PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066694

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066694

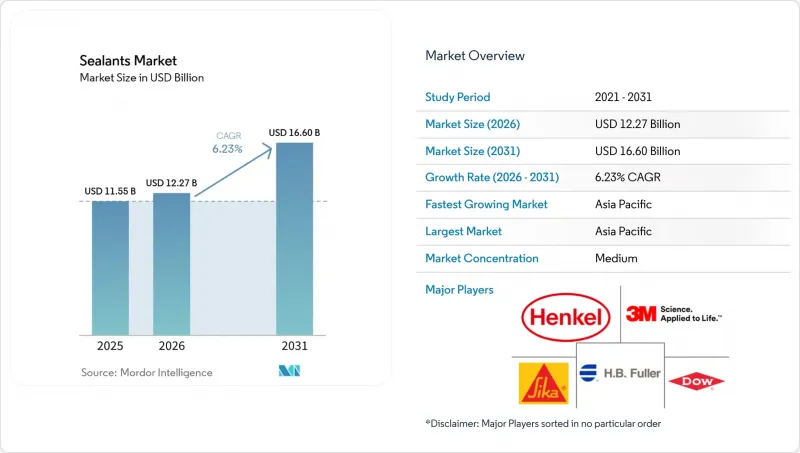

Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sealants market size was valued at USD 11.55 billion in 2025 and is estimated to grow from USD 12.27 billion in 2026 to reach USD 16.60 billion by 2031, at a CAGR of 6.23% during the forecast period (2026-2031).

This report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins), End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (USD).

Global Sealants Market Trends and Insights

Growth in Global Infrastructure Spending

Governments and multilateral lenders committed to infrastructure programs in 2025, showing an increase over 2024. Bridge-deck expansion joints, tunnel gaskets, and pipeline seals all rely on polysulfide or polyurethane grades that tolerate +-50% movement without cohesive failure. India's National Infrastructure Pipeline earmarks resources for highways, metro rail, and port modernization, each requiring robust jointing materials that comply with ASTM C920 Class 25.

China's Belt and Road Initiative continues to fund rail corridors and deep-water terminals that specify two-component silicone systems capable of tack-free cure in high-humidity climates. Public-private partnerships are compressing bid schedules, so suppliers that secure early design approvals under ISO 11600 gain a strategic advantage. Overall, higher public capital outlays enlarge the sealants market by widening the installed base of joints that need initial sealing and periodic renewal.

Lightweighting and Multi-Material Bonding in Electric Vehicles

Battery-electric vehicle production increased significantly in 2025. Automakers are replacing steel closures with aluminum and carbon-fiber composites, creating galvanic-corrosion risks that mechanical fasteners cannot manage. Structural sealants bridge dissimilar substrates, damp vibration, and supply dielectric insulation inside battery packs that cycle between -40 °C and +85 °C. Formulations such as SikaPower flexible epoxies incorporate flame-retardant fillers, extending thermal-runaway escape time beyond the 5-minute threshold set by UN ECE R100.03. As lithium-iron-phosphate chemistries have lower energy density, designers lengthen modules and increase linear seal length, boosting grams-per-vehicle consumption. The automotive drive toward lighter, quieter, and safer platforms, therefore, channels steady incremental revenue to the sealants market.

VOC and REACH Tightening Driving Reformulation Costs

REACH Annex XVII has set a VOC content limit for interior sealants, while California's Rule 1168 imposes an even stricter ceiling. Reformulating products to meet these thresholds requires significant investment and time. This process includes accelerated weathering tests and third-party GREENGUARD evaluations. When aromatic solvents are replaced with acetone or tertiary butyl acetate, the open time decreases. As a result, applicators need to adjust their bead-laying speed to prevent voids. Additionally, water-based acrylics necessitate biocides and freeze-thaw stabilizers, complicating packaging and increasing raw material costs. Producers in the region, lacking polymer synthesis capabilities, are forced to pay a premium for pre-formulated low-VOC resins. Consequently, while compliant products are poised to capture a larger market share, the immediate profitability of the sealants market faces challenges.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Performance Weatherproofing in Smart Buildings

- Rapid Expansion of Asia-Pacific End-Markets

- Silicone Monomer Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone products controlled 44.11% of 2025 volume, confirming their role as the durability benchmark for high-movement joints, high-temperature gaskets, and ultraviolet-exposed facades. Acrylic chemistries, propelled by water-based carriers that meet 50 g/L VOC limits, are advancing at a 6.21% CAGR through 2031, eroding silicone share in porous-substrate applications. Polyurethanes occupy a mid-market niche, balancing abrasion resistance and paintability, which suits parking deck and plaza joints. Epoxies remain confined to chemical-processing and wastewater environments because brittleness restricts dynamic movement. Polysulfides, butyls, and latex acrylics round out the mix, with polysulfides holding a foothold in insulated-glass units thanks to moisture-vapor-transmission rates under 3 g/m2*day. Intensifying disclosure under ISO 11600 forces resin suppliers to publish modulus and elongation profiles across temperatures, enabling specifiers to match products to calculated joint movement. Silicone makers counter the acrylic advance with neutral-cure, primerless grades that adhere to polyethylene and polypropylene without plasma treatment, while hybrid silyl-terminated polyether systems blend UV endurance and paintability to open new niches. Collectively, resin innovation keeps the sealants market dynamic and favors producers able to scale specialty monomer supply.

Geography Analysis

Asia-Pacific accounted for 36.13% of global demand in 2025 and is on track for a 7.32% CAGR to 2031. China continues to headline consumption through residential tower construction, yet new rules from the Green Building Evaluation Standard cap sealant emissions at 0.05 mg/m3*h, accelerating the switch from solvent to water-based systems. India's automotive output hit record vehicles in 2025, with electric two- and three-wheelers comprising a significant portion of the mix, creating local demand for battery-pack sealants serviced by joint ventures between Pidilite and Japanese silicone suppliers. Southeast Asian nations such as Vietnam and Indonesia are attracting electronics and vehicle assembly as supply chains diversify, lifting call-offs for clean-room and thermally conductive grades. Japan and South Korea, relatively mature markets, still see growth in semiconductor and fuel-cell sealing that depends on ultra-pure silicones.

Asia-Pacific leads in growth, while North America and Europe, together accounting for a significant portion of the 2025 volume, lag. The United States, buoyed by the Infrastructure Investment and Jobs Act, is witnessing a steady demand surge. This act funds bridge repairs and transit upgrades, specifically calling for polyurethane and polysulfide joint systems rated for +-50% movement. Meanwhile, Europe's Renovation Wave, aiming for energy upgrades on millions of buildings by 2030, is driving up demand for low-modulus silicone perimeter seals that enhance airtightness. Additionally, REACH Annex XVII is compelling local reformulations, thereby raising entry barriers and bolstering incumbents with their research and development scale.

South America and the Middle East-Africa account for the remaining market share. In Saudi Arabia, the Public Investment Fund has allocated significant resources for NEOM and other mega-projects. These projects mandate low-modulus polyurethane facade joints, designed to withstand desert temperature fluctuations. Over in Brazil, the offshore build-out is pushing the need for polysulfide and epoxy grades, specifically those resistant to seawater immersion. South Africa, on the other hand, is driving demand for UV-stable silicones in photovoltaic module sealing, thanks to its renewed focus on renewable energy. While these regions may be smaller in absolute terms, they present growth opportunities for seasoned formulators. Those willing to navigate the challenges of extreme climates and stringent technical specifications stand to significantly boost their stake in the sealants market.

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI S.p.A.

- Momentive

- Pidilite Industries Ltd

- RPM International

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- THE YOKOHAMA RUBBER CO., LTD.

- ThreeBond Holdings Co., Ltd.

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in global infrastructure spending

- 4.2.2 Lightweighting and multi-material bonding in Electricle Vehicles

- 4.2.3 Demand for high-performance weather-proofing in smart buildings

- 4.2.4 Rapid expansion of Asia-Pacific end-markets

- 4.2.5 Adoption of automated/robotic dispensing lines

- 4.3 Market Restraints

- 4.3.1 VOC and REACH tightening driving reformulation costs

- 4.3.2 Silicone monomer price volatility

- 4.3.3 Skilled-labour gap for correct application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Singapore

- 5.3.1.9 Australia

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison

- 6.4.4 BASF SE

- 6.4.5 Carlisle Companies

- 6.4.6 Dow

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Illinois Tool Works

- 6.4.10 MAPEI S.p.A.

- 6.4.11 Momentive

- 6.4.12 Pidilite Industries Ltd

- 6.4.13 RPM International

- 6.4.14 Saint-Gobain

- 6.4.15 Shin-Etsu Chemical Co., Ltd.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 THE YOKOHAMA RUBBER CO., LTD.

- 6.4.19 ThreeBond Holdings Co., Ltd.

- 6.4.20 Tremco

- 6.4.21 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment