PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066680

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066680

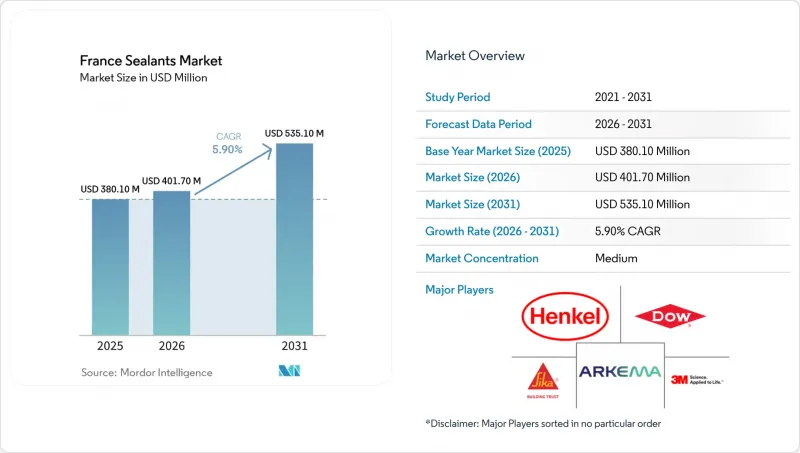

France Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france sealants market size is projected to grow from USD 380.10 million in 2025 to USD 401.70 million in 2026, and reach USD 535.10 million by 2031, growing at a CAGR of 5.90% from 2026 to 2031.

This report is Segmented by Resin Type (Silicone, Polyurethane, Acrylic, Epoxy, and Other Resins) and End-User Industry (Aerospace, Automotive and Transportation, Building and Construction, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

France Sealants Market Trends and Insights

Renovation-Led Demand Surge in Energy-Efficient Building Envelope Upgrades

MaPrimeRenov' extended cash advances up to 50% for very modest households through December 2025, stimulating immediate purchases of silicone and polyurethane sealants for thermal bridges, roof junctions, and duct penetrations. Fluid-applied silicone air-and-water barriers such as Momentive Elemax 2600 can reduce HVAC energy use by as much as 35% by limiting uncontrolled airflow, an attractive payback lever in retrofit settings where sheet membranes are difficult to place. The subsidy's raised cost ceiling to 80% for middle-income households broadens access to premium low-VOC products carrying French FDES declarations, ensuring airtightness compliance under HQE Cible 8 targets. Mandatory ISO 11600 Class 25 movement and EN 15651-2 designations safeguard joint durability in glazing and facade works. These policy and standard frameworks collectively lock in a multi-year demand cycle for high-performance building sealants.

EV Lightweighting Requirements in French Automotive Production

Multi-material bonding, aluminum to carbon-fiber-reinforced polymer and steel to composites, is displacing mechanical fasteners in EV body-in-white architecture, pushing consumption of shear-resistant epoxy and polyurethane adhesives that double as vibration dampers and battery-case sealants. Henkel's April 2025 reveal of AI-generated virtual adhesives and debondable chemistries anticipates EU battery-passport rules that will require traceability and end-of-life disassembly. Acrylic-epoxy hybrids activated by UV in minutes are improving line takt times and adhesion to low-energy plastics when pre-treated with plasma, enabling higher throughput at Stellantis and Renault plants. Evolving LEED v4 and SCAQMD Rule 1168 thresholds below 250 g/L VOC are giving MS polymers an advantage, delivering +-25% to +-50% movement without isocyanate exposure. The combined regulatory and production drivers keep automotive grade sealants on a robust growth path.

Petrochemical Feedstock Price Volatility

With raw materials representing roughly 50% of revenue, French formulators struggle to pass spikes through quarterly construction contracts, compressing EBITDA. BASF's MDI expansion in Geismar may ease tightness by 2027, yet geopolitical risk continues to swing benzene and naphtha costs, exposing sealant makers to margin whiplash. Those without hedging must choose between volume attrition and profit erosion, especially given the persistence of lower-priced Asian imports.

Other drivers and restraints analyzed in the detailed report include:

- Composite Bonding Growth in Airbus and Regional Aerospace Clusters

- Repairability-Index Law Boosting DIY and Appliance Maintenance Sealant Sales

- Stricter EU REACH Limits on Di-Isocyanates Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone captured 38.5% of the France sealants market share in 2025, powered by irreplaceable demand in structural glazing, insulating glass units, and weatherproof facades. Sikasil IG-25 HM Plus meets EN 1279-4 and ASTM C1184, securing gas-retention in vacuum-insulated glazing which commands premium unit prices. Polyurethane is set to pace the France sealants market size expansion, growing 7.24% CAGR during 2026-2031 as EV assemblers bond aluminum, CFRP, and steel modules, substituting welds to cut weight and extend battery range.

Acrylics remain relegated to interior static joints where paintability and near-zero VOC confer decorative advantages, but low movement capability limits outdoor use. Epoxies command niche industrial flooring and aerospace applications where tensile strength and chemical resistance justify slow cure; Baxxodur EC 151 allows functional cure at 5 °C, expanding winter construction windows. Polysulfides and MS polymers fill specialized roles, fuel-tank sealing and isocyanate-free construction joints, respectively, but face medium-term substitution risk from bio-based entrants.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- BASFIKA Produits Chimiques

- Bolton Group

- CERMIX

- Den Braven France

- DL Chemicals NV

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- ISPO Group

- MAPEI S.p.A.

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soprema Group

- Soudal NV

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation-led demand surge in energy-efficient building envelope upgrades

- 4.2.2 EV lightweighting requirements in French automotive production

- 4.2.3 Composite bonding growth in Airbus and regional aerospace clusters

- 4.2.4 Repairability-index law boosting DIY and appliance maintenance sealant sales

- 4.2.5 Marine-grade sealants demand from French offshore-wind build-out

- 4.3 Market Restraints

- 4.3.1 Petrochemical feedstock price volatility

- 4.3.2 Stricter EU REACH limits on di-isocyanates raising compliance costs

- 4.3.3 Emerging bio-based adhesive substitutes eroding conventional sealant share

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicone

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Epoxy

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive and Transportation

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 BASFIKA Produits Chimiques

- 6.4.5 Bolton Group

- 6.4.6 CERMIX

- 6.4.7 Den Braven France

- 6.4.8 DL Chemicals NV

- 6.4.9 Dow

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Illinois Tool Works

- 6.4.13 ISPO Group

- 6.4.14 MAPEI S.p.A.

- 6.4.15 RPM International Inc.

- 6.4.16 Saint-Gobain Weber

- 6.4.17 Sika AG

- 6.4.18 Soprema Group

- 6.4.19 Soudal NV

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment