PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073618

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073618

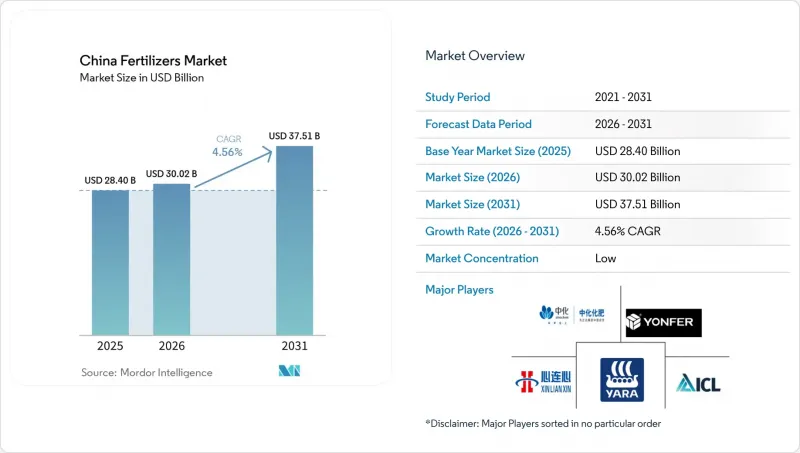

China Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china fertilizer market size is projected to grow from USD 28.40 billion in 2025 to USD 30.02 billion in 2026 and is forecast to reach USD 37.51 billion by 2031 at 4.56% CAGR over 2026-2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

China Fertilizers Market Trends and Insights

Government Fertilizer-Use Subsidy Schemes

Direct government subsidies for balanced fertilization and soil restoration under the Ministry of Agriculture and Rural Affairs programs are accelerating nutrient demand across China's agricultural regions. The agricultural machinery purchase subsidy program expanded to include precision fertilizer application equipment, with subsidy rates reaching 30% for eligible farmers in 2024. These policy interventions create artificial demand elasticity that supports premium pricing for efficiency-enhancing products while simultaneously driving volume growth in targeted nutrient categories. The subsidy framework particularly benefits controlled-release and water-soluble fertilizers that demonstrate measurable efficiency gains over conventional alternatives. Policy implementation varies significantly across provinces, with major grain-producing regions receiving proportionally higher subsidy allocations that distort regional competitive dynamics.

Chronic Pressure to Raise Crop Yields and Quality

Food security mandates embedded in China's national agricultural strategy create persistent upward pressure on fertilizer application intensity across all crop categories. The State Council's diversified food supply system opinion emphasizes yield maximization per hectare to offset limited arable land expansion, directly translating to increased nutrient input requirements. This policy framework operates independently of market pricing signals, creating inelastic demand for fertilizer products even during periods of agricultural commodity price volatility. Regional implementation focuses on closing yield gaps between average and potential productivity, with particular emphasis on grain crops that underpin national food security objectives. The pressure intensifies in regions where urbanization reduces agricultural land availability, forcing remaining farmland to achieve higher productivity levels through intensive fertilization practices.

Stricter Nutrient-Loss Regulations and Inspection Regimes

New GB 15618 soil quality standards impose penalties for excess nitrate leaching and phosphorus runoff, creating compliance costs that constrain fertilizer application rates across environmentally sensitive agricultural regions. The Ministry of Ecology and Environment has strengthened inspection protocols with real-time monitoring systems that track nutrient loading in watershed areas, forcing farmers to reduce application rates or face significant financial penalties . These regulatory constraints operate independently of agronomic optimization, creating situations where yield-maximizing fertilizer rates exceed legally permissible application levels. Compliance requirements favor efficiency-enhanced products that deliver equivalent nutritional value at lower application rates, but the transition period creates market disruption as farmers adjust application practices.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Specialty Fertilizer Consumption

- Expansion of Protected Cultivation Acreage Needing Fertigation

- Plateauing Macronutrient Demand in Major Grain Belts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Complex fertilizers are the largest segment, holding 56.2% of the China fertilizer market share in 2025, and are projected to register the fastest 6.0% CAGR through 2031. The complex segment benefits from precision agriculture trends that favor customized nutrient ratios matched to specific crop requirements and soil conditions. NPK compound fertilizers dominate the complex category, supported by established agronomic protocols that specify balanced nutrient ratios for major crop categories. Specialty complex formulations incorporating micronutrients and secondary macronutrients command premium pricing while addressing specific nutritional deficiencies identified through soil testing programs.

The segment's prominence is primarily attributed to its ability to provide multiple nutrients in a single application, making it highly efficient for farmers. Complex fertilizers are particularly crucial in China's urban greening sector, playing a vital role in maintaining decorative trees, high-quality grass, and nurturing flowers in greenhouses. The segment's strength is further reinforced by China's increasing reliance on NPK fertilizers, which typically account for about half of total fertilizer consumption. The granulation production method stands as the primary manufacturing approach, reflecting China's sophisticated fertilizer production landscape.

Conventional products accounted for 74.0% of revenue in 2025, supported by established manufacturing infrastructure and cost advantages that align with price-sensitive agricultural markets. The conventional segment encompasses traditional granular and crystalline formulations that deliver nutrients reliably through proven application methods and equipment compatibility. Bulk handling advantages in conventional products support efficient distribution systems that serve large-scale agricultural operations with minimal logistical complexity. Manufacturing scale economies in conventional fertilizer production create cost structures that maintain competitive advantages over specialty alternatives in price-sensitive market segments.

Specialty variants are forecast to expand at the fastest pace of 6.1% CAGR through 2031. This segment is experiencing rapid advancement due to the increasing adoption of precision agriculture and modern irrigation methods. Water-soluble fertilizers, which account for about half of the specialty segment, are gaining particular traction due to their superior nutrient-delivery efficiency. The segment's growth is further propelled by rising awareness among farmers about the benefits of controlled-release fertilizers and their role in sustainable agriculture. The Chinese government's emphasis on environmental protection and the need for improved fertilizer efficiency are driving innovation in specialty fertilizer formulations.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Urea

- Others

- Phosphatic

- DAP

- MAP

- SSP

- TSP

- Potassic

- MoP

- SoP

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Sinofert Holdings Limited

- Xinyangfeng Agricultural Technology Co., Ltd.

- Henan XinlianXin Chemicals Group Company Limited

- Yara International ASA

- ICL Group Ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM S.A.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Florikan ESA LLC

- National Fertilizers Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY & KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Primary Nutrients

- 4.3.1 Field Crops

- 4.3.2 Horticultural Crops

- 4.4 Secondary Macronutrients

- 4.4.1 Field Crops

- 4.4.2 Horticultural Crops

- 4.5 Agricultural Land Equipped For Irrigation

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

- 4.8 Market Drivers

- 4.8.1 Government fertilizer?use subsidy schemes

- 4.8.2 Chronic pressure to raise crop yields and quality

- 4.8.3 Surge in specialty fertilizer consumption

- 4.8.4 Expansion of protected cultivation acreage needing fertigation

- 4.8.5 Emergence of digital agriculture platforms enabling precision dosing

- 4.8.6 Early adoption of low-carbon green ammonia production lines

- 4.9 Market Restraints

- 4.9.1 Stricter nutrient-loss regulations and inspection regimes

- 4.9.2 Plateauing macronutrient demand in major grain belts

- 4.9.3 Soil-test service bundles shifting farmers away from blanket NPK

- 4.9.4 Carbon-pricing pilots boosting production costs for high-emission plants

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Sinofert Holdings Limited

- 6.4.2 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.3 Henan XinlianXin Chemicals Group Company Limited

- 6.4.4 Yara International ASA

- 6.4.5 ICL Group Ltd

- 6.4.6 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.7 Compo Expert GmbH

- 6.4.8 Haifa Chemicals Ltd.

- 6.4.9 Nutrien Ltd.

- 6.4.10 Yara International ASA

- 6.4.11 Koch Agronomic Services, LLC

- 6.4.12 SQM S.A.

- 6.4.13 Shandong Hualu-Hengsheng Chemical Co., Ltd.

- 6.4.14 Florikan ESA LLC

- 6.4.15 National Fertilizers Limited

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS