonix reduced reliance on imports from 60% in FY2021 to 24% in FY2025 by localizing assembly, yet epitaxial wafers and chips still arrive from Taiwan and South Korea. The PLI scheme targets 75-80% domestic value addition by 2029, but achieving this goal will require shared fabrication hubs or joint ventures between equipment vendors. Without such moves, currency volatility and geopolitical risks will continue to pressure margins and supply assurance for high-power packages.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost-Per-Lumen of High-Power LED Packages

- Automotive Industry Shift to LED Headlamps

- Thermal Management Challenges in Tropical Climate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 1 W-3 W class dominated the India High-Power LED package market, capturing 47.84% share. Meanwhile, the Above 10 W segment is set to grow at a 6.47% CAGR, continuing through 2031. Above 10 W packages now supply high-mast streetlights, industrial bays, and sports venues, where users accept higher purchase costs in exchange for better total cost of ownership. The India High-Power LED package market in this band is benefiting from stadium retrofits that demand 20-30% energy savings and tighter beam angles. Packages exceeding 50 W typically employ ceramic substrates and precision optics, driving collaboration between diode makers and luminaire houses. Installers view longer service intervals as critical because tower-top maintenance remains cost-intensive. Meanwhile, the legacy 1 W-3 W class, once propelled by UJALA bulbs, is entering a slow-replacement phase in urban homes, limiting its growth potential.

Market participants now design modular engines that group six to eight 15 W LED arrays on a single plate, cutting assembly steps for high-mast luminaires. This system-integration trend rewards suppliers that co-design drivers, optics, and thermal paths, not merely diodes. In rural electrification schemes, higher-wattage solar-streetlight kits have begun to specify 20-W to 30-W arrays paired with Li-ion batteries, pushing above 10 W packages further into off-grid applications. Consequently, contract manufacturers expanding PLI-backed capacity are focusing CAPEX on automated assembly lines rated up to 200 W modules.

List of Companies Covered in this Report:

- Nichia Corp.

- Everlight Electronics Co., Ltd.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED (Wolfspeed, Inc.)

- Samsung Electronics Co., Ltd. (LED Business)

- MLS Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn. Bhd.

- LG Innotek Co., Ltd.

- Surya Roshni Ltd.

- Havells India Ltd.

- Bajaj Electricals Ltd.

- Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- Crompton Greaves Consumer Electricals Ltd.

- Halonix Technologies Pvt. Ltd.

- Syska LED Lights Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Push Through UJALA and SLNP Programs

- 4.2.2 Rapid Urban Infrastructure Expansion and Smart City Projects

- 4.2.3 Declining Cost-per-Lumen of High-Power LED Packages

- 4.2.4 Automotive Industry Shift to LED Headlamps

- 4.2.5 Rise of Horticulture LED Farms in Controlled-Environment Agriculture

- 4.2.6 Surge in High-Mast Sports Lighting Upgrades for Upcoming Events

- 4.3 Market Restraints

- 4.3.1 High Import Dependence for Epitaxy and Packaging Equipment

- 4.3.2 Thermal Management Challenges in Tropical Climate

- 4.3.3 Fragmented Standards for High-Power LED Reliability Testing

- 4.3.4 Supply-Chain Volatility for SiC Substrates

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1W-3W

- 5.1.2 3W-10W

- 5.1.3 Above 10W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Other Architectures (CSP, Flip-chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corp.

- 6.4.2 Everlight Electronics Co., Ltd.

- 6.4.3 Osram Opto Semiconductors GmbH

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED (Wolfspeed, Inc.)

- 6.4.7 Samsung Electronics Co., Ltd. (LED Business)

- 6.4.8 MLS Co., Ltd.

- 6.4.9 Bridgelux, Inc.

- 6.4.10 Citizen Electronics Co., Ltd.

- 6.4.11 Edison Opto Corp.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 Surya Roshni Ltd.

- 6.4.15 Havells India Ltd.

- 6.4.16 Bajaj Electricals Ltd.

- 6.4.17 Wipro Lighting (Wipro Enterprises Pvt. Ltd.)

- 6.4.18 Crompton Greaves Consumer Electricals Ltd.

- 6.4.19 Halonix Technologies Pvt. Ltd.

- 6.4.20 Syska LED Lights Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment