PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073613

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073613

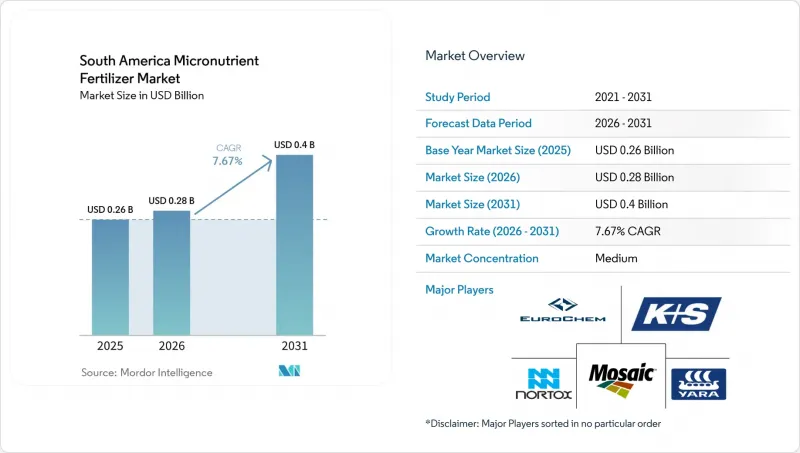

South America Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america micronutrient fertilizer market size was valued at USD 0.26 billion in 2025 and estimated to grow from USD 0.28 billion in 2026 to reach USD 0.40 billion by 2031, at a CAGR of 7.67% during the forecast period (2026-2031).

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and Others), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Micronutrient Fertilizer Market Trends and Insights

Widespread Zinc-Deficient Soils Driving Corrective Demand

Extensive soil tests reveal that more than half of Brazilian and Argentine croplands exhibit DTPA-extractable zinc levels below critical thresholds, underscoring a structural requirement for sustained zinc supplementation . These deficiencies span 12.15 million hectares across the Argentine Pampas alone . High-pH conditions in Brazil's Cerrado further diminish zinc bioavailability, even when total soil zinc appears sufficient. Resulting protein and grain-quality penalties erode export premiums, prompting growers to invest in corrective zinc programs that typically require two or more seasons to restore optimal status. Because soil zinc recovery is slow, a predictable replacement cycle stabilizes purchasing volumes for suppliers. The enduring nature of the deficiency anchors the long-term growth of the micronutrient fertilizer market.

Expansion of Soybean and Corn Acreage

Brazil's record grain harvest, projected at 341 million metric tons for 2025, reflects the continued expansion of soybean and corn acreage that today represents three-quarters of the planted area . Soybeans lift molybdenum demand by facilitating nitrogen fixation, while corn's high uptake of potassium and phosphorus often triggers secondary zinc and manganese deficiencies. Hybrid corn varieties require 15-20% more zinc to realize full yield potential, intensifying per-hectare micronutrient needs. Argentinian growers pushing into marginal lands face soils with lower organic matter, magnifying micronutrient depletion. Export contracts that now specify trace-element minimums reinforce the commercial necessity of balanced nutrient programs. Together, acreage gains and quality standards ignite recurring orders across the micronutrient fertilizer market.

High Price Sensitivity Among Smallholders

Roughly 60% of Brazilian and Argentine farms operate on less than 100 ha, and many rely on basic sulfate formulations costing around USD 800 per metric ton, while chelated alternatives often exceed USD 2,000 per metric ton. Credit programs prioritize NPK fertilizers, leaving micronutrients underfinanced. Cooperative purchases offset some costs, but struggle to align diverse soil needs. During commodity price dips, growers trim discretionary inputs, delaying chelated micronutrient adoption even when agronomic ROI is evident. Suppliers must therefore balance premium positioning with affordable entry-level offerings to sustain penetration in the micronutrient fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Precision-ag Adoption and Soil Testing Penetration

- National Fertilizer Plan 2050 Incentives for Domestic Supply

- Logistics Bottlenecks Inflating Delivered Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for 31.4% of the South America micronutrient fertilizer market zinc in 2025 and posted the fastest growth, with a 7.0% CAGR through 2026-2031. Corrective applications across 12.15 million hectares support its sustained leadership in the market. Demand for zinc-based micronutrient fertilizers is projected to expand steadily, driven by stringent grain-quality specifications in export contracts. Molybdenum, though smaller, accelerates as soybean acreage rises, elevating attention to nitrogen-fixing efficiency. Copper, iron, and manganese cater to crop-specific niches such as Chilean fruits, Argentine wheat, and high-pH soybean soils. Boron remains essential in flowering crops such as coffee and mango. Advanced chelation, notably EDDHA, gains traction in high-pH zones despite higher prices, signaling an ongoing shift from basic sulfates toward value-added chemistries.

Growing awareness of secondary deficiencies pushes growers to adopt multi-micro mixes that mitigate hidden yield losses. Suppliers that bundle zinc with manganese and boron capture cross-selling synergies. As Brazilian regulation fast-tracks domestic capacity, local chelate production may narrow price gaps, smoothing the adoption curve. Concurrently, patent activity in nano-encapsulation and controlled-release formats promises step-wise improvements in nutrient-use efficiency, further enriching the product landscape and supporting long-term market value growth.

Complete Report Scope:

- By Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- By Application Mode

- Fertigation

- Foliar

- Soil

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Country

- Argentina

- Brazil

- Rest of South America

List of Companies Covered in this Report:

- BMS Micro-Nutrients NV

- Grupa Azoty S.A. (Compo Expert GmbH)

- EuroChem Group

- Haifa Group

- ICL Group Ltd

- Inquima LTDA

- K+S Aktiengesellschaft

- Nortox S.A.

- The Mosaic Company

- Yara International ASA

- Nutrien

- SQM S.A.

- TIMAC Agro Brasil (Groupe Roullier)

- Koch Agronomic Services (Koch Industries Inc.)

- FertGrow

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Widespread zinc-deficient soils driving corrective demand

- 4.6.2 Expansion of soybean and corn acreage

- 4.6.3 Precision-ag adoption and soil-testing penetration

- 4.6.4 National Fertilizer Plan 2050 incentives for domestic supply

- 4.6.5 Premium micronutrient blends for specialty coffee and fruit exports

- 4.6.6 Sugarcane ethanol clusters adopting fertigation infrastructure

- 4.7 Market Restraints

- 4.7.1 High price sensitivity among smallholders

- 4.7.2 Logistics bottlenecks inflating delivered cost

- 4.7.3 Volatile by-product supply of industrial metals

- 4.7.4 Export-market scrutiny of chelate residues

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 By Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 By Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 By Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BMS Micro-Nutrients NV

- 6.4.2 Grupa Azoty S.A. (Compo Expert GmbH)

- 6.4.3 EuroChem Group

- 6.4.4 Haifa Group

- 6.4.5 ICL Group Ltd

- 6.4.6 Inquima LTDA

- 6.4.7 K+S Aktiengesellschaft

- 6.4.8 Nortox S.A.

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

- 6.4.11 Nutrien

- 6.4.12 SQM S.A.

- 6.4.13 TIMAC Agro Brasil (Groupe Roullier)

- 6.4.14 Koch Agronomic Services (Koch Industries Inc.)

- 6.4.15 FertGrow

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOs