PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073617

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073617

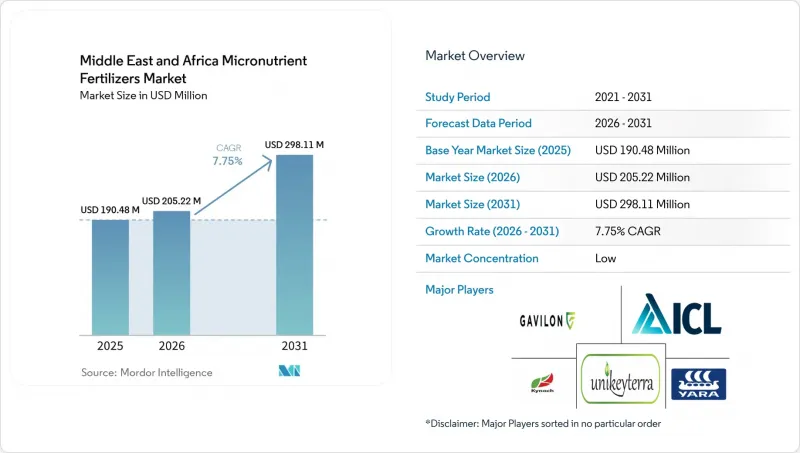

Middle East and Africa Micronutrient Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and Africa micronutrient fertilizers market size in 2026 is estimated at USD 205.22 million, up from 2025's USD 190.48 million, with 2031 projections showing USD 298.11 million, growing at a 7.75% CAGR over 2026-2031.

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and More), by Application Mode (Fertigation, Foliar, and More), by Crop Type (Field Crops, Horticultural Crops, and More), and by Geography (Nigeria, Saudi Arabia, South Africa, Turkey, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East and Africa Micronutrient Fertilizers Market Trends and Insights

Climate-Induced Soil Micronutrient Depletion

Soils across the Middle East and Africa are losing zinc, boron, iron, and manganese at an accelerating pace as hotter temperatures and more frequent sandstorms shear away fertile layers. Turkey's National Soil Health Program documented zinc and boron deficits in 65% of farmland in 2024 and showed a 23% deterioration over the last decade . Laboratory work at King Abdullah University of Science and Technology revealed that sustained soil temperatures above 45 °C cut zinc bioavailability by up to 40% in calcareous fields . This nutrient drain triggers yield losses of 15% to 30% and forces growers to adopt chelated blends that remain soluble in alkaline, moisture-scarce conditions. Continued regional warming and erosion mean corrective micronutrient strategies will stay central to farm profitability well past 2030. Satellite imagery corroborates expanding barren patches that align closely with documented micronutrient gaps.

Growth of Controlled-Environment Agriculture Hubs

Gulf nations are channeling unprecedented capital into vertical farms, hydroponic clusters, and climate-controlled greenhouses to improve food self-sufficiency. Saudi Arabia's NEOM blueprint assigns 10,000 hectares to indoor systems that depend on fully automated fertigation capable of dosing liquid chelates with sub-milliliter accuracy. The United Arab Emirates National Food Security Strategy mobilized USD 2 billion for similar facilities that consume three to five times more micronutrients per hectare than open fields because of higher plant densities and rapid crop cycles . Suppliers respond by formulating ultra-pure liquids that resist precipitation in recirculating lines and by installing cold-chain storage to prevent thermal degradation. As GCC producers scale output for premium local retail and export channels, demand for tech-enabled micronutrient solutions is set to intensify across adjacent markets such as Oman and Bahrain. These large-scale projects also anchor new agritech start-ups that bundle nutrient analytics software with fertigation hardware, enlarging the addressable customer base for specialty chelates.

Volatile Foreign-Exchange Regimes Impacting Import Costs

Sharp currency swings elevate landed costs for chelated inputs that rely on Euro- and Dollar-denominated raw materials. The Nigerian Naira slid 68% in 2024, forcing distributors to raise shelf prices by up to 60% for European-sourced. Turkish Lira volatility prompted suppliers to shorten credit terms, eroding affordability for smallholders who depend on seasonal financing. Hedging fees add another 8% to 12% to product pricing, while port congestion triggers demurrage that further bloats costs. Although some companies negotiate local-currency contracts for packaging and logistics, the chelate ligands themselves remain pegged to foreign exchange, locking in residual exposure. This volatility forces importers to hold buffer inventories, tying up working capital that could otherwise fund market development.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy Realignment Toward Balanced Fertilization

- Emergence of Specialty Chelated Blends for Arid Soils

- Fragmented Distribution Networks in the Sahel and the Horn of Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc captured 34.4% share of the Middle East and Africa micronutrient fertilizers market in 2025 because it corrects widespread soil deficiencies and underpins regional grain fortification mandates. The segment's leadership comes from the dual need to close yield gaps and raise the nutritional value of staple foods.

Molybdenum is forecast to grow the quickest at an 8.8% CAGR through 2031 as legume expansion and nitrogen-fixation programs accelerate its uptake. Iron and manganese blends continue to serve greenhouse tomatoes and peppers, where color and shelf life hinge on balanced levels of these trace elements. Copper demand is rising in Morocco's olives due to its combined nutritional and disease-control properties, and boron remains critical for fruit-quality management in Turkey and Mediterranean vegetables. Suppliers are bundling multi-micronutrient coatings that merge these elements into single granules, simplifying logistics for large cereal farms.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Geography

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

List of Companies Covered in this Report:

- Yara International ASA

- ICL Group Ltd

- Unikeyterra Tarim Sanayi ve Ticaret A.S.

- Kynoch Fertilizer (Maizey Investments Ltd)

- Gavilon South Africa (MacroSource, LLC)

- Azra Group Tarim A.S.

- BASF SE

- Haifa Chemicals Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile S.A. (SQM S.A.)

- Coromandel International Ltd (Murugappa Group)

- Valagro S.p.A. (Syngenta Group Co., Ltd.)

- BMS Micro-Nutrients NV

- Brandt Consolidated Inc.

- Grupa Azoty S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Climate-Induced Soil Micronutrient Depletion

- 4.6.2 Growth of Controlled-Environment Agriculture Hubs

- 4.6.3 Government Subsidy Realignment Toward Balanced Fertilization

- 4.6.4 Emergence of Specialty Chelated Blends for Arid Soils

- 4.6.5 Expansion of Zinc-Enriched Staple Food Fortification Mandates

- 4.6.6 Rise of Regenerative Agriculture Certification Schemes

- 4.7 Market Restraints

- 4.7.1 Volatile Foreign-Exchange Regimes Impacting Import Costs

- 4.7.2 Fragmented Distribution Networks in Sahel and Horn of Africa

- 4.7.3 Limited Local Production Capacity for Chelated Formulations

- 4.7.4 Farmer Price Sensitivity Amid Subsidy Phase-Outs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Geography

- 5.4.1 Nigeria

- 5.4.2 Saudi Arabia

- 5.4.3 South Africa

- 5.4.4 Turkey

- 5.4.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 ICL Group Ltd

- 6.4.3 Unikeyterra Tarim Sanayi ve Ticaret A.S.

- 6.4.4 Kynoch Fertilizer (Maizey Investments Ltd)

- 6.4.5 Gavilon South Africa (MacroSource, LLC)

- 6.4.6 Azra Group Tarim A.S.

- 6.4.7 BASF SE

- 6.4.8 Haifa Chemicals Ltd

- 6.4.9 Koch Industries Inc.

- 6.4.10 Sociedad Quimica y Minera de Chile S.A. (SQM S.A.)

- 6.4.11 Coromandel International Ltd (Murugappa Group)

- 6.4.12 Valagro S.p.A. (Syngenta Group Co., Ltd.)

- 6.4.13 BMS Micro-Nutrients NV

- 6.4.14 Brandt Consolidated Inc.

- 6.4.15 Grupa Azoty S.A.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS