PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066687

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066687

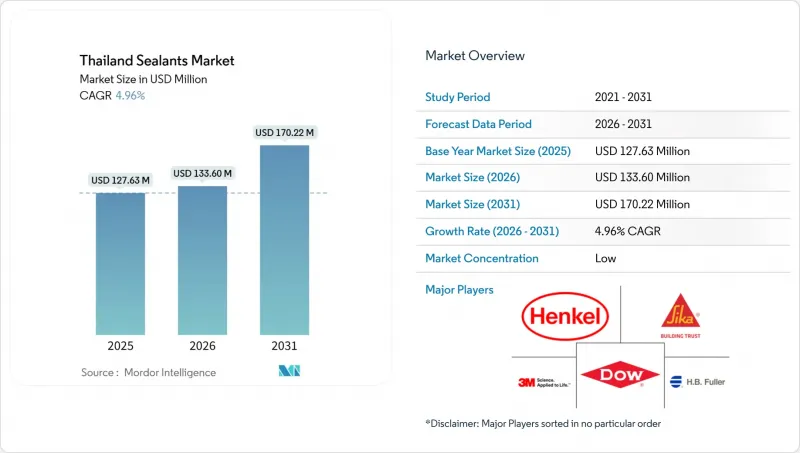

Thailand Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the thailand sealants market size is projected to grow from USD 127.63 million in 2025 to USD 133.60 million in 2026, and reach USD 170.22 million by 2031, growing at a CAGR of 4.96% from 2026 to 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Hybrid and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Electronics and Electrical, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Sealants Market Trends and Insights

Infrastructure Boom Under Thailand's Eastern Economic Corridor

The EEC attracted USD 60.23 billion of investment applications in 2025, channeling capital into smart estates such as WHA ESIE 5. Data-center shells specify fire-rated joint sealants and cable-penetration firestops, while battery cleanrooms call for ionic-controlled silicone formulations. Thailand FastPass cuts permit times by up to 50%, favoring suppliers that hold local inventory and offer on-site technical service. Framework agreements now dominate procurement, locking in performance specifications early and reducing mid-project substitutions.

Automotive-EV Production Expansion by OEMs

BYD and GAC Aion inaugurated Thai assembly in July 2024, underpinning a national 30@30 target that ties incentives to domestic content. Battery-pack sealing requires silicone and polyurethane chemistries that retain adhesion from -40 °C to +90 °C and meet UL 94 V-0. Covestro's planned acquisition of the Vencorex HDI site in Rayong secures aliphatic isocyanate supply for two-component polyurethane systems. Automated six-axis robots on EV lines demand tight viscosity control, raising quality-system thresholds for local compounders.

Petrochemical Feedstock Volatility Compressing Margins

Naphtha averaged USD 674 per ton in 2024, dipping to USD 607 in H1 2025, yet propylene and PVC remained high, trimming converter gross margins by 200-300 bps. Extended inventories to 120 days, as practiced by TOA Paint, reflect supply-risk hedging. Increased recycled-HDPE use introduces certification costs under ISCC Plus, adding further variability.

Other drivers and restraints analyzed in the detailed report include:

- Urban High-Rise and Condominium Renovations

- Electronics Export Clusters Fueling High-Purity Silicone Demand

- Stricter VOC and Chemical Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone captured 40.50% of the Thailand sealants market in 2025, ruled by electronics clusters that require less than 10 ppm ionic contamination and urban facades that demand UV stability. Hybrid and other resins are advancing at a 6.76% CAGR through 2031 as contractors value +-25% movement and over-paintability. Sika's Hybriflex SMP demonstrates this shift by blending polyurethane toughness with silicone weatherability. Polyurethane systems remain entrenched in EV battery packs, where aliphatic isocyanates sourced from Covestro's soon-to-close Rayong site reduce cure-time variability. Acrylic dominates DIY channels, though household debt curbs discretionary renovations. Epoxies stay niche for Map Ta Phut chemical plants that need strong chemical resistance.

Regulatory and capacity moves reinforce these patterns. Wacker's new specialty-silicones complex in Zhangjiagang and Jincheon lines ratchet purity benchmarks, pressing local mixers to match. Bostik's 46% bio-based hybrid with EC1 PLUS and M1 certification signals the sustainability pivot transforming premium bids. The Thailand Industrial Standards Institute's TIS 1321-2566 enforcement from March 2024 adds adhesion-test hurdles that smaller compounders must outsource, lengthening product-launch cycles.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- Covestro AG

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- ITW Polymers Sealants

- MAPEI S.p.A.

- Meridian Adhesives Group (PAS Bangkok Co.)

- Momentive Performance Materials Inc.

- Pidilite Industries Ltd.

- Plic Firston (Thailand) Co., Ltd.

- SCG Chemicals PCL

- Selic Corp PCL

- Shin-Etsu Chemical Co., Ltd.

- Siam Polyurethane Co., Ltd.

- Sika AG

- Soudal Group

- The Yokohama Rubber Co., Ltd. (Hamatite)

- TOA Paint (Thailand) PCL

- Uniseal Co., Ltd.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure boom under Thailand's Eastern Economic Corridor (EEC) programme

- 4.2.2 Automotive-EV production expansion by OEMs

- 4.2.3 Urban high-rise and condominium renovations demanding premium weather-proofing

- 4.2.4 Electronics export clusters fuelling demand for high-purity silicone sealants

- 4.2.5 DIY-retail surge via e-commerce platforms boosting small-pack acrylic sales

- 4.3 Market Restraints

- 4.3.1 Petrochemical feed-stock price volatility compressing margins

- 4.3.2 Stricter VOC and chemical compliance raising reformulation costs

- 4.3.3 Shortage of certified applicators

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Hybrid and Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electronics and Electrical

- 5.2.5 Healthcare

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 ITW Polymers Sealants

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Meridian Adhesives Group (PAS Bangkok Co.)

- 6.4.11 Momentive Performance Materials Inc.

- 6.4.12 Pidilite Industries Ltd.

- 6.4.13 Plic Firston (Thailand) Co., Ltd.

- 6.4.14 SCG Chemicals PCL

- 6.4.15 Selic Corp PCL

- 6.4.16 Shin-Etsu Chemical Co., Ltd.

- 6.4.17 Siam Polyurethane Co., Ltd.

- 6.4.18 Sika AG

- 6.4.19 Soudal Group

- 6.4.20 The Yokohama Rubber Co., Ltd. (Hamatite)

- 6.4.21 TOA Paint (Thailand) PCL

- 6.4.22 Uniseal Co., Ltd.

- 6.4.23 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment