PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064488

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064488

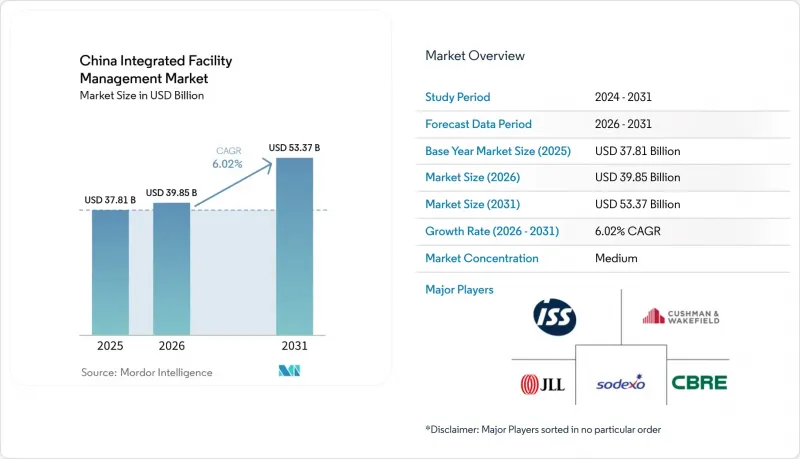

China Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china integrated facility management market size was valued at USD 37.81 billion in 2025 and is estimated to grow from USD 39.85 billion in 2026 to reach USD 53.37 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031).

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Integrated Facility Management Market Trends and Insights

Rapid Growth of Real Estate, Office, And Data Centre Industries

Data centers are creating a distinct stream of demand in the China integrated facility management market because they need uninterrupted engineering support, tighter response windows, and stronger performance validation. This is different from conventional office facilities, where the service mix is broader, but the engineering threshold is often lower. The Data Center Green Development Action Plan set requirements around lower power usage effectiveness and rising renewable energy use, which has increased the need for energy management, cooling optimization, and electrical system oversight within hard FM services. Office parks and corporate campuses continue to add to this demand channel, especially where technology, intelligent manufacturing, and new energy firms need stable and bundled support services. Providers that can handle specialized testing, cooling, compliance, and account management are therefore gaining stronger contract positions in the China integrated facility management (IFM) market.

Rising Outsourcing of Third-Party FM Services in China

The China integrated facility management market is also benefiting from a gradual shift toward third-party delivery, as occupiers seek clearer accountability and better service integration. This shift is visible in large enterprise portfolios, where providers are being asked to combine workplace services, maintenance, digital tools, and performance reporting within a single operating model. Recent product and contract launches show how outsourcing is moving beyond labour substitution and toward a platform-based operating approach. Digital twin monitoring is also being used to support cleaning, maintenance, landscaping, and hygiene under one service structure. As more occupiers seek bundled execution instead of fragmented procurement, the China IFM market is likely to reward vendors that can combine site delivery, digital visibility, and national account management.

Lack Of Standardization in Pricing, Referencing, And Contracts

A lack of standard pricing and contract structures still slows the China integrated facility management (IFM) market because it keeps many tenders focused on lowest-cost selection. That approach makes it harder for buyers to distinguish between basic labour supply and genuinely integrated delivery with technical depth. When procurement leans too heavily on price, providers with stronger engineering or digital capability can struggle to defend margins even when their service quality is higher. This also creates weaker renewal dynamics, because clients may see inconsistent outcomes when contracts are awarded without clear quality benchmarks. Until contract templates, service definitions, and performance baselines become more consistent, the China integrated facility management market will continue to face friction in value-based procurement.

Other drivers and restraints analyzed in the detailed report include:

- Mandate of Energy Efficiency and Focus on Sustainable Solutions

- Acceleration Of Urbanization and Growth of Real Estate Sector in China

- Complex Legal Requirements from National and State-Level Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 55.78% of China integrated facility management (IFM) market share in 2025, which kept it as the largest service group across commercial, institutional, and campus environments. Cleaning, catering, and office support remained the most widely outsourced activities because they are visible, repetitive, and easier for occupiers to centralize under one vendor. This part of the China IFM market also benefits from the spread of larger enterprise campuses, where employers need consistent support services across more complex sites. As contracts become broader, clients are increasingly bundling front-of-house support, cleaning, workplace services, and selected compliance tasks into one package rather than sourcing them separately. That shift supports stable demand for Soft FM even as the service mix becomes more data-aware and process-driven.

Hard FM is the fastest-growing service category, with the China integrated facility management market size for this segment advancing at a 6.73% CAGR from 2026 to 2031. The growth is being driven by asset management, MEP services, HVAC oversight, and other engineering-intensive work tied to uptime, safety, and energy control. Data center policy has added to this demand because operators need tighter oversight of cooling, electrical systems, and performance tracking under formal efficiency targets. Fire systems and safety services are also becoming more specialized as clients look for documented maintenance, audit trails, and better fault response across mission-critical sites. Within the China integrated facility management industry, this leaves hard FM well placed to capture a larger share of new integrated contracts where technical assurance matters as much as routine service coverage.

List of Companies Covered in this Report:

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- ISS A/S

- Sodexo SA

- Savills plc

- Colliers International Group Inc.

- GDI Integrated Facility Services Inc.

- China Overseas Property Holdings Limited

- Poly Property Services Co. Ltd.

- Shanghai Xincheng Facility Management Ltd.

- Sichuan Huaming Property Management Co. Ltd.

- Shenzhen Capital Property Management Co. Ltd.

- Guangzhou Guangwu Property Management Ltd.

- Beijing Winn Property Management Co. Ltd.

- Secom Co. Ltd.

- Diebold Nixdorf Inc.

- Sangfor Technologies Inc.

- Qingdao Hisense Facility Management Co. Ltd.

- Greentown Service Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acceleration of Smart Building Initiatives in Tier-1 Cities

- 4.2.2 Mandated Energy-Efficiency Targets for Public Facilities

- 4.2.3 Rising Outsourcing of Non-Core Operations by SOEs

- 4.2.4 Expansion of Industrial Parks in Western China

- 4.2.5 Growing Demand for Integrated Contracts in Healthcare Campuses

- 4.2.6 Deployment of 5G-Enabled Predictive Maintenance Platforms

- 4.3 Market Restraints

- 4.3.1 Talent Shortages in Specialized Hard FM Services

- 4.3.2 Persistent Price-Based Bidding in Government Tenders

- 4.3.3 Low Penetration of IFM in Small and Medium Enterprises

- 4.3.4 Regulatory Uncertainty Around Private-Public Partnership Models

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End-User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Cushman & Wakefield plc

- 6.4.4 ISS A/S

- 6.4.5 Sodexo SA

- 6.4.6 Savills plc

- 6.4.7 Colliers International Group Inc.

- 6.4.8 GDI Integrated Facility Services Inc.

- 6.4.9 China Overseas Property Holdings Limited

- 6.4.10 Poly Property Services Co. Ltd.

- 6.4.11 Shanghai Xincheng Facility Management Ltd.

- 6.4.12 Sichuan Huaming Property Management Co. Ltd.

- 6.4.13 Shenzhen Capital Property Management Co. Ltd.

- 6.4.14 Guangzhou Guangwu Property Management Ltd.

- 6.4.15 Beijing Winn Property Management Co. Ltd.

- 6.4.16 Secom Co. Ltd.

- 6.4.17 Diebold Nixdorf Inc.

- 6.4.18 Sangfor Technologies Inc.

- 6.4.19 Qingdao Hisense Facility Management Co. Ltd.

- 6.4.20 Greentown Service Group Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment