PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066688

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066688

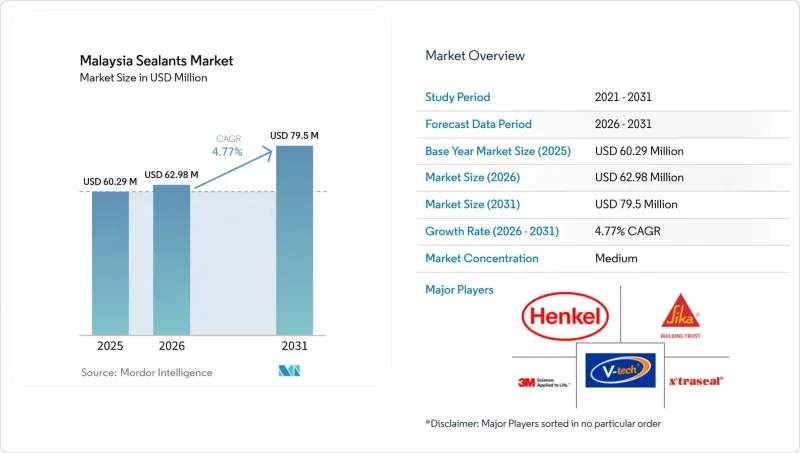

Malaysia Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaysia sealants market size was valued at USD 60.29 million in 2025 and is estimated to grow from USD 62.98 million in 2026 to reach USD 79.5 million by 2031, at a CAGR of 4.77% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Silicone, Polyurethane, Acrylic, Epoxy, and Others) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, Electronics and Electricals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Sealants Market Trends and Insights

Surge in Public-Sector Megaproject Pipeline Boosts Construction Sealant Demand

The East Coast Rail Link reached 92.62% completion in early 2026, injecting RM 50.27 billion (USD 11.3 billion) into sealant-intensive viaducts, tunnels, and station envelopes. Parallel programs such as MRT-3 and the Johor Bahru-Singapore Rapid Transit System Link deepen volume, but the real shift stems from the 70% IBS requirement that relocates joint sealing from outdoor sites to climate-controlled factories. Controlled curing cuts rework, shortens project cycles, and favors suppliers skilled in automated dispensing. The Construction Industry Development Board's (CIDB) 2025 Competency Standard adds Building Information Modeling proficiency to contractor licensing, pushing improper joint design from a warranty concern to a compliance risk.

Medical-Device Export Boom Driving Need for Sterilizable Silicone Grades

Malaysia's medical-device exports climbed to RM 37 billion in 2024 after RM 20 billion of cumulative investment since 2021, prompting demand for FDA-compliant silicone sealants that tolerate repeated 134 °C steam sterilization without extractables. Continuous-flow sterilization lines require faster tack-free times to avert bottlenecks, shifting preference toward platinum-catalyzed grades. Local formulators that can certify ISO 10993 biocompatibility gain pricing power, particularly as Penang's cleanroom builders look for seal-and-sensor solutions that streamline validation.

Volatile Silicone-Monomer Prices Squeezing SME Formulators' Margins

Double-digit cost swings since 2024, sparked by Chinese plant outages and feedstock spikes, are eroding margins at SMEs without hedging capacity. Wacker's incremental builds in South Korea and Japan have not neutralized regional tightness, so local formulators face unpredictable cost baselines. Consolidation is accelerating: integrated producers are acquiring niche brands to lock in distribution. Some SMEs are pivoting to MS-polymer or acrylic systems with steadier input costs but narrower application windows.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Modular Building Systems Accelerates Factory-Applied Sealant Usage

- Growing EV Assembly Stimulates High-Temperature Battery-Pack Sealant Uptake

- Labor-Skill Shortages Causing Premature Joint Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone held a 39.50% Malaysia sealants market share in 2025 because aerospace fuel-tank sealing, medical-device cleanrooms, and curtain-wall facades cannot compromise on UV stability and temperature resistance. Polyurethane is forecast to grow at a 6.02% CAGR through 2031, pushed by EV battery-pack modules that bond aluminum cooling plates to composite casings. Acrylic serves mid-rise residential interiors where paintability trumps movement capability, while epoxy fills chemical-resistant flooring niches.

The Malaysia sealants market size for MS-polymer hybrids is small today, but expanding as fabricators seek isocyanate-free systems that still accept paint. VITAL TECHNICAL claims over 50% regional share in MS-polymer sales and is leveraging eight-minute tack-free times to win factory-line approvals. Specialty grades, intumescent, underwater curing, and fire-rated systems, round out the resin palette and are shaped by rising SIRIM certification of low-VOC formulations.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- Chemibond Enterprise Sdn Bhd

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Mapei S.p.A.

- Mohm Chemical Sdn. Bhd.

- Momentive Performance Materials

- Pidilite Industries Ltd.

- RPM International Inc.

- Selic Corp.

- Sika AG

- Soudal Group

- VITAL TECHNICAL Sdn Bhd

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in public-sector megaproject pipeline boosts construction sealant demand

- 4.2.2 Medical-device export boom driving need for sterilizable silicone grades

- 4.2.3 Shift to modular/industrialised building systems (IBS) accelerates factory-applied joint-sealant usage

- 4.2.4 Growing EV assembly in Tanjung Malim and Kulim stimulating high-temperature battery-pack sealant uptake

- 4.2.5 Aerospace MRO cluster expansion in Selangor fuels demand for fuel-tank and structural sealants

- 4.3 Market Restraints

- 4.3.1 Volatile silicone monomer prices squeezing SME formulators' margins

- 4.3.2 Labour-skill shortages causing improper application and premature joint failures

- 4.3.3 Delayed adoption of Malaysia-specific low-VOC standards creating regulatory uncertainty

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Existing Competitors

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicone

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Epoxy

- 5.1.5 Others

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Electronics and Electricals

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Chemibond Enterprise Sdn Bhd

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 Mapei S.p.A.

- 6.4.10 Mohm Chemical Sdn. Bhd.

- 6.4.11 Momentive Performance Materials

- 6.4.12 Pidilite Industries Ltd.

- 6.4.13 RPM International Inc.

- 6.4.14 Selic Corp.

- 6.4.15 Sika AG

- 6.4.16 Soudal Group

- 6.4.17 VITAL TECHNICAL Sdn Bhd

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment