PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044257

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044257

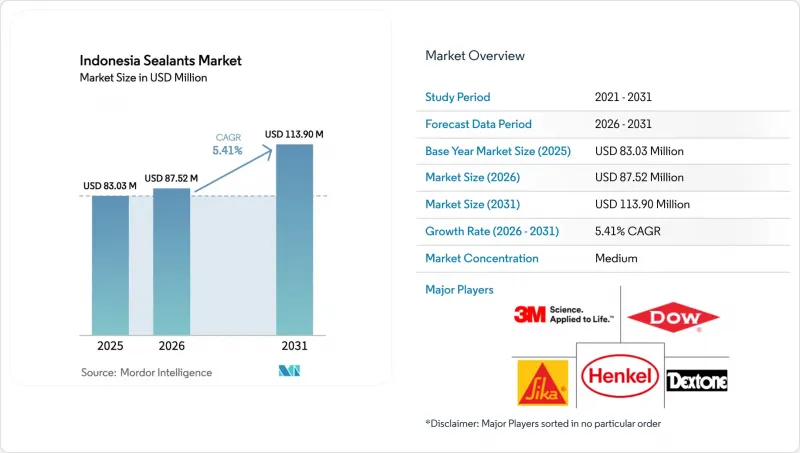

Indonesia Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Indonesia Sealants Market size is expected to grow from USD 83.03 million in 2025 to USD 87.52 million in 2026 and is forecast to reach USD 113.90 million by 2031 at 5.41% CAGR over 2026-2031. In Indonesia, a surge in residential and industrial construction, coupled with investments in electric vehicle assembly in West Java and a shipbuilding revival in Sulawesi, is driving the adoption of weather-proofing, structural, and marine-grade formulations. Multinational brands are ramping up local production to meet mandatory SNI certification and tropical-performance testing. Meanwhile, a draft regulation on low-VOC emissions set for the 2026-2031 period is pushing demand toward waterborne acrylic and alpha-silane chemistries. Additionally, while low-cost imports from China are putting pressure on commodity prices, there is a noticeable shift toward differentiated products, bolstered by technical services and local validation.

Indonesia Sealants Market Trends and Insights

OEM Automotive Line Expansion in West Java

By March 2026, BYD's electric-vehicle plant in Subang will have neared completion. With a target for annual production capacity, the plant is expected to influence the demand for silicone thermal-interface materials and polyurethane structural sealants. In June 2025, IMAS and GAC Aion inaugurated a scalable facility in Purwakarta, with a notable portion of their components sourced locally. These initiatives are projected to boost the forecast CAGR for the period 2026-2031 by creating a consistent demand for battery-housing gaskets, lightweight body bonding, and cabin air-tightening sealants. Wacker's expansion of specialty silicones capacity in the Asia-Pacific region ensures a steady supply for Indonesian OEM tiers. As the industry transitions from internal combustion engines to battery packs, certain engine-bay applications have diminished. However, this shift has created opportunities for more valuable electrification joints, elevating quality standards in Indonesia's sealants market.

Tropical-Climate Weather-Seal Retrofits

In Indonesia, where humidity levels consistently range from 70% to 90% and annual rainfall can peak at 6,000 mm, sealants experience reduced lifespans. This climatic hurdle has spurred a steady demand for retrofitting in areas such as glazing, facade joints, and sanitary grades. In recent years, as the building sector has expanded, developers, acutely aware of humidity challenges, have emphasized mitigation strategies, particularly in high-occupancy projects. By 2024, Sika had broadened its retail footprint, a strategic move in tune with Indonesia's growing trend of do-it-yourself sealant replacements. Although SNI-mandated tropical durability testing can extend product approval by four to eight weeks, showcasing resilience against hydrolytic and fungal stress is becoming a pivotal branding edge. With the e-commerce boom, there is an escalating demand for warehouses, amplifying the need for flexible, forklift-resistant floor-joint sealants. These sealants must endure the challenges posed by heavy machinery and the country's pronounced moisture fluctuations.

Rising Inflow of Low-Cost Chinese Imports

In July 2025, Indonesia saw a surge in imports of caulking compounds and adhesive preparations from China, with the latter offering substantial discounts over local brands. These imports, including toluene di-isocyanate and silicone polymers, enabled aggressive under-pricing, thereby tightening profit margins for Indonesia's commodity-grade sealant suppliers. In 2025, Henkel restructured its Southeast Asia distributorship, underscoring how global entities recalibrated their market strategies to combat budget-friendly competitors while enhancing their premium service image. Despite the introduction of carbon-levy mechanisms under Regulation 110/2025, aimed at penalizing high-emission imports to bridge the cost gap, the immediate pricing pressures still cast a slight shadow on growth during the forecast period of 2026-2031.

Other drivers and restraints analyzed in the detailed report include:

- Low-VOC Siloxane Reformulation Push

- Sulawesi Shipbuilding Corridor Stimulus

- Certification and Skilled-Labor Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, silicone secured a commanding 44.22% revenue share in Indonesia's sealants market, primarily due to its exceptional ultraviolet (UV) stability and adhesion. These attributes are critical for the archipelago's humid, high-rainfall climate. Conversely, acrylic grades are projected to register the highest compound annual growth rate (CAGR) of 5.83% during the forecast period of 2026-2031. This trend is attributed to a growing preference among contractors for cost-effective, low-volatile organic compound (VOC) solutions for residential retrofits, a shift catalyzed by Regulation 110/2025.

Silicone's elastic recovery and biocide-friendly formulation ensure that facade and sanitary joints can withstand daily wet-dry cycles, with a lifespan of 10 to 15 years. Simultaneously, the demand for acrylic roof and wall fillers in Indonesia is increasing, driven by government housing subsidies that encourage repainting and leakage repairs. In the automotive sector, polyurethane plays a critical role in bonding and securing joints in warehouse flooring, where tensile adhesion exceeding 1.5 megapascal (MPa) is essential. This segment is also benefiting from the rapidly expanding West Java Electric Vehicle corridor. Furthermore, hybrid alpha-silane technologies, developed at Wacker's Asian facilities, combine the flexibility of silicone with the adhesion strength of polyurethane. These advancements offer tin-free alternatives, aligning with future VOC regulations.

The Indonesia Sealants Market Report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins), End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- DEXTONE INDONESIA

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI S.p.A.

- Momentive

- Pidilite Industries Ltd

- RPM International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM automotive line-expansion in West Java

- 4.2.2 Growing demand for tropical-climate weather-seal retrofits

- 4.2.3 Eco-friendly low-VOC siloxane push (2027 draft MoEF rule)

- 4.2.4 Sulawesi shipbuilding corridor fueling marine-grade uptake

- 4.2.5 E-commerce logistics hubs needing high-movement floor joints

- 4.3 Market Restraints

- 4.3.1 Rising inflow of low-cost PRC imports

- 4.3.2 Prolonged SNI certification for aerospace-grade sealants

- 4.3.3 Skilled applicator shortage outside Java

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison

- 6.4.4 BASF SE

- 6.4.5 Carlisle Companies

- 6.4.6 DEXTONE INDONESIA

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Illinois Tool Works

- 6.4.11 MAPEI S.p.A.

- 6.4.12 Momentive

- 6.4.13 Pidilite Industries Ltd

- 6.4.14 RPM International Inc.

- 6.4.15 Shin-Etsu Chemical Co., Ltd.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 Tremco

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment