PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911488

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911488

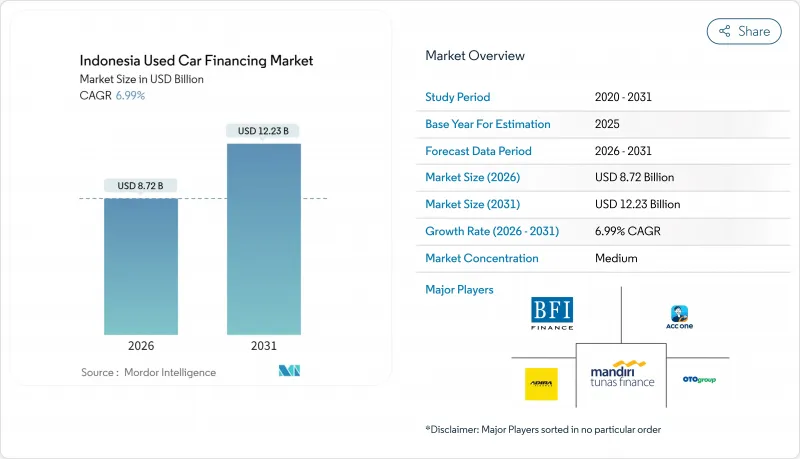

Indonesia Used Car Financing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Indonesian used car financing market was valued at USD 8.15 billion in 2025 and estimated to grow from USD 8.72 billion in 2026 to reach USD 12.23 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031).

This outlook captures strong latent demand even as wholesale new-car sales contract, because financing for pre-owned vehicles offers lower entry prices and smaller initial outlays. Digital lenders are scaling quickly; peer-to-peer loan balances grew 27.32% year-on-year to IDR 75.60 trillion; embedded-finance features on automotive marketplaces shrink approval times to minutes. Banks continue to dominate by volume, yet fintech and captive OEM arms widen credit access in underbanked clusters. Regulatory tightening on interest caps and mandatory liability insurance raises compliance costs, but it also strengthens consumer trust and should improve portfolio quality. Consolidation by foreign investors signals confidence in the Indonesian used car financing market's long-run profitability.

Indonesia Used Car Financing Market Trends and Insights

Robust Demand Shift from New- to Used-Cars Amid High Interest Rates

To combat inflation, Bank Indonesia has maintained its benchmark rate at a high level. This decision has increased borrowing costs for new vehicles, prompting many households to consider more affordable, pre-owned options. As a result, while wholesale volumes for new cars have declined, approvals for used car loans have surged. With average minimum wages, many consumers extend payment schedules, and these longer tenors facilitate more manageable installment payments. BCA's auto-loan portfolio rose 14.8% year-on-year, underlining sustained appetite for financed second-hand cars . Dealers respond by curating certified units and bundled insurance to support lender risk controls. The net effect lifts penetration of the Indonesian used car financing market across middle-income brackets.

Expansion of Multi-Finance and Bank Loan Portfolios into Used-Cars

Despite a nationwide decline in new-car sales, Toyota Astra Financial Services made significant auto loan disbursements in late 2024, demonstrating a strategic shift towards pre-owned assets. Meanwhile, due to meticulous collateral valuation, BFI Finance maintains non-performing ratios significantly lower than the industry average. OJK's development roadmap prioritizes automotive financing as an engine for broader financial inclusion, letting multi-finance companies tap new prudential capital sources . Such institutional support sustains the Indonesian used car financing market even when cyclical headwinds weigh on household sentiment.

Persistent Trust and Odometer Fraud Issues

KoinWorks incurred IDR 365 billion in losses from borrower fraud, underscoring systemic gaps in digital underwriting . Islamic banking assets are witnessing robust annual growth, fueling a surge in murabahah-based vehicle financing. Since 2020, Bank Syariah Indonesia has expanded its assets and started offering halal certification services alongside automotive loans, targeting a significant Muslim demographic. The OJK has introduced new guidelines that streamline product approvals and prioritize consumer protection. This move solidifies Sharia finance's role as a cornerstone in Indonesia's used car financing arena. Unlike traditional markets, this segment prioritizes religious compliance over pricing, enabling lenders to maintain their margins while broadening their reach beyond primary urban locales.

Other drivers and restraints analyzed in the detailed report include:

- Digital Marketplaces Embedding Instant Loan Approvals

- Growth of Sharia-Compliant Auto Finance Products

- Elevated Lending Rates and Macro-Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-Purpose Vehicles (MPVs) held 43.28% of the Indonesian used car financing market share in 2025 because multi-row seating suits family travel and ride-sharing side gigs. Average monthly installments for a three-year-old MPV remain within 30% of provincial minimum wages, reinforcing popularity. Sports Utility Vehicles (SUVs) are growing fastest at 7.98% CAGR during the forecast period (2026-2031) and now benefit from hybrid variants that lower fuel spend, supporting total cost of ownership. The Indonesia used car financing market size for SUVs is projected to expand 1.7 times by 2031 as infrastructure upgrades make larger vehicles practical across peri-urban zones.

New import entrants from China priced below Japanese peers widened choice and compressed residual values, making used SUVs attainable for middle-income customers. Dealers bundle two-year warranties and prepaid service to offset perceived maintenance risk. Marketplace analytics show SUVs record shorter listing-to-sale cycles than sedans, a pattern lenders exploit to manage collateral liquidation timelines. Consequently, lender risk models now factor in higher salvage values that reinforce loan-to-value comfort levels for the segment.

Banks' segment has a 69.60% share in the Indonesian used car financing market, as their grip on the target market reflects low funding costs from core deposits and multi-product relationships that allow cross-selling. Their branch footprint supports document verification, and Basel-aligned credit scoring maintains portfolio stability. Peer-to-peer and fintech lenders, however, are compounding at 8.86% during the forecast period (2026-2031)and target thin-file borrowers through telecom and e-wallet data. The Indonesia used car financing market size under fintech management could exceed USD 2.5 billion by 2031 if current momentum continues.

Regulation now requires fintechs to hold IDR 25 billion in paid-up capital, a filter that favors well-funded platforms. Strategic partnerships with insurers and warranty providers let them package risk-mitigation tools into every loan. Banks respond by launching API-based credit origination, cutting approval from two days to less than one hour. Competition thereby pivots on user experience and ancillary services rather than headline interest rates alone.

The Indonesia Used Car Financing Market Report is Segmented by Vehicle Type (Hatchback, Sedan, and More), Financing Provider (Captive OEM Finance, Commercial Banks, and More), Financing Tenor (<=24 Months, 25-48 Months, and More), Vehicle Age (<=3 Years Old, 4-7 Years Old, and More), and Province (Jakarta, West Java, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Astra Credit Companies (ACC)

- BFI Finance Indonesia

- Adira Dinamika Multi Finance

- Oto Multiartha

- Mandiri Tunas Finance

- PT Toyota Astra Financial Services

- Suzuki Finance Indonesia

- PT JACCS MPM Finance Indonesia

- BCA Finance

- Bussan Auto Finance

- Dipo Star Finance

- Batavia Prosperindo Finance

- BRI Multifinance Indonesia

- Clipan Finance Indonesia

- BNI Multifinance

- CIMB Niaga Auto Finance

- Bank Syariah Indonesia - OTO Finance

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Demand Shift from New- to Used-Cars Amid High Interest Rates

- 4.2.2 Expansion of Multi-Finance and Bank Loan Portfolios into Used-Cars

- 4.2.3 Digital Marketplaces Embedding Instant Loan Approvals

- 4.2.4 Growth of Sharia-Compliant Auto Finance Products

- 4.2.5 Buy-Now-Pay-Later Down-Payment Solutions

- 4.2.6 Second-Hand Hybrid and EV Incentives Creating Niche Demand

- 4.3 Market Restraints

- 4.3.1 Persistent Trust and Odometer Fraud Issues

- 4.3.2 Elevated Lending Rates and Macro-Volatility

- 4.3.3 Stricter OJK Caps on Fintech Lending Fees

- 4.3.4 Rise in Collateral Fraud and Stolen-Vehicle Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Economic Impact Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Hatchback

- 5.1.2 Sedan

- 5.1.3 Sport Utility Vehicle (SUV)

- 5.1.4 Multi-Purpose Vehicle (MPV)

- 5.2 By Financing Provider

- 5.2.1 Captive OEM Finance

- 5.2.2 Commercial Banks

- 5.2.3 Non-Bank Finance Companies

- 5.2.4 Peer-to-Peer / Fintech Lenders

- 5.3 By Financing Tenor

- 5.3.1 Less than/Equals 24 Months

- 5.3.2 25 - 48 Months

- 5.3.3 49 - 72 Months

- 5.3.4 Above 72 Months

- 5.4 By Vehicle Age

- 5.4.1 Less than/equals 3 Years Old

- 5.4.2 4 -7 Years Old

- 5.4.3 Above 7 Years Old

- 5.5 By Province

- 5.5.1 Jakarta

- 5.5.2 West Java

- 5.5.3 East Java

- 5.5.4 Central Java

- 5.5.5 Banten

- 5.5.6 North Sumatra

- 5.5.7 Other Provinces

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Astra Credit Companies (ACC)

- 6.4.2 BFI Finance Indonesia

- 6.4.3 Adira Dinamika Multi Finance

- 6.4.4 Oto Multiartha

- 6.4.5 Mandiri Tunas Finance

- 6.4.6 PT Toyota Astra Financial Services

- 6.4.7 Suzuki Finance Indonesia

- 6.4.8 PT JACCS MPM Finance Indonesia

- 6.4.9 BCA Finance

- 6.4.10 Bussan Auto Finance

- 6.4.11 Dipo Star Finance

- 6.4.12 Batavia Prosperindo Finance

- 6.4.13 BRI Multifinance Indonesia

- 6.4.14 Clipan Finance Indonesia

- 6.4.15 BNI Multifinance

- 6.4.16 CIMB Niaga Auto Finance

- 6.4.17 Bank Syariah Indonesia - OTO Finance

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment