PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073615

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073615

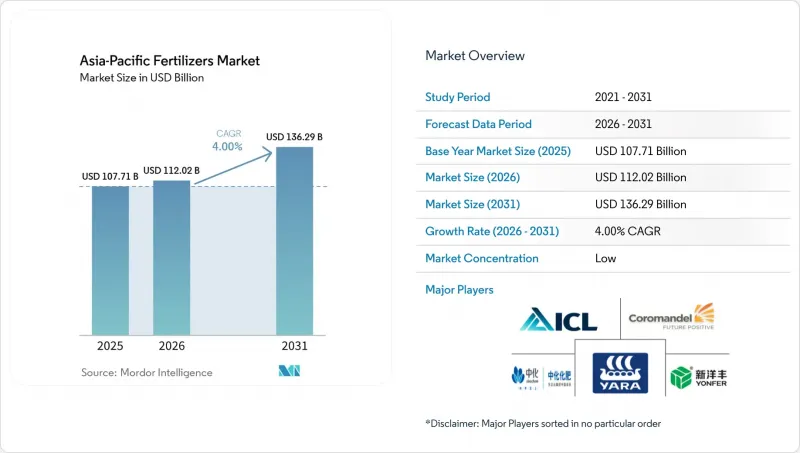

Asia-Pacific Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific fertilizers market size is projected to grow from USD 107.71 billion in 2025 to USD 112.02 billion in 2026 and is forecast to reach USD 136.29 billion by 2031, registering a CAGR of 4.0% during the forecast period (2026-2031).

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Geography (Australia, Bangladesh, China, India, Indonesia, Japan, Pakistan, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Fertilizers Market Trends and Insights

Subsidy rationalization in India and China is shifting demand toward balanced fertilization

India's Nutrient-Based Subsidy framework and China's parallel reforms narrow the cost gap between urea and complex fertilizers, steering growers toward balanced NPK blends and specialty micronutrients. The converging policies underpin stronger demand for high-analysis products that improve soil fertility while moderating nitrogen overuse. Established producers with diversified portfolios gain pricing power, whereas commodity urea suppliers confront shrinking margins. Supply-chain complexity increases as companies must align formulation registration and distribution systems with evolving sub-national subsidy codes. The shift strengthens the premium tier of the Asia-Pacific fertilizers market.

Government-funded soil health card initiatives are improving micronutrient adoption

More than 220 million soil health cards distributed in India reveal zinc, boron, and iron deficiencies across key cereal belts, galvanizing targeted micronutrient fertilizer uptake. Data-driven prescriptions encourage growers to adopt custom blends that command price premiums yet deliver measurable yield gains. Manufacturers respond with crop- and region-specific micronutrient packs while investing in agronomy advisory teams that translate analytical results into precise usage guidelines. Similar initiatives in Bangladesh and Pakistan position South Asia as a long-run growth engine for the Asia-Pacific fertilizers market.

Volatile ammonia and phosphate feedstock prices are squeezing producer margins

Yara projects natural gas cost increases of USD 85 million for Q1 2025 and USD 225 million for Q2 2025, underscoring susceptibility to energy price swings that compress gross margins. Smaller Asian producers reliant on imported ammonia or phosphate rock face pronounced cost pass-through risks, occasionally curtailing operating rates during spike episodes. Extended price turbulence complicates growers' budgeting cycles and may delay the adoption of premium fertilizers within the Asia-Pacific fertilizers market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in specialty fertilizer capacity expansions across Southeast Asia

- Rising horticulture exports from Vietnam and Thailand propelling water-soluble demand

- Stringent Chinese export quotas limiting regional supply security

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers accounted for 59.0% of the Asia-Pacific fertilizers market share in 2025, driven by the prevalent use of separate nitrogen, phosphorus, and potassium applications in major crop production systems. Nitrogenous fertilizers, particularly urea with its 46% nitrogen content, continue to lead demand due to their cost-effectiveness and widespread use in China and India. Phosphatic and potassic fertilizers remain critical for enhancing crop productivity, while increasing awareness of soil nutrient deficiencies is encouraging the adoption of micronutrients such as zinc.

Complex fertilizers are anticipated to be the fastest-growing segment, with a projected CAGR of 5.4% from 2026 to 2031. This growth is attributed to rising demand for balanced nutrient formulations that enhance nutrient-use efficiency and simplify fertilizer application processes. Government initiatives, such as India's USD 4.8 billion nutrient-based subsidy scheme for 2026 and measures to ensure fertilizer availability in China, are further promoting adoption across the region. Additionally, the expansion of precision farming practices is projected to drive demand for complex fertilizers throughout the forecast period.

Conventional fertilizers accounted for 72.0% of revenue in 2025, while specialty fertilizers are projected to expand at a CAGR of 7.1% through 20231 as growers and regulators increasingly prioritize nutrient-use efficiency. Water-soluble products top the growth leaderboard, encouraged by widespread fertigation rollouts in horticulture zones. Controlled-release fertilizers gain share as labor scarcity and leaching losses push demand for single-shot applications, though scrutiny of polymer microplastics is intensifying.

ICL's USD 170 million distribution pact with AMP Holdings underscores commercial confidence in specialty water-soluble offerings for premium fruit and vegetable crops. Liquid fertilizers ride the mechanization trend, especially in greenhouse and plantation settings, adding further momentum to the specialty segment within the Asia-Pacific fertilizers market.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Ammonium Nitrate

- Anhydrous Ammonia

- Urea

- Others

- Phosphatic

- DAP

- MAP

- SSP

- TSP

- Others

- Potassic

- MoP

- SoP

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Country

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Coromandel International Ltd.

- Grupa Azoty S.A. (Compo Expert)

- Haifa Group

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- ICL Group Ltd

- Sinofert Holdings Limited

- Sociedad Quimica y Minera de Chile SA

- Xinyangfeng Agricultural Technology Co., Ltd.

- Yara International ASA

- Zhongchuang xingyuan chemical technology co.ltd

- Koch Agronomic Services, LLC

- Nutrien Ltd.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Florikan ESA LLC

- Kingenta Ecological Engineering Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Subsidy rationalization in India and China shifting demand toward balanced fertilization

- 4.6.2 Government-funded soil health card initiatives improving micronutrient adoption

- 4.6.3 Surge in specialty fertilizer capacity expansions across Southeast Asia

- 4.6.4 Rising horticulture exports from Vietnam and Thailand propelling water-soluble demand

- 4.6.5 Carbon-credit monetization pilot projects rewarding low-emission fertilizers

- 4.6.6 Coastal aquaculture nutrient-leakage restrictions driving sulfur-coated products

- 4.7 Market Restraints

- 4.7.1 Volatile ammonia and phosphate feedstock prices squeezing producer margins

- 4.7.2 Stringent Chinese export quotas limiting regional supply security

- 4.7.3 Proliferation of counterfeit fertilizer bags in South Asia eroding brand trust

- 4.7.4 Growing micro-plastic scrutiny on polymer-coated CRFs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

- 5.5 Country

- 5.5.1 Australia

- 5.5.2 Bangladesh

- 5.5.3 China

- 5.5.4 India

- 5.5.5 Indonesia

- 5.5.6 Japan

- 5.5.7 Pakistan

- 5.5.8 Philippines

- 5.5.9 Thailand

- 5.5.10 Vietnam

- 5.5.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 ICL Group Ltd

- 6.4.6 Sinofert Holdings Limited

- 6.4.7 Sociedad Quimica y Minera de Chile SA

- 6.4.8 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.9 Yara International ASA

- 6.4.10 Zhongchuang xingyuan chemical technology co.ltd

- 6.4.11 Koch Agronomic Services, LLC

- 6.4.12 Nutrien Ltd.

- 6.4.13 Shandong Hualu-Hengsheng Chemical Co., Ltd.

- 6.4.14 Florikan ESA LLC

- 6.4.15 Kingenta Ecological Engineering Group Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOs