PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073619

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073619

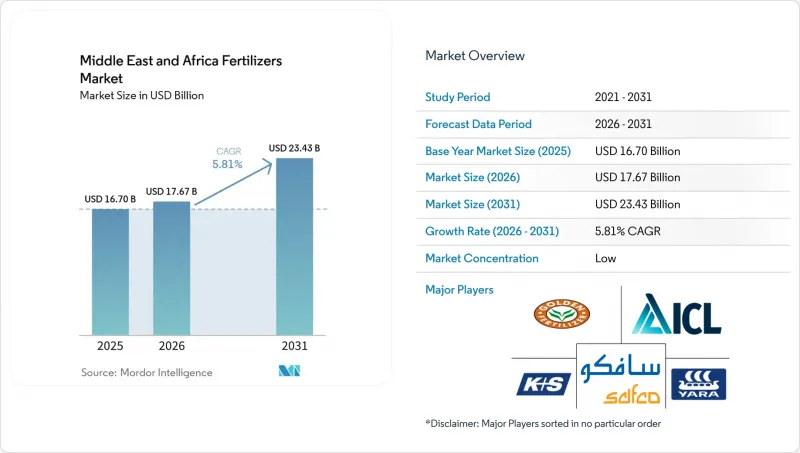

Middle East and Africa Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and Africa fertilizers market size was valued at USD 16.70 billion in 2025 and estimated to grow from USD 17.67 billion in 2026 to reach USD 23.43 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031).

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and More), by Crop Type (Field Crops, Horticultural Crops, and Soil), and by Geography (Nigeria, Saudi Arabia, South Africa, Turkey, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East and Africa Fertilizers Market Trends and Insights

Rising Regional Food Security Initiatives

Middle East and African governments are tying fertilizer self-sufficiency directly to food sovereignty. Saudi Arabia earmarked USD 1.2 billion for import-substitution projects in 2024, targeting integrated ammonia and urea complexes that reduce external dependence. Nigeria's Presidential Fertilizer Initiative set a goal to trim fertilizer imports by 50% by 2027, leveraging new capacity at Dangote facilities. Ethiopia partnered with a private investor to build a USD 2.5 billion urea plant that will tap domestic gas reserves, bringing 3 million metric tons annual line online within 40 months. Sub-Saharan Africa currently imports roughly 80% of its fertilizer, so each new plant sends a positive signal to lenders and multinational equipment suppliers. These projects also catalyze ancillary investments in gas pipelines, rail spurs, and bulk terminals that knit the regional supply chain together.

Expansion of Government Fertilizer Subsidy Programs

National treasuries view subsidies as a fast-acting lever to stabilize input costs and rural incomes. Egypt raised its subsidy pool by 35% in 2024, cutting farmer urea prices to USD 180 per metric ton against international quotes above USD 350 per metric ton. Kenya's program reached 1.2 million smallholders, slashing input costs by up to 50% through mobile vouchers that link soil-test prescriptions to verified dealer outlets. Nigeria distributed 12 million bags of subsidized NPK blends in 2024 and combined the roll-out with e-wallet payments that curb leakages. Saudi Arabia covers 75% of the landed cost of micronutrient packages for date-palm growers, prompting a surge in precision nutrition adoption on arid plots. Predictable offtake allows blenders to lock in feedstock contracts and plan inventory turns in advance.

Volatile Natural Gas Linked Ammonia Prices

Energy represents roughly three-quarters of ammonia production cost, so swings in gas prices ripple straight into urea quotations. The European Union shuttered up to 70% of its capacity at the height of the 2022 gas spike, forcing African buyers to absorb freight premiums and longer lead times. Kenya experienced retail fertilizer prices that climbed 150% between 2020 and 2022, denting staple-crop yields among the smallholders who supply most domestic food. Importers now diversify suppliers and use longer-tenor gas contracts, yet risk remains elevated whenever benchmark gas trade tightens.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Specialty and Slow-Release Fertilizers

- Rising Investments in Modern Irrigation Systems

- Persistent Logistical Bottlenecks at Key Red Sea Ports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight formulations accounted for 57.9% of the Middle East and Africa fertilizers market share in 2025. Government programs tend to subsidize basic NPK components, making single-nutrient grades the default choice among smallholders. Urea leads nitrogen sales for cereal production systems, whereas DAP and MAP remain the principal phosphatic products. The Middle East and Africa fertilizers market size for straight grades benefits from standardized distribution and storage systems that favor bulk handling.

Complex fertilizers are projected to be the fastest-growing segment, with a CAGR of 7.2% through 2026 to 2031. They play a crucial role in horticulture, irrigated cash crops, and export-oriented farms that demand precise nutrient ratios. Morocco's capacity expansion under the SP2M plan will lift blended output across North Africa, offering site-specific formulations that pair macronutrients with micronutrient packages. Uptake is strongest where soil-testing mandates exist, such as in South Africa, or where lenders tie credit to agronomic prescriptions.

Conventional granules captured 83.5% share of the Middle East and Africa fertilizers market in 2025. Broad familiarity, robust supply chains, and equipment compatibility underpin their dominance. Producers are investing in energy-saving revamps, such as Egypt's Abu Qir natural gas efficiency upgrade, to keep cost curves competitive.

Specialty fertilizers, grades of controlled-release fertilizers, water-soluble fertilizers, and foliar liquids occupy a small yet fast-rising niche, projected to grow at a CAGR of 9.3% during 2026-2031. Drip-irrigated acreage expansion in Gulf greenhouses and the spread of hydroponics in Turkish horticulture fuel demand for fully soluble products. Slow-release coatings appeal to remote growers with limited labor, reducing application frequency and nutrient loss in sandy soils.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Ammonium Nitrate

- Urea

- Others

- Phosphatic

- Diammonium Phosphate (DAP)

- Monoammonium Phosphate (MAP)

- Single Super Phosphate (SSP)

- Triple Super Phosphate (TSP)

- Others

- Potassic

- Muriate of Potash (MoP)

- Sulfate of Potash (SoP)

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Specialty

- Controlled Release Fertilizer (CRF)

- Liquid Fertilizer

- Slow Release Fertilizer (SRF)

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Geography

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

List of Companies Covered in this Report:

- Yara International ASA

- SABIC Agri-Nutrients Company (Saudi Basic Industries Corporation)

- OCP Group

- Ma'aden Phosphate Company (Saudi Arabian Mining Company - Ma'aden)

- Qatar Fertiliser Company QAFCO (Industries Qatar)

- ICL Group Ltd

- K+S Aktiengesellschaft

- EuroChem Group AG

- PhosAgro PJSC

- Fertiglobe PLC (OCI N.V.)

- Omnia Fertilizer (Pty) Ltd (Omnia Holdings Ltd)

- Dangote Fertilizer Ltd (Dangote Industries Ltd)

- Indorama Eleme Fertilizer and Chemicals Ltd (Indorama Corporation)

- Haifa Group

- Jordan Phosphate Mines Company PLC

- Golden Fertilizer Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising regional food security initiatives

- 4.6.2 Expansion of government fertilizer subsidy programs

- 4.6.3 Increasing adoption of specialty and slow-release fertilizers

- 4.6.4 Rising investments in modern irrigation systems

- 4.6.5 Shift toward sulfur-enriched blends for oil-seed crop rotations

- 4.6.6 Growing use of desalinated water driving demand for micronutrients

- 4.7 Market Restraints

- 4.7.1 Volatile natural gas linked ammonia prices

- 4.7.2 Persistent logistical bottlenecks at key Red Sea ports

- 4.7.3 Regulatory pushback on cadmium levels in imported phosphates

- 4.7.4 Rising farmer preference for biologicals in high-value crops

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Urea

- 5.1.2.2.3 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 Diammonium Phosphate (DAP)

- 5.1.2.3.2 Monoammonium Phosphate (MAP)

- 5.1.2.3.3 Single Super Phosphate (SSP)

- 5.1.2.3.4 Triple Super Phosphate (TSP)

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 Muriate of Potash (MoP)

- 5.1.2.4.2 Sulfate of Potash (SoP)

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Specialty

- 5.2.2.1 Controlled Release Fertilizer (CRF)

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 Slow Release Fertilizer (SRF)

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

- 5.5 Geography

- 5.5.1 Nigeria

- 5.5.2 Saudi Arabia

- 5.5.3 South Africa

- 5.5.4 Turkey

- 5.5.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 SABIC Agri-Nutrients Company (Saudi Basic Industries Corporation)

- 6.4.3 OCP Group

- 6.4.4 Ma'aden Phosphate Company (Saudi Arabian Mining Company - Ma'aden)

- 6.4.5 Qatar Fertiliser Company QAFCO (Industries Qatar)

- 6.4.6 ICL Group Ltd

- 6.4.7 K+S Aktiengesellschaft

- 6.4.8 EuroChem Group AG

- 6.4.9 PhosAgro PJSC

- 6.4.10 Fertiglobe PLC (OCI N.V.)

- 6.4.11 Omnia Fertilizer (Pty) Ltd (Omnia Holdings Ltd)

- 6.4.12 Dangote Fertilizer Ltd (Dangote Industries Ltd)

- 6.4.13 Indorama Eleme Fertilizer and Chemicals Ltd (Indorama Corporation)

- 6.4.14 Haifa Group

- 6.4.15 Jordan Phosphate Mines Company PLC

- 6.4.16 Golden Fertilizer Company Limited

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS