PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066616

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066616

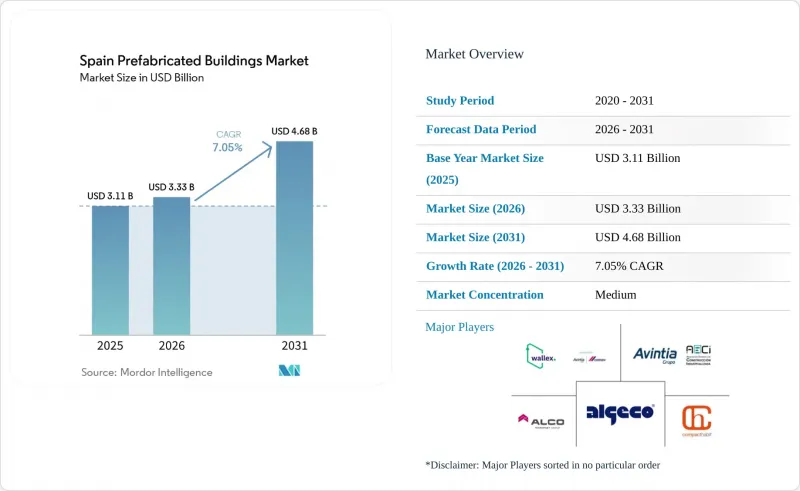

Spain Prefabricated Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spain prefabricated buildings market size in 2026 is estimated at USD 3.33 billion, growing from 2025 value of USD 3.11 billion with 2031 projections showing USD 4.68 billion, growing at 7.05% CAGR over 2026-2031.

This report is Segmented by Material (Concrete, Glass, Metal, Timber, and Other Materials), by Application (Residential, Commercial, and Others), by Product Type (Modular Buildings, Panelized & Componentized Systems, and Other Prefab Types), and Key Cities (Madrid, Barcelona, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Prefabricated Buildings Market Trends and Insights

EU NextGen funds accelerate industrialized housing

The Spain prefabricated buildings market benefits directly from NextGenerationEU grants that channel USD 1.42 billion into factory upgrades, digital twins, and workforce training. Madrid and Valencia lead early pilots that target 20,000 industrialized homes a year by 2035. Manufacturers winning these funds enjoy reduced capital costs, faster type approvals, and priority access to public land. Public-private consortia are standardizing modules that hit EPC-B ratings at scale, lowering risk for lenders and insurers. The result positions Spain as an EU benchmark for industrialized residential delivery.

Mandatory EPC-B retrofits favor modular over-cladding

Royal Decree 390/2021 and the updated Technical Energy Code require EPC-B for both new builds and major retrofits. Modular over-cladding delivers airtight facades without displacing tenants, reducing on-site disruption by 50% compared with traditional scaffolding. Social landlords are bundling retrofit contracts into 10-year energy-performance agreements that reward suppliers able to guarantee kWh savings. These mandates generate predictable, long-run revenue streams and fuel the Spain prefabricated buildings market.

Fragmented municipal codes delay type approval

Spain's 8,000-plus municipalities enjoy wide autonomy over planning and fire codes, forcing suppliers to navigate a maze of local rules. While Madrid and Valencia offer digital one-stop portals, smaller towns still rely on manual checks that can push modular approvals beyond 120 days. SMEs lack the legal resources to track varying requirements, curbing cross-regional scale and slowing the Spain prefabricated buildings market.

Other drivers and restraints analyzed in the detailed report include:

- Labor scarcity pushes off-site productivity

- Tourism-driven rental shortage boosts rapid builds

- Premium land prices squeeze plant-logistics radii

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Concrete accounted for 40.60% of Spain's prefabricated buildings market share in 2025, underpinned by an established supply chain and broad contractor familiarity. Volumetric concrete pods dominate student housing and hotel bathrooms, where fire and acoustic regulations are stringent. Producers such as Eiffage have integrated high-recycled aggregate mixes that cut embodied carbon by 35% compared with 2023 baselines. Timber, led by CLT and glue-lam, records the fastest 7.86% CAGR, driven by carbon reporting mandates and wildfire-resilient rural programs. Public tenders in Catalonia now assign up to 10 quality points for biogenic materials, tipping awards toward timber modules. Metal and glass hybrids serve iconic retail facades, while high-performance insulation panels extend concrete's reach into near-zero-energy buildings.

Timber's growth reshapes factory workflows: automated CNC lines cut panels to millimeter precision, and robotic spray booths apply fire-retardants within minutes. Modular makers pair CLT walls with steel chassis to meet seismic requirements in Granada and Murcia. Insurers offer premium discounts for properly treated timber, a shift from earlier skepticism. Concrete producers respond with ultra-thin UHPC walls that shave 20% off transport weight, defending market share. Such material innovation keeps the Spain prefabricated buildings market agile and responsive to evolving standards.

List of Companies Covered in this Report:

- Algeco Espana

- Grupo Avintia (Avita Industrial)

- Wallex Off-Site (Avintia + Cemex)

- Compact Habit

- Grupo ALCO Modular

- Hormipresa

- Eurocasa Modular

- Cubic House

- KEU Mobile Homes

- EDOMUS

- Modulos ARCO

- Hydrodiseno Pods

- Arquitectura Modular

- Adhorna Prefabricados

- Dinave Paneles

- COFITOR

- Alquibarsa

- CIMBRA Industrializada

- PREFABRI STEEL

- Modular Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU NextGen funds accelerating industrialised-housing uptake

- 4.2.2 Tourism-driven rental shortage boosting rapid-build demand

- 4.2.3 Labour-scarcity pushing off-site productivity gains

- 4.2.4 Mandatory EPC-B retrofit targets favouring modular over-cladding

- 4.2.5 Wild-fire-resilient CLT modules for rural rebuilds (under-reported)

- 4.2.6 On-site crane permit exemptions for flat-pack volumetrics (under-reported)

- 4.3 Market Restraints

- 4.3.1 Fragmented municipal codes delaying type-approval roll-out

- 4.3.2 Premium land prices squeezing plant-logistics radii

- 4.3.3 Perception of prefab as low-quality in high-end coastal zones

- 4.3.4 Shortage of domestic CLT capacity vs booming export demand (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Brief on Different Structures Used in Prefabricated Buildings

- 4.9 Cost Structure Analysis of Prefabricated Buildings

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Concrete

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Timber

- 5.1.5 Other Materials

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Others

- 5.3 By Product Type

- 5.3.1 Modular Buildings

- 5.3.2 Panelized & Componentized Systems

- 5.3.3 Other Prefab Types

- 5.4 By Key Cities

- 5.4.1 Madrid

- 5.4.2 Barcelona

- 5.4.3 Catalonia (ex-Barcelona)

- 5.4.4 Rest of Spain

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Algeco Espana

- 6.3.2 Grupo Avintia (Avita Industrial)

- 6.3.3 Wallex Off-Site (Avintia + Cemex)

- 6.3.4 Compact Habit

- 6.3.5 Grupo ALCO Modular

- 6.3.6 Hormipresa

- 6.3.7 Eurocasa Modular

- 6.3.8 Cubic House

- 6.3.9 KEU Mobile Homes

- 6.3.10 EDOMUS

- 6.3.11 Modulos ARCO

- 6.3.12 Hydrodiseno Pods

- 6.3.13 Arquitectura Modular

- 6.3.14 Adhorna Prefabricados

- 6.3.15 Dinave Paneles

- 6.3.16 COFITOR

- 6.3.17 Alquibarsa

- 6.3.18 CIMBRA Industrializada

- 6.3.19 PREFABRI STEEL

- 6.3.20 Modular Systems

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment