PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073167

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073167

United States Cross-Border E-Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

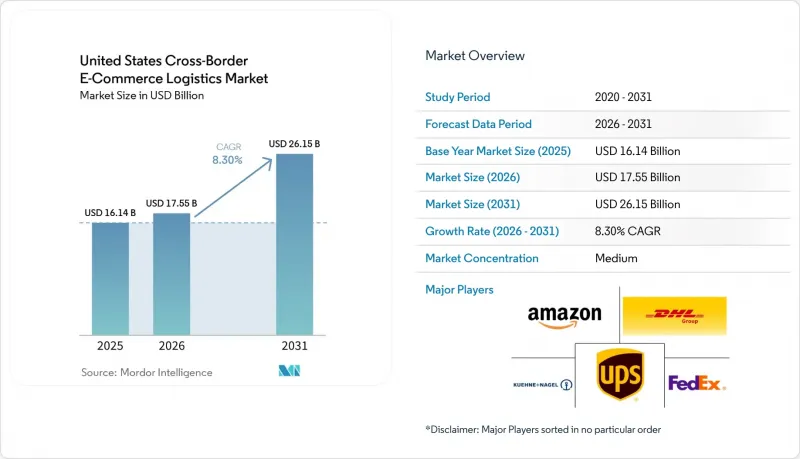

According to Mordor Intelligence, the united states cross-border e-commerce logistics market was valued at USD 16.14 billion in 2025 and is estimated to grow from USD 17.55 billion in 2026 to reach USD 26.15 billion by 2031, at a CAGR of 8.30% during the forecast period from 2026 to 2031.

This report is Segmented by Product Category (Foods, Personal and Household Care, and More), by Logistics Function (Transportation, Warehousing, and More), by Business Model (B2C, B2B, C2C), by Delivery Speed (Express, Standard), and by Flow Direction (Outbound/Inbound: Canada, Mexico, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

United States Cross-Border E-Commerce Logistics Market Trends and Insights

Marketplace-Led International Selling Expansion

Marketplace platforms are expanding access to overseas demand, giving the United States cross-border e-commerce logistics market a broader outbound base than it had when cross-border selling was limited to large merchants. Amazon opened Amazon Supply Chain Services on May 4, 2026, and made its freight, distribution, fulfillment, and parcel network available to businesses across industries, which marks one of the largest platform-led entries into the logistics stack tied to online commerce. Amazon said the network behind this offer includes more than 100 aircraft, more than 24,000 intermodal containers, and customs clearance capability, which means the platform is now competing more directly with established integrators and freight providers for cross-border flows. This matters for the United States cross-border e-commerce logistics market because customs, delivery, and fulfillment tools are moving closer to the point of sale, and merchants can add international channels without building a full internal trade compliance team. The result is that the United States cross-border e-commerce logistics market is capturing more export activity from brands that once treated foreign sales as too complex or too expensive to manage. It also reinforces the faster growth outlook for outbound flows, because marketplace-linked selling lowers the operational barrier between digital demand and physical shipment creation.

AI-Enabled Logistics Visibility and Customs Orchestration

AI tools are becoming more central to the United States' cross-border e-commerce logistics market because customs work, routing decisions, and disruption handling now require greater speed and consistency than manual processes can provide. Maersk launched Trade & Tariff Studio on June 25, 2025, and said the system applies AI across more than 6,000 product codes and 20,000 sub-codes with live input from more than 2,700 customs experts, which shows how classification and tariff analysis are moving into structured digital workflows. Maersk also stated that 20% of shipments are delayed by inadequate customs preparation, underscoring why merchants are placing greater value on providers that can reduce document errors before cargo reaches the border. project44 launched Autopilot on May 11, 2026, and said the platform processes more than 700 million logistics events daily across 259,000 carriers in 186 countries, with documented outcomes that included a 4% reduction in freight spend and up to 40% lower disruption-related costs. In the United States cross-border e-commerce logistics market, that kind of event visibility helps smaller merchants gain access to shipment intelligence that was once concentrated among larger enterprises. It also supports the growth of value-added services, because the commercial advantage is shifting from pure transport capacity toward better exception management, duty calculation, and customs readiness.

De Minimis Rollback and Tariff Stacking

The largest near-term restraint on the United States cross-border e-commerce logistics market is the rollback of de minimis treatment, because it changes the operating model for a very large parcel base. The White House stated that the suspension, effective August 29, 2025, removed duty-free treatment for low-value commercial shipments globally, which ended the main cost pathway that had supported direct parcel flows under the USD 800 threshold. The United States Customs and Border Protection said every e-commerce shipment still has to meet the applicable entry and compliance requirements, and the agency's guidance now places more weight on accurate classification, declared value, and entry processing than the prior low-friction parcel model did. The White House also noted that more than 1.36 billion de minimis shipments entered the United States in 2024, which shows the scale of the operational reset now being absorbed by merchants, carriers, and brokers. In the United States cross-border e-commerce logistics market, this does not remove demand, but it does raise the documentation, customs labor, and landed-cost burden tied to each parcel. It also strengthens the case for bonded warehousing, FTZ inventory positioning, and logistics networks capable of formal entry, because merchants now need more controlled ways to manage duty exposure and delivery certainty.

Other drivers and restraints analyzed in the detailed report include:

- USMCA-Enabled North American Corridor Optimization

- Delivery-Speed Visibility and Checkout Transparency Expectations

- Regulatory Complexity for Regulated and Battery-Linked Categories

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fashion and Lifestyle accounted for 23.65% of the United States cross-border e-commerce logistics market size in 2025, making it the largest revenue contributor. That lead came from a mix of high-frequency inbound apparel and accessories from Asian production hubs and outbound luxury and lifestyle shipments from US brands to buyers in Asia-Pacific and the Middle East. The segment remains strong because classification workflows, return handling, and parcel routing are already well established compared with more regulated product groups. In the United States cross-border e-commerce logistics market, fashion and lifestyle still benefit from repeat purchase behavior and a broad merchant base that ranges from global labels to smaller marketplace sellers. The maturity of the lane also means providers compete less on basic movement and more on delivery speed, prepaid duty options, and return control.

Personal and household Care is projected to grow at a 9.29% CAGR through 2031, which gives it the strongest momentum among product categories in the United States cross-border e-commerce logistics market. This part of the United States cross-border e-commerce logistics industry is benefiting from demand for specialty wellness items, prestige beauty products, and health-related goods that are not always easy to source through domestic channels alone. The shift suggests that future share gains will come from categories with higher value density and tighter handling needs rather than only from apparel volume. Consumer electronics and household appliances still account for meaningful inbound demand, but the battery rules on air shipments are increasing execution complexity for providers that serve those lanes. Foods and beverages and furniture remain part of the United States cross-border e-commerce logistics market, but their growth is held back by perishability on one side and dimensional weight economics on the other, which makes provider specialization more important than simple parcel scale.

Transportation accounted for 68.39% of the United States cross-border e-commerce logistics market share in 2025, reflecting the cost-weighted share of air, ocean, road, and rail movements across international lanes. This lead is especially visible on North American corridors, where road transport remains central to regional trade and rapid replenishment. The United States cross-border e-commerce logistics market still relies on transport capacity as its largest revenue pool, but the margin profile of the business is changing as compliance demands rise. Warehousing, distribution, and inventory management remain the next major functions because merchants need better control over landed cost timing, inventory release, and returns routing after the de minimis rollback. Bonded and FTZ facilities are becoming more relevant in the United States cross-border e-commerce logistics market because they allow duty deferral and more flexible release planning in a trade environment with higher documentation pressure.

Value-added services and others is projected to grow at a 13.48% CAGR through 2031, making it the fastest-expanding function in the United States cross-border e-commerce logistics market. That growth reflects rising demand for DDP management, customs brokerage, returns handling, classification support, and merchant-facing visibility tools rather than only more trucks or more aircraft. SEKO Logistics launched DutyPay in May 2025 to improve customs compliance and clearance execution, which shows how service providers are formalizing duty and entry workflows that used to be handled in a more fragmented way. Maersk and project44 have also expanded the technology layer around tariff and event management, which supports the move toward software-enabled value-added offerings inside the United States cross-border e-commerce logistics market. The result is a market where transportation still anchors revenue, but compliance intelligence and digital control are capturing a larger share of commercial value.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Flow Direction

- Outbound (Exports)

- Canada

- Mexico

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Inbound (Imports)

- Canada

- Mexico

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Outbound (Exports)

List of Companies Covered in this Report:

- United Parcel Service of America, Inc. (UPS)

- FedEx

- DHL Group

- Amazon, Inc.

- Pitney Bowes

- Kuehne+Nagel

- DSV A/S

- Expeditors International of Washington, Inc.

- CMA CGM Group (Including CEVA Logistics)

- GEODIS

- A.P. Moller - Maersk

- C.H. Robinson

- Nippon Express Holdings (NX Group)

- SEKO Logistics

- Flexport

- Global-e Online

- Asendia

- ShipBob

- ShipMonk

- Passport Shipping

- Easyship

- Zonos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Marketplace-Led International Selling Expansion

- 4.6.2 AI-Enabled Logistics Visibility and Customs Orchestration

- 4.6.3 USMCA-Enabled North American Corridor Optimization

- 4.6.4 Delivery-Speed Visibility and Checkout Transparency Expectations

- 4.6.5 DDP Checkout and Landed-Cost Visibility Adoption

- 4.6.6 Shift Toward US-Based Bonded and FTZ Inventory Positioning

- 4.7 Market Restraints

- 4.7.1 De Minimis Rollback and Tariff Stacking

- 4.7.2 Regulatory Complexity for Regulated and Battery-Linked Categories

- 4.7.3 UFLPA-Origin Traceability Burden on Low-Value Parcels

- 4.7.4 Duty-Paid Returns and Refused-Delivery Friction

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Flow Direction

- 5.5.1 Outbound (Exports)

- 5.5.1.1 Canada

- 5.5.1.2 Mexico

- 5.5.1.3 Europe

- 5.5.1.4 Asia-Pacific

- 5.5.1.5 Middle East and Africa

- 5.5.1.6 South America

- 5.5.2 Inbound (Imports)

- 5.5.2.1 Canada

- 5.5.2.2 Mexico

- 5.5.2.3 Europe

- 5.5.2.4 Asia-Pacific

- 5.5.2.5 Middle East and Africa

- 5.5.2.6 South America

- 5.5.1 Outbound (Exports)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service of America, Inc. (UPS)

- 6.4.2 FedEx

- 6.4.3 DHL Group

- 6.4.4 Amazon, Inc.

- 6.4.5 Pitney Bowes

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S

- 6.4.8 Expeditors International of Washington, Inc.

- 6.4.9 CMA CGM Group (Including CEVA Logistics)

- 6.4.10 GEODIS

- 6.4.11 A.P. Moller - Maersk

- 6.4.12 C.H. Robinson

- 6.4.13 Nippon Express Holdings (NX Group)

- 6.4.14 SEKO Logistics

- 6.4.15 Flexport

- 6.4.16 Global-e Online

- 6.4.17 Asendia

- 6.4.18 ShipBob

- 6.4.19 ShipMonk

- 6.4.20 Passport Shipping

- 6.4.21 Easyship

- 6.4.22 Zonos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment