PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073611

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073611

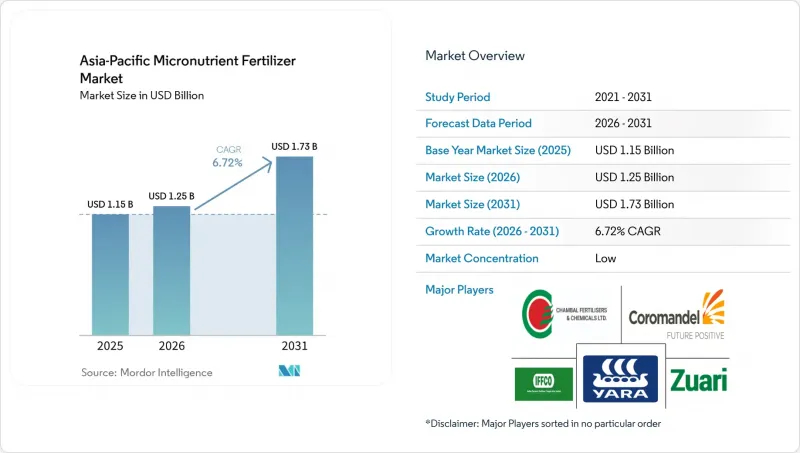

Asia-Pacific Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific micronutrient fertilizer market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.25 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, and More), Application Mode (Fertigation, Foliar, and More), Crop Type (Field Crops, Horticultural Crops, and More), and Geography (Australia, Bangladesh, China, India, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Micronutrient Fertilizer Market Trends and Insights

China's Zinc Subsidies Target Hidden Hunger Crisis

China's nutrition-centric subsidy scheme reallocates provincial funds toward zinc-enriched fertilizers that lift grain micronutrient density instead of merely boosting yields. The initiative reframes product success metrics around grain zinc content and aligns public health goals with farm-level practices, pushing the Asia-Pacific micronutrient fertilizer market toward value-added formulations. Field evidence shows foliar zinc delivers 55.2% higher biofortification efficacy than soil application, spurring R&D into next-generation foliar sprays. Multiplier effects arise as neighboring countries monitor China's program to replicate its public health gains, unlocking additional addressable demand for specialized suppliers.

Australia's Fertigation Revolution in Protected Horticulture

Water-scarce Australia prioritizes fertigation to minimize waste and fine-tune nutrient timing for high-density blueberries and other greenhouse fruit crops. This shift favors fully water-soluble chelated micronutrients that command premium pricing yet deliver measurable yield-and-quality gains. Early adopters report reductions in iron chlorosis episodes and improved firmness in export berries, catalyzing copy-cat investments in New Zealand and Southeast Asian greenhouses. Rising fertigation acreage, therefore, underwrites the fastest-growing application segment of the Asia-Pacific micronutrient fertilizer market.

Raw-Material Price Volatility Constrains Market Accessibility

China's mine closures under stringent environmental mandates curtail the supply of high-grade zinc sulfate ores, lifting feedstock costs and cascading into micronutrient price swings. Distributors struggle to hedge inventories, forcing periodic price hikes that strain smallholders' cash flow and hinder uptake. Chelated and nano formulations, which rely on purer inputs, bear disproportionate cost pressure, narrowing the adoption of these high-efficacy options within the Asia-Pacific micronutrient fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Platforms Accelerate Precision Micronutrient Applications

- Specialty-Crop Expansion Drives Customized Demand

- Credit Constraints Limit Premium Product Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for the largest Asia-Pacific micronutrient fertilizer market share, 34.2% in 2025, supported by widespread zinc deficiencies across agricultural soils and its critical role in crop growth, nutrient uptake, and yield improvement. The segment benefits from strong adoption across cereals, oilseeds, and horticultural crops, while continued product innovation in chelated, coated, and water-soluble formulations is enhancing nutrient-use efficiency. Growing government-led soil testing initiatives and balanced fertilization programs across major agricultural economies are further supporting zinc demand and reinforcing its leadership position in the Asia-Pacific micronutrient fertilizer market.

Boron is anticipated to be the fastest-growing product segment, with a projected CAGR of 9.2% during 2026 to 2031. This growth is fueled by the increasing cultivation of fruits, vegetables, oilseeds, and plantation crops, which require boron for flowering, pollination, fruit set, and quality improvement. The rising adoption of fertigation and foliar nutrient management practices is boosting demand for soluble and specialty boron formulations across various cropping systems. Meanwhile, micronutrients such as iron, copper, and manganese continue to address crop-specific nutrient deficiencies, ensuring a balanced portfolio of high-volume and value-added products in the Asia-Pacific micronutrient fertilizer market.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Geography

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Yara International ASA

- Chambal Fertilisers and Chemicals Limited

- Zuari Agro Chemicals Limited

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited

- Compo Expert GmbH (Grupa Azoty S.A.)

- Haifa Negev Technologies Ltd. (Haifa Group)

- ICL Fertilizers (ICL Group Ltd.)

- Kingenta Ecological Engineering Group Co., Ltd.

- Nutrien Ltd.

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Gujarat State Fertilizers and Chemicals Limited

- OMEX Agriculture Ltd. (OMEX Group)

- Valagro S.p.A. (Syngenta Group)

- Balchem Plant Nutrition (Balchem Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 China's Zinc Subsidies Target Hidden Hunger Crisis

- 4.6.2 Australia's Fertigation Revolution in Protected Horticulture

- 4.6.3 India's Soil Health Cards Drive Systematic Micronutrient Testing

- 4.6.4 Digital Platforms Accelerate Precision Micronutrient Applications

- 4.6.5 Specialty-Crop Expansion Drives Customized Demand

- 4.6.6 Consumer Demand for Fortified Foods Spurs Farm-Level Biofortification

- 4.7 Market Restraints

- 4.7.1 Raw-Material Price Volatility Constrains Market Accessibility

- 4.7.2 Credit Constraints Limit Premium Product Adoption

- 4.7.3 Counterfeit Products Erode Farmer Confidence

- 4.7.4 Port Bottlenecks Delay Chelated Micronutrient Exports

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Geography

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Chambal Fertilisers and Chemicals Limited

- 6.4.3 Zuari Agro Chemicals Limited

- 6.4.4 Coromandel International Limited

- 6.4.5 Indian Farmers Fertiliser Cooperative Limited

- 6.4.6 Compo Expert GmbH (Grupa Azoty S.A.)

- 6.4.7 Haifa Negev Technologies Ltd. (Haifa Group)

- 6.4.8 ICL Fertilizers (ICL Group Ltd.)

- 6.4.9 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.10 Nutrien Ltd.

- 6.4.11 Deepak Fertilisers and Petrochemicals Corporation Limited

- 6.4.12 Gujarat State Fertilizers and Chemicals Limited

- 6.4.13 OMEX Agriculture Ltd. (OMEX Group)

- 6.4.14 Valagro S.p.A. (Syngenta Group)

- 6.4.15 Balchem Plant Nutrition (Balchem Corporation)

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS