PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066690

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066690

Singapore Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

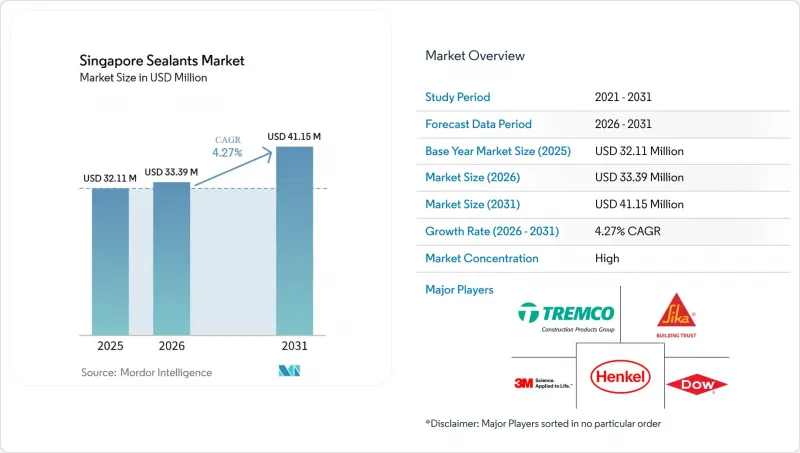

According to Mordor Intelligence, the singapore sealants market size is expected to grow from USD 32.11 million in 2025 to USD 33.39 million in 2026 and is forecast to reach USD 41.15 million by 2031 at 4.27% CAGR over 2026-2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins ) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Sealants Market Trends and Insights

Accelerated Public-Sector Infrastructure Pipeline

Five concurrent rail packages, the Jurong Region Line, Cross Island Line Stage 1, Circle Line Stage 6, Thomson-East Coast Line Stage 5, and Downtown Line Stage 3 East, will introduce dozens of stations that require fire-rated tunnel, platform, and concourse joints, sustaining annual demand for fast-cure, low-shrink silicone, polyurethane, and polysulfide grades. The Urban Redevelopment Authority's Master Plan pledges more than 80,000 new residential units, while Housing and Development Board data lists 127 active projects in early 2026, collectively locking in multi-year sealant volumes. CONQUAS 2025 now ties functional-test results to Temporary Occupation Permit issuance, elevating the premium on products that achieve leak-free glazing and ponding compliance in a single pass. Contractors, therefore, favor formulations with primer-less adhesion and extended movement capability that shorten remediation cycles. Distributors that supply site training and accelerated-cure mock-ups strengthen specification pull-through and repeat orders.

Transition to Green-Certified Building Envelopes

Singapore's Green Mark guidelines emphasize reducing life-cycle carbon footprints and encourage the use of low-emission sealants. These sealants must hold certifications such as GEV EMICODE EC1 PLUS, the Singapore Green Label, or equivalent. Sika's products, Sikaflex Purform and SikaTop-540 Seal, comply with various indoor-air-quality standards, supporting developers in obtaining Leadership in Energy and Environmental Design (LEED) credits. Additionally, these products help developers qualify for Green Mark incentives, including gross floor area benefits. Henkel's new Geneo Science Park lab accelerates perfluoroalkyl-substance-free research and development ahead of anticipated National Environment Agency solvent limits, keeping the firm positioned for early compliance bids. Moisture-cure polyurethanes and hybrid silyl-terminated polymers, which emit negligible isocyanates or aromatics, gain share as workplace exposure limits tighten. Developers increasingly specify two-component epoxy-polyurethane hybrids for below-grade waterproofing because they deliver zero shrinkage and prevent delamination in high water-table sites along reclaimed coasts.

Volatile Silicone Polymer Import Prices Tied to China Supply

Spot premiums for dimethyl carbonate increased, and lead times between Asia and Europe lengthened significantly, driven by China's environmental restrictions on silicon-metal smelters. Singapore, fully import-dependent, saw distributors absorb cost spikes because fixed-price public tenders prevented pass-through. Some shifted to acrylic or hybrid polymers, but substitution risks warranty breaches where high movement or ultraviolet (UV) durability is mandatory. Multinationals with multi-regional sourcing diversified feedstock exposure, while smaller players relied on higher inventory holdings, straining working capital.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor Clean-Room Expansion

- Growing aircraft Maintenance, Repair, and Overhaul (MRO) hub status

- Shrinking Public-Housing Backlog Post-Handover Peak

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone retained 38.50% of the Singapore sealants market share in 2025, owing to superior UV resistance and -40 °C to 100 °C service capability. However, polyurethane's 6.21% CAGR from 2026 to 2031 outpaces the overall Singapore sealants market size as architects specify low-modulus, high-movement products for glass facades and precast concrete joints. SikaHyflex 250 Facade is designed to accommodate significant movement, allowing contractors to widen joints without requiring bond-breaker tape. In humid conditions, where pure silicones often face challenges, hybrid MS-polymers like PENOSIL Facade Joint Hybrid 25LM are highly effective. These polymers adhere well to damp substrates and achieve high emissions standards. Meanwhile, acrylic and butyl mastics continue to be preferred for interior trim and vapor-barrier details, particularly in applications where cost sensitivity is critical, and movement is limited.

The transition from solvent-borne polysulfides to moisture-cure chemistries accelerates under South Coast Air Quality Management District (AQMD) Rule 1124, which bans para-chlorobenzotrifluoride in aerospace sealants by 2028, signaling global supply rationalization that will ripple into Singapore specifications. Producers responding with Product-Weighted Maximum Incremental Reactivity-compliant catalysts highlight a regulatory trend that structurally favors polyurethane and hybrid platforms over legacy polysulfides.

List of Companies Covered in this Report:

- 3M

- Alteco Chemical Pte Ltd.

- Dow

- Fosroc, Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- PFE Technologies Pte Ltd

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated public-sector infrastructure pipeline

- 4.2.2 Transition to green-certified building envelopes

- 4.2.3 Semiconductor clean-room expansion

- 4.2.4 Growing aircraft MRO hub status at Seletar and Changi

- 4.2.5 Government incentives for low-VOC materials

- 4.3 Market Restraints

- 4.3.1 Volatile silicone polymer import prices tied to China supply

- 4.3.2 Shrinking public-housing backlog post-HDB 2025 handover peak

- 4.3.3 Tight migrant-labour quotas raising on-site application costs

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alteco Chemical Pte Ltd.

- 6.4.3 Dow

- 6.4.4 Fosroc, Inc.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 MAPEI S.p.A.

- 6.4.8 PFE Technologies Pte Ltd

- 6.4.9 Shin-Etsu Chemical Co., Ltd.

- 6.4.10 Sika AG

- 6.4.11 Soudal Group

- 6.4.12 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment