PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064416

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064416

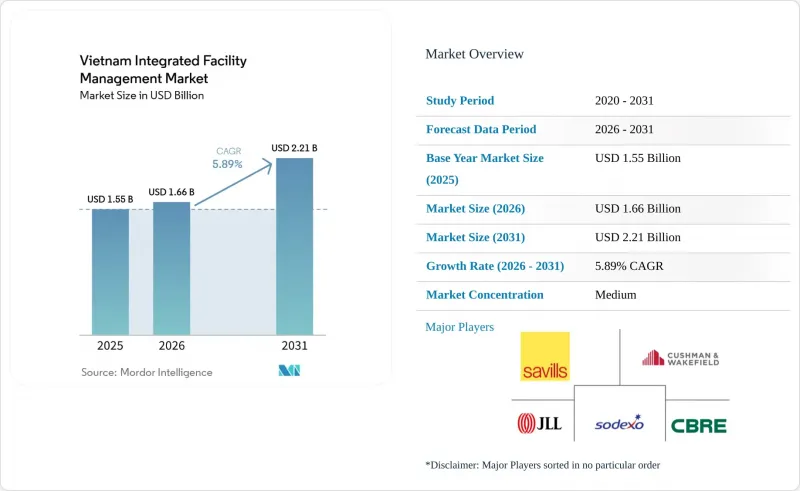

Vietnam Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vietnam integrated facility management market size is projected to be USD 1.55 billion in 2025, USD 1.66 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Integrated Facility Management Market Trends and Insights

Rising FDI And Industrial Park Expansion

The Vietnam integrated facility management market is gaining direct support from new industrial park supply and from the steady rise in higher-value manufacturing activity across both the north and the south. New factories, logistics hubs, and supplier campuses not only add floor area but also introduce technical systems, safety procedures, and operating protocols that require a single accountable service model rather than multiple disconnected vendors. This is especially visible in Bac Ninh, Bac Giang, and Hai Phong, where electronics, semiconductor assembly, and precision manufacturing tenants need cleanroom control, uninterrupted utilities, calibrated maintenance schedules, and auditable site security practices. The same pattern is visible in southern corridors such as Binh Duong and Dong Nai, where industrial expansion is creating a pipeline of bundled, technically intensive FM contracts. Savills Vietnam reported 42 newly approved industrial park projects in 2025, adding close to 8,400 hectares of leasable land, which supports a multi-year asset pipeline for the Vietnam integrated facility management market as those parks move toward occupancy. As Vietnam attracts more process-critical production, the service scope within the Vietnam integrated facility management market shifts upward from reactive site support toward preventive engineering, compliance management, and continuous operations assurance.

Rapid Urbanization and Commercial Real Estate Growth

Vietnam integrated facility management market is also expanding because urban construction in Hanoi and Ho Chi Minh City continues to add a large stock of buildings that need organized lifecycle management. Vietnam Television reported that the two cities had more than 2,870 completed high-rise buildings by late 2024, which shows that the demand base for recurring FM services is broad and still expanding. The opportunity is strongest in newer Grade A and upper-tier commercial properties because those assets usually include centralized building management systems, HVAC zoning, smart access controls, and energy monitoring tools that require trained operators rather than single-line contractors. Green-certified office development is reinforcing that pattern because owners need maintenance regimes that preserve certification outcomes and support tenant expectations around energy, indoor air quality, and service transparency. West Hanoi and central Ho Chi Minh City are showing this movement most clearly, but the spillover is reaching Da Nang and Hai Phong as office, mixed-use, and logistics projects become more institutional in design. The same urban expansion is also lifting demand from hospitality, retail, and technology office occupiers, which need more specialized cleaning, support, security, and asset-care programs than older buildings typically required.

Fragmented And Unorganized Provider Landscape

The Vietnam integrated facility management market is still held back by a service base that remains highly fragmented across cleaning firms, security companies, maintenance vendors, and small local support providers. Vietnam Television noted that the number of new FM-related businesses has been rising quickly, but this expansion has not created a comparable rise in standardized delivery quality or broad multi-service capability. That makes vendor consolidation harder for occupiers because many domestic operators can manage one or two service lines effectively, but only a limited number can absorb a full IFM mandate with the right staffing depth, documentation discipline, and insurance coverage. Mid-market properties are the most exposed to this issue because they often rely on informal or narrowly scoped subcontracting arrangements that are difficult for integrated providers to displace on price alone. The absence of a compulsory national quality framework for FM keeps underqualified players in the bidding pool and caps average contract value across the Vietnam integrated facility management market. This same landscape also slows the conversion of domestic SMEs, which often remain unconvinced that integrated contracts offer enough value to justify a shift away from low-cost single-service procurement.

Other drivers and restraints analyzed in the detailed report include:

- Cost Optimization Through Outsourcing Non-Core FM Activities

- Digital Transformation and Smart Building Technology Adoption

- Shortage Of Qualified and Skilled FM Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management (FM) held 55.7% of Vietnam integrated facility management (IFM) market share in 2025, reflecting the wide use of cleaning, catering, pest control, concierge, and support services across commercial, hospitality, industrial, and residential properties. This segment remains large because labor-intensive environments, including hotels, hospitals, food processing units, and high-traffic office towers, require consistent headcount deployment and service routines that translate into steady contract value. The Vietnam IFM industry also gives Soft FM added weight because hygiene, occupancy support, and front-of-house services remain essential even when technical systems are less advanced. Bundled FM is gaining ground inside this mix, as occupiers prefer one contract that combines site support, asset care, and compliance reporting rather than a patchwork of separate vendors. LOTUS V4 adds another push because certified properties now need more structured performance records and standardized building operations, which fit better with coordinated service models than with fragmented outsourcing.

Hard FM is projected to grow at a 6.4% CAGR from 2026 to 2031, making it the fastest-growing service type in the Vietnam IFM market. The main reason is the technical profile of new assets entering operation, especially factories, ready-built industrial space, premium offices, and data-linked facilities that cannot rely on periodic repair crews alone. Semiconductor assemblers, electronics manufacturers, and EV component producers need planned maintenance, calibrated engineering support, fire system certification, and continuous MEP uptime to protect production quality and avoid shutdown risk. KCN Vietnam highlighted the rise of LEED Gold ready-built factories in locations such as Hai Phong, Dong Nai, and Bac Ninh, which reinforces the movement toward permanent on-site engineering teams and digitally supported maintenance routines. Within the Vietnam IFM industry, this means Hard FM is moving from a support function to a core value driver for contracts tied to advanced manufacturing and institutional-grade real estate.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Savills Vietnam Ltd.

- ISS A/S

- Sodexo SA

- G4S Plc

- Cushman AND Wakefield plc

- Knight Frank LLP

- Colliers International Group Inc.

- FPT Facility Management JSC

- VinService JSC

- BVFM Facility Management Co. Ltd.

- Newtecons FM Co. Ltd.

- PMC Building Services and Trading Co. Ltd.

- NoVa Facility Management Co., Ltd.

- A2Z Facility Services Co. Ltd.

- Aplitek Services Co. Ltd.

- Vinhomes Property and Facility Management

- Anabuki Clean Service Vietnam Co. Ltd.

- REE Corporation (Facility Services Division)

- Detech Facility Management Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Industry Value-Chain Analysis

- 4.4 Technology Analysis

- 4.5 Regulatory Landscape

- 4.6 Market Drivers

- 4.6.1 Rising FDI Inflows and Industrial Park Expansion

- 4.6.2 Rapid Urbanization and Commercial Real Estate Growth

- 4.6.3 Cost Optimization Pressure Driving Outsourcing of Non-Core FM Activities

- 4.6.4 Digital Transformation and Smart Building Technology Adoption

- 4.6.5 Growing ESG Compliance Requirements and Green Building Certification Adoption

- 4.6.6 Expanding Hospitality, Retail, and Technology Office Sectors Requiring Specialized FM

- 4.7 Market Restraints

- 4.7.1 Highly Fragmented and Unorganized FM Service Provider Landscape

- 4.7.2 Shortage of Qualified and Skilled FM Professionals

- 4.7.3 High Upfront Capital Investment Requirements for Integrated FM Technology Platforms

- 4.7.4 Low Awareness of Integrated FM Value Proposition Among Domestic SMEs

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Savills Vietnam Ltd.

- 6.4.4 ISS A/S

- 6.4.5 Sodexo SA

- 6.4.6 G4S Plc

- 6.4.7 Cushman AND Wakefield plc

- 6.4.8 Knight Frank LLP

- 6.4.9 Colliers International Group Inc.

- 6.4.10 FPT Facility Management JSC

- 6.4.11 VinService JSC

- 6.4.12 BVFM Facility Management Co. Ltd.

- 6.4.13 Newtecons FM Co. Ltd.

- 6.4.14 PMC Building Services and Trading Co. Ltd.

- 6.4.15 NoVa Facility Management Co., Ltd.

- 6.4.16 A2Z Facility Services Co. Ltd.

- 6.4.17 Aplitek Services Co. Ltd.

- 6.4.18 Vinhomes Property and Facility Management

- 6.4.19 Anabuki Clean Service Vietnam Co. Ltd.

- 6.4.20 REE Corporation (Facility Services Division)

- 6.4.21 Detech Facility Management Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment