PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2060417

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2060417

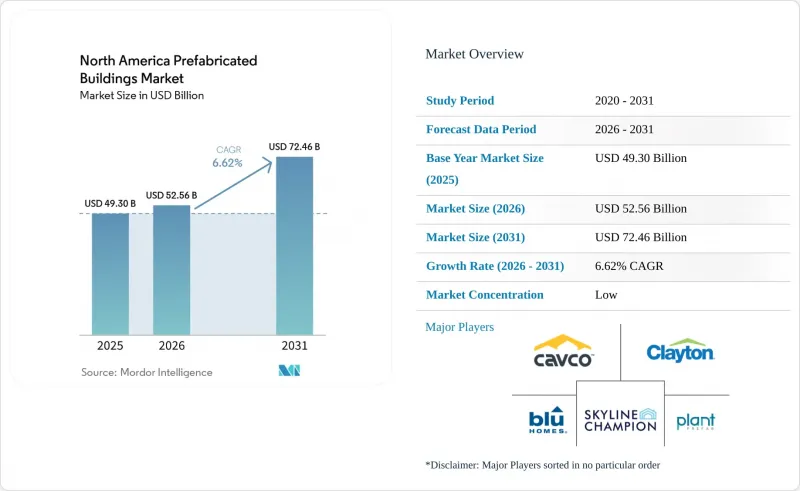

North America Prefabricated Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america prefabricated buildings market size was valued at USD 49.3 billion in 2025 and estimated to grow from USD 52.56 billion in 2026 to reach USD 72.46 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031).The growth trajectory is propelled by persistent labor shortages, accelerating project timelines, and supportive federal programs that reduce financing friction for factory-built housing.

This report is Segmented by Material Type (Concrete, Glass, Metal, Timber, Other Materials), Application (Residential, Commercial, Others), Product Type (Modular Buildings, Panelized & Componentized Systems, Other Prefab Types), and Geography (US, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Prefabricated Buildings Market Trends and Insights

Federal Housing Policy Catalyzes Tribal and Rural Development

Updated Section 184 and Section 502 programs are widening access to capital by lowering guarantee fees and lengthening pilot waivers, directly improving affordability for buyers in low-density regions. Award allocations under the USD 225 million PRICE initiative earmark community-level upgrades that bundle infrastructure with manufactured-home installations, ensuring demand continuity for the North America prefabricated buildings market. As tribal authorities channel the funds into mixed-use developments, manufacturers capture incremental volume while lenders secure federal backstops, reducing credit-risk premiums. The multiplier effect extends to skilled-labor retention, because stable factory employment inside reservations helps stem outward migration of younger cohorts. In turn, companies achieve higher plant utilization rates, cushioning cyclical swings in broader housing starts.

E-commerce Infrastructure Drives Pre-Engineered Building Demand

Fulfillment-center footprints continue to swell as online retail penetration rises. With site selection gravitating toward last-mile nodes and cross-dock hubs, developers favor long-span steel frames, insulated roof panels, and plug-and-play MEP modules to guarantee 18-month delivery targets. Prefabrication compresses critical-path scheduling, enabling tenants to capture holiday-season turnover earlier than conventional builds, strengthening the value proposition inside the North America prefabricated buildings market. Industrial landlords also cite ESG scorecard requirements that reward low-waste assembly and repeatable envelope details. Despite growing plant backlogs, manufacturers mitigate bottlenecks by adopting takt-time production and by staging auxiliary lines in Mexico's border states, trimming over-the-road miles for outbound shipments into the U.S. Sun Belt logistics belt.

Transportation Economics Challenge Volumetric Module Scalability

Permitting, escort vehicles, and structural clearances push transport costs beyond 15% of total installed value for single-lift volumetric units exceeding standard trailer dimensions. The cost curve steepens after 500 miles, prompting manufacturers to cluster plants within megaregions such as Texas's Triangle and the Great Lakes. MMY US's Louisville facility illustrates the strategy, adding 73 jobs and positioning annual output of 500 units within one-day drive times to Midwest metros. Panelized systems-shipped flat within legal load envelopes-circumvent the constraint, explaining their superior 7.62% CAGR inside the North America prefabricated buildings market.

Other drivers and restraints analyzed in the detailed report include:

- Labor Market Disruption Accelerates Off-Site Construction Adoption

- Building Code Evolution Favors Low-Carbon Prefabricated Solutions

- Regulatory Fragmentation Impedes Standardization and Interstate Commerce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Concrete retained 35.42% of the North America prefabricated buildings market size in 2025 due to fire-rating and load-bearing benchmarks crucial for warehouses and data centers. Yet timber is charting a 7.41% CAGR to 2031 on the back of cross-laminated panels and glue-laminated beams that satisfy seismic codes in mid-rise applications. British Columbia, Quebec, and Oregon now sanction mass-timber towers above 12 stories, accelerating order pipelines for engineered-wood suppliers. Forward-looking developers cite 15% lighter foundations and 30% faster enclosure timelines as decisive advantages, driving incremental wins against concrete.

Timber's ascendance also dovetails with embodied-carbon disclosure mandates in public-procurement tenders, giving low-carbon materials a scoring edge. University pilot projects such as Toronto's Academic Wood Tower validate durability and acoustical performance at scale, shrinking insurer hesitation. Meanwhile metal demand remains steady for roof trusses and long-span girders that dominate e-commerce warehouses. Hybrid composite panels integrating glass curtain walls and steel cores address hurricane-zone resilience without compromising factory throughput, serving niche coastal installations within the North America prefabricated buildings market.

List of Companies Covered in this Report:

- Clayton Homes (Berkshire Hathaway)

- Cavco Industries

- Skyline Champion Corporation

- BluHomes

- Plant Prefab

- ICON Technology

- Butler Manufacturing (BlueScope)

- Nucor Building Systems

- Varco Pruden Buildings

- Behlen Building Systems

- ATCO Structures

- NRB Modular Solutions

- Black Diamond Group

- Williams Scotsman (WillScot Mobile Mini)

- Whitley Manufacturing

- Triumph Modular

- Palomar Modular

- Lindal Cedar Homes

- Stillwater Dwellings

- Horizon North Logistics (Dexterra)

- Modular System Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal-level push for modular housing on tribal & rural land (HUD, USDA)

- 4.2.2 Rapid e-commerce warehouse expansion demanding long-span PEBs

- 4.2.3 Skilled-labor shortages lifting off-site construction adoption

- 4.2.4 Net-zero building codes (IECC-2024, ASHRAE-90.1) favor low-carbon prefab

- 4.2.5 Tax-equity financing for factory-built affordable housing projects

- 4.2.6 Coastal climate-resilience programs funding hurricane-rated volumetric units

- 4.3 Market Restraints

- 4.3.1 High logistics cost for over-dimensional volumetric modules

- 4.3.2 Fragmented state & municipal permitting regimes

- 4.3.3 Limited factory throughput for giga-scale data-center demand

- 4.3.4 Consumer perception of lower resale value vs stick-built houses

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Brief on Different Structures Used in the Prefabricated Buildings Industry

- 4.9 Cost Structure Analysis of the Prefabricated Buildings Industry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Concrete

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Timber

- 5.1.5 Other Materials

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Others

- 5.3 By Product Type

- 5.3.1 Modular Buildings

- 5.3.2 Panelized & Componentized Systems

- 5.3.3 Other Prefab Types

- 5.4 By Country

- 5.4.1 US

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Clayton Homes (Berkshire Hathaway)

- 6.4.2 Cavco Industries

- 6.4.3 Skyline Champion Corporation

- 6.4.4 BluHomes

- 6.4.5 Plant Prefab

- 6.4.6 ICON Technology

- 6.4.7 Butler Manufacturing (BlueScope)

- 6.4.8 Nucor Building Systems

- 6.4.9 Varco Pruden Buildings

- 6.4.10 Behlen Building Systems

- 6.4.11 ATCO Structures

- 6.4.12 NRB Modular Solutions

- 6.4.13 Black Diamond Group

- 6.4.14 Williams Scotsman (WillScot Mobile Mini)

- 6.4.15 Whitley Manufacturing

- 6.4.16 Triumph Modular

- 6.4.17 Palomar Modular

- 6.4.18 Lindal Cedar Homes

- 6.4.19 Stillwater Dwellings

- 6.4.20 Horizon North Logistics (Dexterra)

- 6.4.21 Modular System Sp. z o.o.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment