PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064459

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064459

Thailand Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

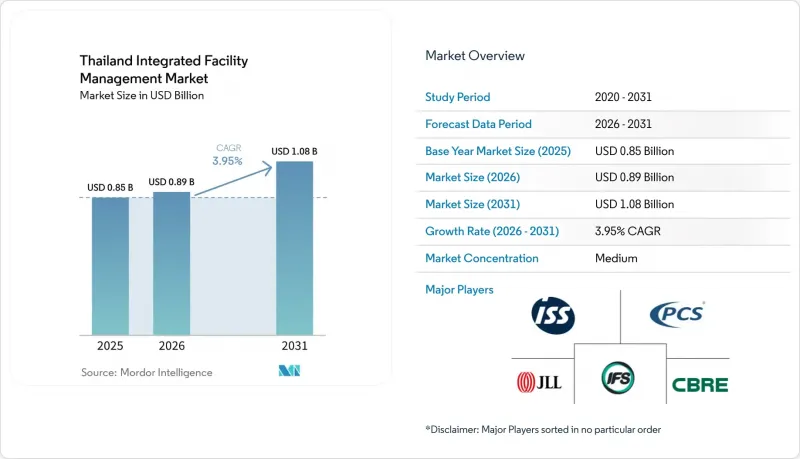

According to Mordor Intelligence, the thailand integrated facility management market size is projected to expand from USD 0.85 billion in 2025 and USD 0.89 billion in 2026 to USD 1.08 billion by 2031, registering a CAGR of 3.95% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Service, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Integrated Facility Management Market Trends and Insights

Government Investment in Eastern Economic Corridor Industry Parks Drives Integrated FM Demand

The EEC remains the clearest demand engine for the Thailand integrated facility management market because it concentrates large industrial estates, transport links, and new infrastructure within a relatively compact operating corridor. Its 2023-2027 development plan targets THB 500 billion (USD 14.5 billion) in actual investment, while developed industrial land in the EEC reached 110,275 rai by H1 2025, up 7% from the end of 2024. That scale matters because multi-tenant estates need providers that can coordinate engineering, security, cleaning, compliance, and reporting across many buildings instead of serving a single site at a time. U-Tapao Airport's Eastern Aviation City, Laem Chabang Port Phase 3, and the high-speed rail link are creating permanent facilities where MEP upkeep, fire systems, and building management systems become core service lines rather than optional add-ons. In May 2025, Prospect Development announced THB 6.5 billion (USD 188.4 million), equivalent to USD 188.4 million, for the Bangpakong Industrial Estate in the EEC, aimed at automotive, digital, and food processing users that require stronger technical operating support. As those facilities move from construction into steady operations, the Thailand integrated facility management (IFM) market gains a more durable stream of contracts tied to uptime, compliance, and asset performance rather than one-time support work.

Government Mandates on Commercial Buildings for Energy Efficiency Reshape FM Service Scope

Thailand's Building Energy Code, issued under ministerial regulation B.E. 2563 pursuant to the Energy Conservation Act B.E. 2535, applies energy-saving requirements to new or significantly modified buildings above 2,000 sq m and has been fully enforced since March 2023. The code covers six systems, including building envelope, lighting, air-conditioning, hot water, overall energy consumption, and renewable energy, which has widened the technical scope that owners now expect from FM partners. DEDE's Energy Efficiency Plan targets a 30% reduction in Thailand's energy intensity by 2037, and the building sector carries a 1,574-ktoe electricity demand reduction target within that plan. This changes procurement in the Thailand IFM market because energy auditing, BMS optimization, and performance reporting now sit closer to the center of contract design, especially for larger commercial assets. Bangkok Metropolitan Administration reinforced that direction in December 2025 through an energy conservation training program for 74 government officials under the Bangkok Energy Action Plan 2024-2030, extending operating scrutiny across public buildings in the capital. As a result, the Thailand integrated facility management market is seeing stronger demand for operators that can demonstrate measurable savings, documented procedures, and credible technical supervision in day-to-day building operations.

Skilled Labor Shortage in Technical FM Roles Constrains Hard FM Expansion

Thailand's labour challenge is structural, making it a deeper restraint on the Thailand IFM market than a short-term hiring cycle would suggest. The country's total fertility rate fell to 1.16 in 2023, it entered ageing-society status in the same year, and it is projected to become a super-ageing society by 2036. NESDC projects labour demand of 44.71 million by 2037 against a working-age population of 40.7 million, creating a gap likely to affect technical and mid-skilled roles most severely. The pressure is especially acute in MEP engineering, HVAC servicing, and BMS operations because these functions sit inside the fastest-growing parts of the Thailand integrated facility management market and cannot easily be filled with general labour. JLL noted that 40% of FM professionals in high-income countries are expected to retire by 2026 and that 56% of organizations plan to use predictive maintenance technologies, yet Thailand still faces weak digital readiness, with 74.1% of youth lacking foundational digital skills and only 5% of industries having adopted Industry 4.0 by 2024. Unless operators accelerate training and automation, the Thailand integrated facility management (IFM) market will continue to experience margin pressure, uneven service quality, and slower capacity build-out in technical accounts.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Special Economic Zones Broadens Market Reach Beyond Core Cities

- Mandatory ISO 41001 Adoption Elevates Contract Standards and Favors Certified Operators

- Fragmented Regulatory Oversight Creates Compliance Friction Across Portfolios

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management (FM) held 54.76% of the market in 2025, giving it the largest role in the Thailand integrated facility management (IFM) market and reflecting the broad installed base of commercial buildings, industrial estates, retail centers, and hospitality assets that need daily support. Cleaning, security, landscaping, and other support services remained central because they are required across asset classes and are easier to bundle into recurring contracts than specialized engineering work. Security services and cleaning or housekeeping were the two largest soft FM sub-segments, which explains why labour scale and route density still matter for winning high-volume accounts. Sodexo Amata Services, which serves more than 95 corporate clients in EEC industrial estates, demonstrates how multi-tenant parks convert routine service lines into long-running integrated mandates with steady renewal potential. Landscaping is also becoming more structured in premium projects because One Bangkok includes 108 rai of development area and 50 rai of managed green space, increasing coordination among grounds teams, common-area maintenance, and broader site operations.

Hard FM is the fastest-growing service type in the Thailand IFM market, with a 4.62% CAGR through 2031, as newer facilities require greater engineering oversight and faster response times. Thailand's data center service revenue is projected at THB 14.2 billion (USD 411.6 million), in 2026, up 9% from 2025, signalling a larger installed base of technically intensive sites that need constant monitoring and uptime support. These facilities require continuous MEP supervision, precision cooling control, and fire suppression compliance, making them difficult to serve with a low-skill staffing model. BOI approvals for 18 data center projects worth THB 389.14 billion (USD 11.3 billion), in H1 2025 suggest that the Thailand integrated facility management industry will continue shifting toward contracts with higher technical intensity and stronger 24/7 service expectations. As those assets move into full operation, hard FM will continue raising the quality threshold and renewal logic across the Thailand integrated facility management market.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Cushman and Wakefield plc

- PCS Security and Facility Services Limited

- ISS A/S

- Sodexo SA

- IFS Facility Services Co., Ltd.

- G4S Limited

- Guardforce Security (Thailand) Co., Ltd.

- Prompt Techno Service Co., Ltd.

- Metthier Co., Ltd.

- Global Facility Management Co., Ltd.

- STG Professional Co., Ltd.

- ASM Management Co., Ltd.

- Seacon Services Co., Ltd.

- THS Development Co., Ltd.

- AND Facility Management Co., Ltd.

- C.P. Property Management Co., Ltd.

- Siam Piwat Facilities Services Co., Ltd.

- GFM Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Investment in Eastern Economic Corridor Industry Parks

- 4.2.2 Government Mandates on Commercial Buildings for Energy Efficiency

- 4.2.3 Expansion of Special Economic Zones

- 4.2.4 Mandatory ISO 41001 Adoption in Public Sectors

- 4.2.5 Thailand Industrial Property Clustering and Industry City Development

- 4.2.6 Rising FDI-Driven Corporate Campus and Digital Infrastructure Investments

- 4.3 Market Restraints

- 4.3.1 Skilled Labor Shortage in Technical FM Roles

- 4.3.2 Fragmented Regulatory Oversight Across Multiple Agencies

- 4.3.3 High Competition from Price-Focused Staffing Outlets

- 4.3.4 Consolidation Gaps Between Traditional IFM Contracts and Legacy Facility Structures

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Cushman and Wakefield plc

- 6.4.4 PCS Security and Facility Services Limited

- 6.4.5 ISS A/S

- 6.4.6 Sodexo SA

- 6.4.7 IFS Facility Services Co., Ltd.

- 6.4.8 G4S Limited

- 6.4.9 Guardforce Security (Thailand) Co., Ltd.

- 6.4.10 Prompt Techno Service Co., Ltd.

- 6.4.11 Metthier Co., Ltd.

- 6.4.12 Global Facility Management Co., Ltd.

- 6.4.13 STG Professional Co., Ltd.

- 6.4.14 ASM Management Co., Ltd.

- 6.4.15 Seacon Services Co., Ltd.

- 6.4.16 THS Development Co., Ltd.

- 6.4.17 AND Facility Management Co., Ltd.

- 6.4.18 C.P. Property Management Co., Ltd.

- 6.4.19 Siam Piwat Facilities Services Co., Ltd.

- 6.4.20 GFM Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment