PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073604

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073604

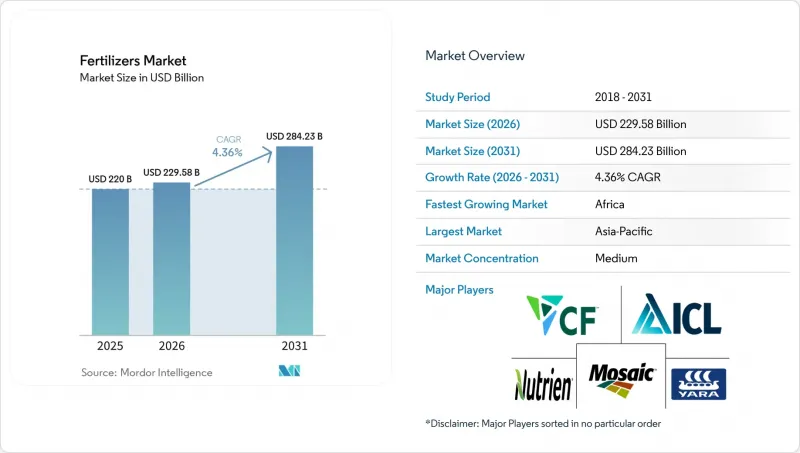

Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fertilizers market size is projected to expand from USD 220.00 billion in 2025 and USD 229.58 billion in 2026 to USD 284.23 billion by 2031, registering a CAGR of 4.36% between 2026 and 2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Fertilizers Market Trends and Insights

Surge in Fertilizer Demand from Precision-Agriculture Projects

Precision agriculture integrates global navigation satellite systems, soil sensors, and machine-learning algorithms to apply nutrients only where and when crops need them. This targeted approach reduces nitrogen use per bushel in United States corn trials, saving money and cutting nitrous oxide emissions. Adoption accelerates where farm consolidation and reliable connectivity support large machinery fleets fitted with variable-rate controllers. As equipment manufacturers embed agronomic software in sprayers and spreaders, growers seek controlled-release and liquid fertilizers that match site-specific prescriptions. The resulting pull effect spurs a steady rise in specialty nutrient demand across North America and Western Europe, with early signs of replication in China and Brazil. Evidence of payback within two seasons strengthens the investment case for smaller producers, widening the total addressable market for digital agronomy and nutrient combinations tailored to micro-zones.

Transition to Climate-Smart Nutrient-Management Policies

Governments embed nutrient stewardship in climate commitments because both fertilizer production and field emissions contribute significantly to agricultural greenhouse gas emissions. The European Union Farm to Fork Strategy targets a 20% cut in fertilizer use by 2030, while India promotes balanced fertilization under the National Mission for Sustainable Agriculture. Such mandates elevate demand for nitrification inhibitors, urease inhibitors, and polymer-coated urea that slow nutrient release and curb volatilization. China's guidelines require soil testing before fertilizer purchase, accelerating the shift from blanket doses to precision prescriptions. Producers capable of supplying enhanced-efficiency products gain pricing power, whereas commodity-grade volume faces downward pressure in regulated regions. Over the long term, harmonized carbon accounting may further differentiate suppliers on embedded emissions, reinforcing the strategic value of low-carbon nitrogen routes.

Growing Organic Farming Acreage

The expansion of organic farming acreage is substantially decreasing the demand for synthetic nitrogen-based fertilizers while increasing the demand for organic fertilizers, biofertilizers, and compost. As consumer preference for organic produce rises, certified farmland grows and prohibits synthetic nutrient inputs. The European Union Organic Action Plan (2021-2030) serves as a fundamental component of the Farm to Fork Strategy, aiming to achieve a target of at least 25% of agricultural land under organic farming by 2030. Organic agriculture is practiced in 188 countries, with over 96 million hectares of agricultural land managed organically by at least 4.5 million farmers as of 2024. Each converted hectare removes volume from the addressable market for chemical fertilizers, constituting a structural headwind that technology cannot offset. Although organic farms often yield less per hectare, their premium pricing sustains the acreage trend and dampens long-term demand in high-income regions.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Specialty and Slow-Release Formulations

- Artificial Intelligence Enabled Variable-Rate Application Platforms

- Scarcity of Water for Fertigation in Arid Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers remained the largest segment by type and accounted for 63.0% of the global fertilizers market share in 2025. This dominance is attributed to the continued reliance of crop production systems on separate applications of nitrogen, phosphorus, and potassium nutrients. Within this segment, nitrogen fertilizers accounted for the largest volume, with products such as urea, anhydrous ammonia, and ammonium nitrate driving demand across major agricultural regions. According to the International Fertilizer Association, global urea production reached 201 million metric tons in 2024, up 3% compared to 2023. China's urea output is projected to reach 76.5 million metric tons by 2026 as new production capacities become operational. Phosphatic fertilizers, including diammonium phosphate, monoammonium phosphate, single superphosphate, and triple superphosphate, remained critical for crop establishment despite higher procurement costs. Potassic fertilizers, led by muriate of potash, continued to experience stable demand, supported by expanding production capacities. Additionally, the segment encompasses secondary nutrients and micronutrients, with zinc holding the largest share among micronutrients, and boron witnessing increased adoption in intensively cultivated farming systems.

Complex fertilizers are anticipated to be the fastest-growing segment by type, with a projected CAGR of 5.8% from 2026 to 2031, surpassing the overall market growth rate. These fertilizers combine multiple nutrients into a single formulation, promoting balanced crop nutrition while simplifying application processes and reducing labor requirements. Adoption is particularly increasing in horticultural, plantation, and other high-value crop systems where nutrient efficiency is crucial for productivity. In Europe, nutrient reduction targets and sustainability initiatives are driving the use of nutrient-dense formulations that enhance nutrient-use efficiency while lowering application volumes. Furthermore, the growing adoption of precision agriculture technologies, variable-rate application systems, and soil-specific nutrient management practices is bolstering demand for balanced fertilizer products. As growers focus on maximizing yields and improving fertilizer efficiency, complex fertilizers are emerging as a preferred alternative to standalone nutrient products, supporting consistent growth throughout the forecast period.

Conventional fertilizers are the largest form and account for 88.5% of the fertilizers market size in 2025, yet growers in regulated regions are gradually shifting to enhanced-efficiency forms that meet environmental targets without sacrificing yield. These products, generally uncoated granules or prills, are applied using broadcast spreaders or incorporated into the soil during tillage. Nutrient availability depends on factors such as soil moisture, temperature, and microbial activity. Their low production cost and compatibility with existing farming equipment support their continued prevalence in price-sensitive markets, including cereals, oilseeds, and sugarcane. Conventional products are increasingly challenged by regulatory restrictions on application rates and by environmental concerns about nutrient runoff. This has led to a gradual shift toward enhanced-efficiency alternatives, even in cost-sensitive segments.

Specialty fertilizers are projected to grow at a CAGR of 6.3% during the period 2026-2031. This growth is driven by the adoption of controlled-release, slow-release, liquid, and water-soluble formulations, which enhance nutrient-use efficiency and reduce labor requirements. Controlled-release fertilizers, coated with polymers or sulfur, release nutrients based on soil temperature and moisture, aligning nutrient availability with crop demand and reducing leaching losses by 20% to 40% compared to conventional fertilizers. Slow-release fertilizers, formulated with chemicals such as urea-formaldehyde or isobutylidene diurea, provide a cost-effective option with extended nutrient release, making them suitable for turfgrass and ornamental applications. Liquid fertilizers are witnessing significant growth in North America and Europe, where large farms incorporate them into existing sprayer systems for foliar or starter applications, ensuring uniform coverage and rapid nutrient uptake by plants.

Complete Report Scope:

- By Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Ammonium Nitrate

- Anhydrous Ammonia

- Urea

- Others

- Phosphatic

- Di-ammonium Phosphate (DAP)

- Mono Ammonium Phosphate (MAP)

- Single Super Phosphate (SSP)

- Triple Superphosphate (TSP)

- Others

- Potassic

- Muriate of Potash (MoP)

- Sulphate of Potash (SoP)

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- By Form

- Conventional

- Specialty

- Controlled-Release Fertilizer (CRF)

- Liquid Fertilizer

- Slow-Release Fertilizer (SRF)

- Water Soluble

- By Application Mode

- Fertigation

- Foliar

- Soil

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Geography

- North America

- Canada

- Mexico

- United States

- Rest of North America

- Europe

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Ukraine

- United Kingdom

- Rest of Europe

- Asia-Pacific

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

- South America

- Argentina

- Brazil

- Rest of South America

- Middle East

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific is the largest geography segment, accounting for 52.3% of the fertilizers market share in 2025, led by China and India. China's domestic urea production capacity exceeded 80.45 million metric tons in 2024, ensuring a stable supply. However, older coal-based facilities may face stricter emissions regulations, potentially leading to idled operations and creating opportunities for coastal gas-based plants equipped with carbon capture technology. In India, the Ministry of Agriculture reported that total annual fertilizer consumption for 2023-24 was approximately 60.1 million metric tons. Of this, 50.3 million metric tons were produced domestically, while 17.7 million metric tons were imported. In Southeast Asia, demand is driven by palm oil, rice, and rubber plantations. Additionally, Indonesian refiners are testing controlled-release fertilizer blends in large rice paddies to meet sustainability certification requirements.

Africa is projected to record the fastest compound annual growth rate (CAGR) of 6.2% through 2031. Fertilizer demand in Sub-Saharan Africa is shaped by agricultural modernization, population growth, and government efforts to achieve food self-sufficiency. Fertilizer application rates in the region are considerably lower than global averages, indicating significant growth potential as infrastructure improves and affordability challenges are addressed. Nigeria and South Africa, the region's largest economies, are focusing on increasing domestic production capacities to reduce reliance on imports and stabilize prices. Additionally, Ethiopia, Kenya, and Tanzania are expanding blending facilities that import bulk urea and diammonium phosphate (DAP) to create customized NPK ratios tailored to local crops such as coffee, tea, and maize. In the Middle East, countries like Saudi Arabia, the United Arab Emirates, and Turkey combine domestic production capabilities with imports to meet fertilizer demand, as arid climates and limited arable land restrict agricultural growth. Turkey's strategic location positions it as a logistics hub for fertilizer trade across Europe, Asia, and Africa.

Europe confronts stringent nutrient caps and elevated energy costs that curb straight-fertilizer volumes but boost specialty margins. Eastern European markets, particularly Ukraine and Russia, remain key exporters of urea, ammonium nitrate, and potash. However, geopolitical instability and export restrictions have disrupted trade flows, redirecting volumes toward Asia and Africa. In the United Kingdom, post-Brexit agricultural policy focuses on environmental land management, with subsidies transitioning from production support to ecosystem services. This shift has placed additional pressure on conventional fertilizer demand while creating opportunities for organic and biostimulant products. Crop producers in France and Spain invest in precision-spreaders to comply with nitrogen limits without depressing grain output, reinforcing demand for inhibitor-coated products.

- Nutrien Ltd.

- Uralkali PJSC (Uralchem Group)

- The Mosaic Company

- K+S Aktiengesellschaft

- ICL Group Ltd.

- EuroChem Group AG

- CF Industries Holdings, Inc.

- OCP S.A.

- PhosAgro PJSC

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- Haifa Chemicals Ltd.

- Yara International ASA

- Koch Fertilizer, LLC

- Grupa Azoty S.A. (Compo Expert)

- BHP Group Limited

- Qinghai Salt Lake Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in fertilizer demand from precision-agriculture projects

- 4.6.2 Transition to climate-smart nutrient-management policies

- 4.6.3 Rapid adoption of specialty and slow-release formulations

- 4.6.4 Capacity expansions in low-cost natural-gas regions

- 4.6.5 Carbon-credit incentives for green ammonia production

- 4.6.6 Artificial intelligence enabled variable-rate application platforms

- 4.7 Market Restraints

- 4.7.1 Volatile feedstock prices

- 4.7.2 Regulatory caps on nitrogen usage in Europe

- 4.7.3 Growing organic farming acreage

- 4.7.4 Scarcity of water for fertigation in arid regions

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 Di-ammonium Phosphate (DAP)

- 5.1.2.3.2 Mono Ammonium Phosphate (MAP)

- 5.1.2.3.3 Single Super Phosphate (SSP)

- 5.1.2.3.4 Triple Superphosphate (TSP)

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 Muriate of Potash (MoP)

- 5.1.2.4.2 Sulphate of Potash (SoP)

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 By Form

- 5.2.1 Conventional

- 5.2.2 Specialty

- 5.2.2.1 Controlled-Release Fertilizer (CRF)

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 Slow-Release Fertilizer (SRF)

- 5.2.2.4 Water Soluble

- 5.3 By Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 By Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 Mexico

- 5.5.1.3 United States

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 France

- 5.5.2.2 Germany

- 5.5.2.3 Italy

- 5.5.2.4 Netherlands

- 5.5.2.5 Russia

- 5.5.2.6 Spain

- 5.5.2.7 Ukraine

- 5.5.2.8 United Kingdom

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 Australia

- 5.5.3.2 Bangladesh

- 5.5.3.3 China

- 5.5.3.4 India

- 5.5.3.5 Indonesia

- 5.5.3.6 Japan

- 5.5.3.7 Pakistan

- 5.5.3.8 Philippines

- 5.5.3.9 Thailand

- 5.5.3.10 Vietnam

- 5.5.3.11 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Argentina

- 5.5.4.2 Brazil

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Nutrien Ltd.

- 6.4.2 Uralkali PJSC (Uralchem Group)

- 6.4.3 The Mosaic Company

- 6.4.4 K+S Aktiengesellschaft

- 6.4.5 ICL Group Ltd.

- 6.4.6 EuroChem Group AG

- 6.4.7 CF Industries Holdings, Inc.

- 6.4.8 OCP S.A.

- 6.4.9 PhosAgro PJSC

- 6.4.10 Coromandel International Limited

- 6.4.11 Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- 6.4.12 Haifa Chemicals Ltd.

- 6.4.13 Yara International ASA

- 6.4.14 Koch Fertilizer, LLC

- 6.4.15 Grupa Azoty S.A. (Compo Expert)

- 6.4.16 BHP Group Limited

- 6.4.17 Qinghai Salt Lake Industry Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS