PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063934

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063934

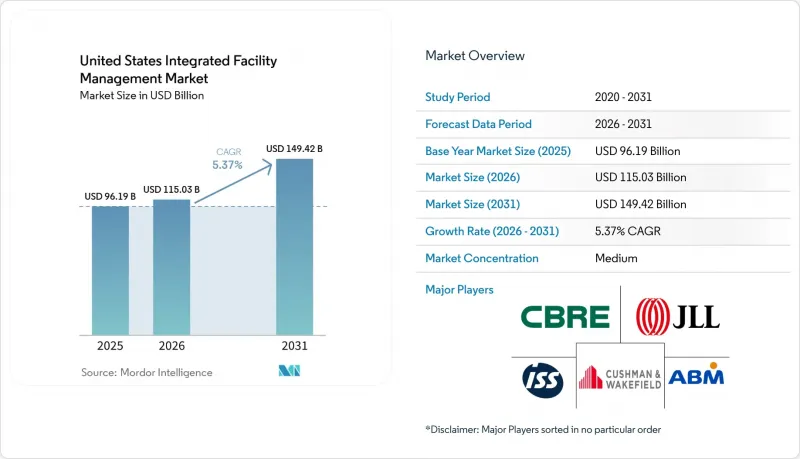

United States Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states integrated facility management market size was valued at USD 96.19 billion in 2025 and estimated to grow from USD 115.03 billion in 2026 to reach USD 149.42 billion by 2031, at a CAGR of 5.37% during the forecast period 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Integrated Facility Management Market Trends and Insights

Growing Demand for Smart, Connected Buildings

Smart building infrastructure is becoming a core operating layer in the United States integrated facility management market, rather than a separate technology upgrade. Smart-building node installations are projected to reach 115 million in 2026, which means more facilities are sending live operating data into day-to-day service workflows. That data now supports real-time HVAC optimization, occupancy-linked energy control, and predictive fault detection, which reduces the need for large manual inspection teams. As a result, many contracts are shifting away from labor-hour commitments and toward uptime, comfort, and energy-performance targets, which tends to favor larger vendors with stronger digital platforms. JLL reported that 28% of FM organizations embedded AI in operations in 2025, while the figure reached 46% among enterprises with more than 100,000 employees, and 92% had already piloted AI tools in real estate or FM functions. Johnson Controls reinforced that direction in April 2026 when it acquired Nantum AI to strengthen autonomous HVAC control, with the company pointing to energy savings above 10% per building.

Rising Outsourcing to Control Operating Expenditure

Cost pressure has become one of the clearest reasons buyers are moving deeper into the United States IFM market. JLL found in 2025 that 84% of CRE and FM leaders identified escalating costs and budget constraints as a top concern, while 81% said cost efficiency was a leading priority for the following year. That pressure matters most in first-time outsourcing, where organizations are moving from in-house delivery into bundled or fully integrated contracts and creating new addressable demand. IFMA reported a net 19% point shift toward greater outsourcing in its Q4 2025 FM Market Pulse, with utilities, healthcare, and professional services showing especially strong movement. Buyers are also becoming more selective in how they choose vendors, and JLL said 78% of organizations ranked deep business understanding as the top selection factor rather than the lowest unit rate. That preference supports longer contract relationships because providers that understand operations, compliance, and occupancy patterns are harder to replace once the service model is embedded.

Fragmented Vendor Landscape Limiting Standardization

Fragmentation remains a structural drag on the United States integrated facility management market because service delivery becomes harder to standardize when multiple vendors, systems, and local practices overlap. The problem becomes more severe in large portfolios where cleaning, security, engineering, catering, and workplace systems are still procured or tracked separately. Each additional interface increases the risk of inconsistent logs, delayed work orders, incomplete data transfers, and limited visibility into service-level compliance. International Facility Management Association has also emphasized the importance of integrated KPI visibility and audit traceability in modern FM operations, particularly as regulatory and internal reporting requirements continue to increase. As a result, fragmentation is no longer just an administrative challenge because it directly impacts cost control, operational performance tracking, and audit defensibility across large enterprise accounts.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Emphasis on Energy-Efficient Operations

- Accelerated Post-Pandemic Hybrid Workplace Adoption

- Shortage Of Skilled MEP And HVAC Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management segment held 56.28% of the United States integrated facility management market share in 2025, which made it the largest service category by revenue. In the United States IFM industry, that lead reflects the broad role of office support, security, cleaning, catering, and workplace experience services across outsourced contracts. These activities are now treated as a core part of occupier value rather than a peripheral support layer, especially in commercial and institutional settings where user experience matters more. Hard facility management segment, which covers asset management, MEP and HVAC services, fire systems and safety, and other technical functions, is projected to expand at a 5.83% CAGR through 2031. The US IFM market size for technical services is rising faster because energy rules, aging mechanical systems, and connected building controls are all pushing more work into non-discretionary maintenance budgets.

That split shows why soft services still drive volume while hard services often drive stickier contract economics and stronger margins. Within Hard FM, MEP and HVAC remain the most capacity-constrained areas because technician shortages are limiting how much of the available demand providers can actually serve. Within Soft FM, security is moving through a technology-led upgrade cycle as AI-enabled access control, remote monitoring, and integrated visitor systems replace older guard-heavy models in many buildings. That upgrade changes site economics because digital layers can improve oversight and standardization without relying on the same staffing mix used in legacy contracts. Johnson Controls' acquisition of Nantum AI in April 2026 captured the broader direction of travel, where analytics, building controls, and hard-services delivery are converging into a more differentiated technical offer.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated (JLL)

- Cushman & Wakefield plc

- ABM Industries Inc.

- ISS A/S

- Sodexo S.A.

- Aramark Corporation

- EMCOR Group, Inc.

- Compass Group plc

- Honeywell International Inc.

- Veolia Environnement S.A.

- Brookfield Global Integrated Solutions (BGIS)

- GDI Integrated Facility Services Inc.

- ServiceMaster Global Holdings, Inc.

- Johnson Controls International plc

- Allied Universal

- Cushman Facility Services, Inc.

- CBM Managed Services

- Trane Technologies plc

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Smart, Connected Buildings

- 4.2.2 Rising Outsourcing to Control Operating Expenditure

- 4.2.3 Increasing Emphasis on Energy-Efficient Operations

- 4.2.4 Accelerated Post-Pandemic Hybrid Workplace Adoption

- 4.2.5 Federal Push for Carbon-Neutral Government Facilities

- 4.2.6 Emergence of Data-Driven Predictive Maintenance

- 4.3 Market Restraints

- 4.3.1 Fragmented Vendor Landscape Limiting Standardization

- 4.3.2 Shortage of Skilled MEP and HVAC Technicians

- 4.3.3 High Cybersecurity Risk in IoT-Enabled FM Platforms

- 4.3.4 Inflation-Driven Contract Cost Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft FM

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated (JLL)

- 6.4.3 Cushman & Wakefield plc

- 6.4.4 ABM Industries Inc.

- 6.4.5 ISS A/S

- 6.4.6 Sodexo S.A.

- 6.4.7 Aramark Corporation

- 6.4.8 EMCOR Group, Inc.

- 6.4.9 Compass Group plc

- 6.4.10 Honeywell International Inc.

- 6.4.11 Veolia Environnement S.A.

- 6.4.12 Brookfield Global Integrated Solutions (BGIS)

- 6.4.13 GDI Integrated Facility Services Inc.

- 6.4.14 ServiceMaster Global Holdings, Inc.

- 6.4.15 Johnson Controls International plc

- 6.4.16 Allied Universal

- 6.4.17 Cushman Facility Services, Inc.

- 6.4.18 CBM Managed Services

- 6.4.19 Trane Technologies plc

- 6.4.20 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment