PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939568

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939568

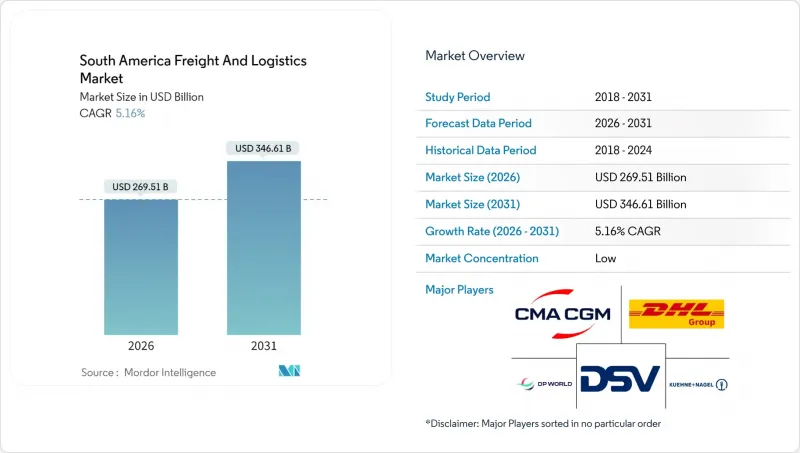

South America Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America freight and logistics market was valued at USD 256.29 billion in 2025 and estimated to grow from USD 269.51 billion in 2026 to reach USD 346.61 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031).

The expansion reflects the region's appeal as a nearshoring destination, continued infrastructure modernization, and rapid adoption of digital supply-chain solutions. Brazil retains scale benefits through its diversified industrial base and port network, while Peru's China-backed Chancay megaport is set to redirect Pacific trade flows and stimulate hinterland freight volumes. E-commerce growth is reshaping demand toward parcel-intensive networks that reward technology-enabled providers with agile last-mile capabilities. At the same time, climate-driven river level volatility, chronic road bottlenecks, and complex cross-border regulation temper the sector's growth potential.

South America Freight And Logistics Market Trends and Insights

E-Commerce Boom and Last-Mile Demand

Rapid digital retail adoption across metropolitan Brazil, Argentina, and Chile is transforming network design toward parcel-heavy flows that require dense micro-fulfillment footprints. Mercado Libre plans to raise its Brazilian distribution center count from 10 to 21 by end-2025 to support same-day and next-day delivery commitments. Heightened consumer expectations are pulling investment into urban sortation hubs and cold-chain micro-depots capable of meeting two-hour delivery windows for fresh groceries and pharmaceuticals. Parcel fragmentation pushes load factors down for traditional LTL yet enables premium pricing for time-definite services. Cross-border e-commerce among the three largest economies is adding international parcel volumes that test legacy customs procedures and stimulate demand for tech-enabled brokerage.

Nearshoring-Led Manufacturing Relocation

Supply-chain de-risking motivates automotive and electronics producers to relocate capacity from Asia-Pacific toward South America, generating bidirectional freight flows of components and finished goods. Brazil's industrial clusters attract suppliers seeking tariff advantages within MERCOSUR, while Mexico's competitiveness raises pressure on southern neighbors to streamline logistics costs. Integrated providers that can orchestrate multimodal moves and regulatory compliance stand to capture disproportionate share. Facility siting decisions hinge on infrastructure quality; therefore, logistics firms that invest in bonded warehousing close to manufacturing zones create compelling value propositions.

Chronic Road and Rail Bottlenecks

Capacity limitations in Brazil's Santos corridor, Argentina's Rosario grain routes, and Chile's copper corridors translate into prolonged dwell times and demurrage costs exceeding USD 200 per container during peak seasons. Legacy single-track rail and outdated signaling hamper modal shifts that could relieve road congestion. Funding gaps slow double-tracking and intermodal terminal upgrades. Incumbent providers with dedicated capacity maintain pricing power, while start-ups reliant on fluid networks struggle to scale.

Other drivers and restraints analyzed in the detailed report include:

- Port and Corridor Infrastructure Upgrades

- Digital Freight Platforms Improving Truck Load Factors

- High Logistics Taxes and Tolls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 34.68% of the South America freight and logistics market size in 2025, anchored by Brazil's autos and electronics clusters. Producers favor near-port locations to minimize inland drayage complexity. Wholesale and retail trade is projected for a 5.42% CAGR (2026-2031)as rising urban purchasing power fuels consumption-driven logistics. Retailers deploy regional distribution centers with embedded cross-dock functions that consolidate inbound freight and stage parcels for last-mile delivery.

Agriculture remains structurally significant during harvest cycles, yet compliance-heavy cold-chain exports provide higher margins than bulk grain shipments. Oil and gas cargoes display lower growth but stable volumes that support specialized tank container operators. Construction freight demand tracks infrastructure spending surges, rewarding carriers with flexible capacity contracts. Convergence of retail replenishment and manufacturing inputs creates opportunities for integrated providers that reuse assets across supply-chain stages.

Freight transport contributed the largest revenue slice, equal to 61.37% of the South America freight and logistics market size in 2025. Commodity exports, import replenishment, and industrial resupply underpin sustained bulk and container flows. CEP activities are forecast for a 5.73% CAGR (2026-2031), catalyzed by urban e-commerce and same-day delivery commitments. The South America freight and logistics market share held by legacy truckload carriers will trend lower as asset-light parcel platforms widen service reach. Providers integrating freight forwarding with temp-controlled warehousing gain pricing leverage by bundling compliance services for high-growth agrifood exporters.

Technology adoption also reshapes value pools. Load-matching applications increase truck utilization, allowing small fleets to penetrate formerly relationship-based freight networks. Freight forwarding retains relevance by navigating EU carbon adjustment mechanisms and deforestation certifications that increase documentary burden. Expeditors' 31% Latin American revenue jump in Q3 2024 illustrates the premium demand for compliance-centric forwarding.

The South America Freight and Logistics Market Report is Segmented by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Wholesale and Retail Trade, Others), and Geography (Chile, Argentina, and Brazil). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Agencias Universales SA (AGUNSA)

- Alonso Group

- Americold

- CMA CGM Group (Including CEVA Logistics)

- Correios

- DHL Group

- DP World

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx Corp.

- Kuehne+Nagel

- Log-In Logistica Integrada

- MercadoLibre, Inc.

- Rappi Logistics

- Romeu

- Rumo Logistica

- SAAM

- Scan Global Logistics (Including Blu Logistics)

- TASA Logistica

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.22.1 Argentina

- 4.22.2 Brazil

- 4.22.3 Chile

- 4.22.4 Peru

- 4.23 Regulatory Framework (Sea and Air)

- 4.23.1 Argentina

- 4.23.2 Brazil

- 4.23.3 Chile

- 4.23.4 Peru

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Boom and Last-Mile Demand

- 4.25.2 Nearshoring-Led Manufacturing Relocation

- 4.25.3 Port and Corridor Infrastructure Upgrades

- 4.25.4 Digital Freight Platforms Improving Truck Load Factors

- 4.25.5 Cold-Chain Compliance for High-Value Agrifood Exports

- 4.25.6 Regional Free-Trade Agreements Deepening Customs Union

- 4.26 Market Restraints

- 4.26.1 Chronic Road and Rail Bottlenecks

- 4.26.2 High Logistics Taxes and Tolls

- 4.26.3 Mercosur Cross-Border Regulatory Fragmentation

- 4.26.4 Climate-Driven Disruption (Floods, Droughts)

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Suppliers

- 4.28.3 Bargaining Power of Buyers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Peru

- 5.3.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Agencias Universales SA (AGUNSA)

- 6.4.2 Alonso Group

- 6.4.3 Americold

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Correios

- 6.4.6 DHL Group

- 6.4.7 DP World

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 Expeditors International of Washington, Inc.

- 6.4.10 FedEx Corp.

- 6.4.11 Kuehne+Nagel

- 6.4.12 Log-In Logistica Integrada

- 6.4.13 MercadoLibre, Inc.

- 6.4.14 Rappi Logistics

- 6.4.15 Romeu

- 6.4.16 Rumo Logistica

- 6.4.17 SAAM

- 6.4.18 Scan Global Logistics (Including Blu Logistics)

- 6.4.19 TASA Logistica

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment