PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073175

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073175

GCC Cross-Border E-Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

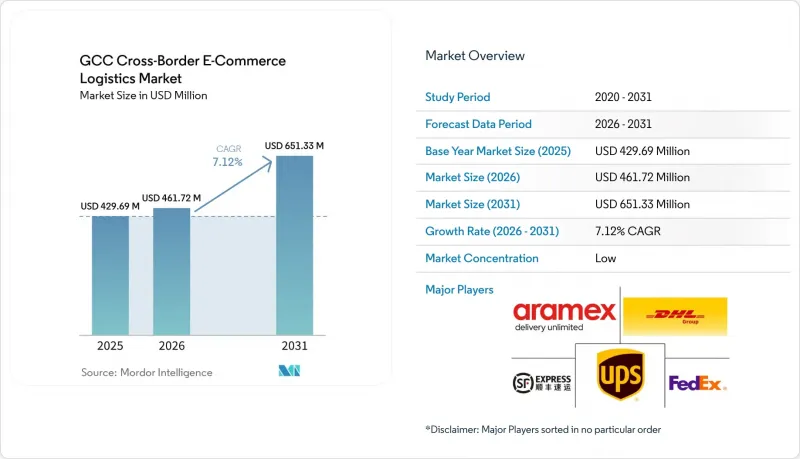

According to Mordor Intelligence, the GCC cross-border e-commerce logistics market size is expected to increase from USD 429.69 million in 2025 to USD 461.72 million in 2026 and reach USD 651.33 million by 2031, growing at a CAGR of 7.12% over 2026-2031.

The GCC cross-border e-commerce logistics market is expanding on the back of high digital adoption, strong consumer purchasing power, and the region's growing role as a gateway between Asian production centers and Gulf demand centers. This report is Segmented by Product Category (Fashion, Electronics, Personal and Household Care, Furniture, Other), by Logistics Function (Transportation, Warehousing, and More), by Business Model (B2C, B2B, C2C), Delivery Speed (Express, Standard), by Flow Direction (Inbound [North America, Europe, and More], Outbound [North America, Europe, and More]). The Market Forecasts are in Value (USD).

GCC Cross-Border E-Commerce Logistics Market Trends and Insights

Rising Demand for International Brands

Demand for imported brands remains one of the clearest growth supports for the GCC cross-border e-commerce logistics market. Consumers across the Gulf continue to spend heavily on foreign apparel, cosmetics, accessories, and electronics because domestic manufacturing depth in these categories remains limited. This pattern is pushing logistics contracts beyond basic parcel movement and toward premium handling, controlled packaging, and stronger return-management capabilities. It is also creating a broader role for operators to coordinate product compliance, especially for regulated goods that undergo import checks before release. As a result, the GCC cross-border e-commerce logistics market is earning a larger share of revenue from service complexity rather than from volume growth alone.

Double-Digit GCC E-Commerce Growth

Rapid online retail expansion continues to lift parcel volumes and support the GCC cross-border e-commerce logistics market. Seasonal demand peaks are becoming easier to forecast, which allows carriers and fulfillment operators to position inventory in advance rather than absorb demand shocks at the last minute. The growth in orders is also changing the freight mix because merchants are moving more regulated products, higher-value goods, and mixed-origin shipments that require different customs treatment. This makes customs support, bonded storage, and delivery coordination more important than simple line-haul capacity. The GCC cross-border e-commerce logistics market, therefore, benefits not only from rising order counts but also from rising handling intensity per shipment.

Customs and VAT Fragmentation

The GCC cross-border e-commerce logistics market still faces friction from uneven customs treatment and tax administration across the 6 states. Operators that serve several destination markets must manage different documentation rules, tax treatments, and release requirements even when the shipment enters through one regional gateway. This increases compliance costs and raises the value of integrated technology that can automate invoicing and multi-country tax handling. Larger carriers absorb this burden more effectively because they can spread compliance investment across broader parcel volumes. Smaller operators remain more exposed, which keeps the GCC cross-border e-commerce logistics market less efficient than a fully harmonized customs area would allow.

Other drivers and restraints analyzed in the detailed report include:

- Free Zones and Customs Digitization

- Faster-Delivery Expectations

- High Shipping and Reverse-Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fashion and lifestyle accounted for 37.41% of the GCC cross-border e-commerce logistics market size in 2025, making it the largest product category by value. This leadership reflects the region's young consumer base, strong preference for imported labels, and continued demand for apparel, footwear, and accessories sourced from Europe and Asia. In the GCC cross-border e-commerce logistics industry, fashion parcels require more than basic shipping, as packaging quality, returns handling, and rapid replenishment influence merchant performance. The category remains large, but it is also becoming more operationally demanding as international marketplaces and direct-from-origin sellers push higher order frequency into Gulf destinations.

Health and beauty / personal care is projected to grow at a 8.11% CAGR through 2031, making it the fastest-growing product category. Growth in this segment is supported by rising demand for imported skincare, wellness products, and premium personal care lines that are not always available through local retail channels. Compliance requirements are more stringent here because cosmetics and supplements often require additional registration and release management before final delivery. Consumer electronics and household appliances continue to carry some of the highest shipment values, which supports the use of air freight on time-sensitive corridors. Foods and beverages and furniture still account for a smaller share because food imports can face tighter restrictions, while furniture often carries an unfavorable volumetric cost profile for cross-border fulfillment.

Transportation held 73.33% of the GCC cross-border e-commerce logistics market share in 2025, confirming that line-haul movement still captures the majority of revenue in the current model. Air freight remains the leading transport mode within this segment because fashion, electronics, and premium consumer goods need shorter transit times from Asia and Europe into Gulf markets. Sea freight plays a role for heavier and lower-value goods where delivery time is less critical, while road transport remains essential for onward movement once parcels enter gateway markets. The GCC cross-border e-commerce logistics industry still depends heavily on transport capacity, but monetization is widening beyond pure movement.

Value-added services and others are forecast to grow at a 12.30% CAGR through 2031, which makes it the fastest-growing logistics function. This reflects growing merchant demand for bonded warehousing, returns handling, kitting, customs support, and localized buyer communication under a single logistics contract. Warehousing, distribution, and inventory management are also gaining importance as brands seek to place stock closer to Gulf consumers in order to shorten delivery windows. JD.com's logistics platform opened a warehouse in the UAE in 2025 and later announced a 70,000 m2 smart logistics hub with Abu Dhabi Airports, which signals continuing infrastructure investment around regional fulfillment depth. As these facilities scale, the GCC cross-border e-commerce logistics market should derive a larger share of revenue from warehousing and service integration rather than from transport alone.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Flow Direction

- Outbound (Exports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Inbound (Imports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Outbound (Exports)

List of Companies Covered in this Report:

- Aramex

- DHL Group

- FedEx

- United Parcel Service of America, Inc. (UPS)

- SF Express

- J&T Express

- JD Logistics

- A.P. Moller - Maersk

- Kuehne+Nagel

- CMA CGM Group (Including CEVA Logistics)

- DSV A/S

- DP World

- Emirates SkyCargo

- Qatar Airways Cargo

- AJEX Logistics Services

- iMile

- Shipa Delivery

- SMSA Express Transportation, Ltd.

- Asyad Express

- Amazon, Inc.

- Saudi Post (Including NAQEL Express)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising Demand for International Brands

- 4.6.2 Double-Digit GCC E-Commerce Growth

- 4.6.3 Free Zones and Customs Digitization

- 4.6.4 Faster-Delivery Expectations

- 4.6.5 Saudi National Address Enforcement

- 4.6.6 IOR and SOR Market-Entry Models

- 4.7 Market Restraints

- 4.7.1 Customs and VAT Fragmentation

- 4.7.2 High Shipping and Reverse-Logistics Costs

- 4.7.3 Product Registration Bottlenecks

- 4.7.4 DDU and COD Refusal Loops

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Flow Direction

- 5.5.1 Outbound (Exports)

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia-Pacific

- 5.5.1.4 Middle East and Africa

- 5.5.1.5 South America

- 5.5.2 Inbound (Imports)

- 5.5.2.1 North America

- 5.5.2.2 Europe

- 5.5.2.3 Asia-Pacific

- 5.5.2.4 Middle East and Africa

- 5.5.2.5 South America

- 5.5.1 Outbound (Exports)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Aramex

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 SF Express

- 6.4.6 J&T Express

- 6.4.7 JD Logistics

- 6.4.8 A.P. Moller - Maersk

- 6.4.9 Kuehne+Nagel

- 6.4.10 CMA CGM Group (Including CEVA Logistics)

- 6.4.11 DSV A/S

- 6.4.12 DP World

- 6.4.13 Emirates SkyCargo

- 6.4.14 Qatar Airways Cargo

- 6.4.15 AJEX Logistics Services

- 6.4.16 iMile

- 6.4.17 Shipa Delivery

- 6.4.18 SMSA Express Transportation, Ltd.

- 6.4.19 Asyad Express

- 6.4.20 Amazon, Inc.

- 6.4.21 Saudi Post (Including NAQEL Express)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment