PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061693

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061693

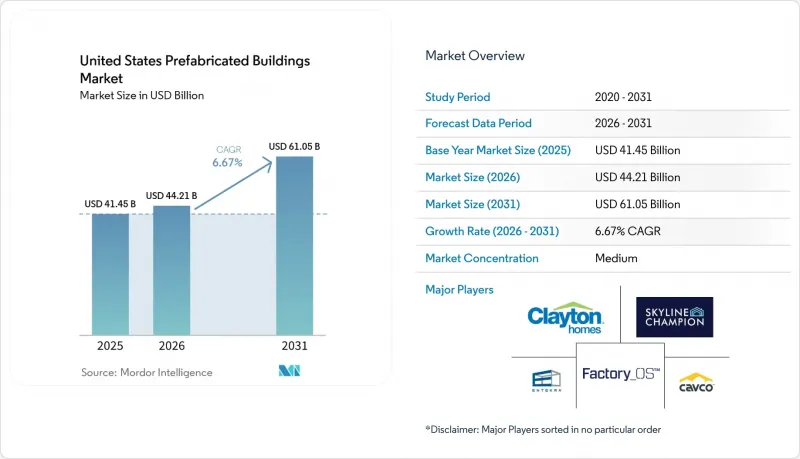

United States Prefabricated Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states prefabricated buildings market size was valued at USD 41.45 billion in 2025 and estimated to grow from USD 44.21 billion in 2026 to reach USD 61.05 billion by 2031, at a CAGR of 6.67% during the forecast period (2026-2031).

This report is Segmented by Material (Concrete, Glass, Metal, Timber, Other Materials), by Application (Residential, Commercial, Others), by Product Type (Modular Buildings, Panelized & Componentized Systems, Other Prefab Types), and by States (Texas, California, Florida, New York, Illinois, Rest of US). The Market Forecasts are Provided in Terms of Value (USD).

United States Prefabricated Buildings Market Trends and Insights

Federal Net-Zero Mandates Accelerate Modular Adoption

Washington's push for 90% fossil-fuel cuts in new federal buildings from fiscal year 2025 sets a clear preference for turnkey envelopes and pre-integrated systems that are easier to deliver in a plant than on a site. Updated General Services Administration standards add embodied-carbon limits, channeling Inflation Reduction Act dollars directly to suppliers able to verify low-emission outputs. Pilot funding under the Green Proving Ground is testing 17 off-site technologies, and results due in 2026 are likely to codify prefabricated solutions as the default for future public work. Together, these measures formalize a pipeline that lifts baseline volumes for modular factories while reducing finance risk for private developers piggybacking on federal specifications.

Rising Labor Shortages Drive Factory-Built Solutions

Contractors enter 2025 needing 439,000 additional workers, with deficits mounting as older tradespeople retire and fewer entrants choose construction careers. Tight labor markets spike overtime premiums and lengthen schedules, so project teams look to assembly-line environments where automation handles repetitive tasks. With construction unemployment at 4.6% and job-opening ratios stubbornly high, factories that require 30% to 50% fewer skilled onsite hours become a hedge against cost overruns. State workforce programs will help, but training pipelines lag present demand, placing the US prefabricated buildings market in a favorable position to capture near-term starts.

Patchwork State Codes Create Interstate Barriers

Fifty sets of modular rules add paperwork and extra inspections when a factory ships a bathroom pod across state lines. Virginia's 2024 adoption of ICC/MBI off-site standards offers a template, but most jurisdictions still enforce unique plan-review protocols that drain time and inflate cost. Lenders and insurers price these frictions into premiums, and some small plants choose to serve only local counties, limiting scale benefits that would otherwise lower unit prices nationwide.

Other drivers and restraints analyzed in the detailed report include:

- Corporate ESG Mandates Favor Low-Waste Construction

- "Made in America" Timber Incentives Strengthen Domestic Supply

- Bank Underwriting Bias Constrains Financing Access

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Timber held a 31.74% US prefabricated buildings market share in 2025, translating to the single-largest material block in dollar terms. Cross-laminated timber and glue-laminated beams now underpin military barracks, higher-education dorms, and mid-rise offices, all helped by federal sourcing preferences that discount domestically produced mass-timber against carbon-intensive steel. The segment's 7.5% CAGR stems from capacity additions in Oregon, Arkansas, and Alabama, where integrated sawmill-to-panel campuses cut logistics miles and embed rural jobs. Modest price declines expected from these new lines should buffer contractors against commodity swings and extend adoption into price-sensitive multifamily projects.

Growth across metals and concrete remains steady, but these incumbents face stiffer embodied-carbon thresholds under updated GSA material rules. Specialized concrete blends employing slag and fly-ash cut emissions and keep the material competitive, while cold-formed steel framing enjoys popularity in hurricane-prone regions. Glass and composites sit in a smaller niche but benefit from ultra-high-performance facades demanded by tech tenants. Regulatory certainty around timber incentivizes architects to pair wood superstructures with hybrid cores, a trend that sustains volume expansion for engineered panels well beyond the forecast window.

List of Companies Covered in this Report:

- Clayton Homes, Inc.

- Skyline Champion Corporation

- Cavco Industries, Inc.

- Cosmic Buildings

- Entekra LLC

- Factory OS

- Blokable

- Plant Prefab

- Prescient Co.

- Guerdon, LLC

- FullStack Modular

- ICON Technology, Inc.

- BMarko Structures

- Turner Construction (Modular Services)

- Whitley Manufacturing

- Nucor Building Systems

- Wikkelhouse USA

- Champion Modular Inc.

- Z Modular (Zekelman Industries)

- Safe & Green Holdings Corp.

- Modular System Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal-level net-zero mandates pulling forward modular demand

- 4.2.2 Rising labour shortages in skilled trades accelerating factory-built adoption

- 4.2.3 Corporate ESG targets favouring low-waste off-site construction

- 4.2.4 Disaster-recovery funding allocating FEMA prefab housing kits

- 4.2.5 VC capital inflow into robotic volumetric factories

- 4.2.6 "Made in America" incentives for domestically sourced mass timber panels

- 4.3 Market Restraints

- 4.3.1 Patchwork state codes limiting interstate module movement

- 4.3.2 Bank underwriting bias against non-traditional collateral

- 4.3.3 Shortfall of heavy lift carriers for oversize coastal shipments

- 4.3.4 Perception gap on long-term resale value of prefab homes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Brief on Different Structures Used in Prefabricated Buildings

- 4.9 Cost Structure Analysis of Prefabricated Buildings

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Concrete

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Timber

- 5.1.5 Other Materials

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Others

- 5.3 By Product Type

- 5.3.1 Modular Buildings

- 5.3.2 Panelized & Componentized Systems

- 5.3.3 Other Prefab Types

- 5.4 By States

- 5.4.1 Texas

- 5.4.2 California

- 5.4.3 Florida

- 5.4.4 New York

- 5.4.5 Illinois

- 5.4.6 Rest of US

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Clayton Homes, Inc.

- 6.4.2 Skyline Champion Corporation

- 6.4.3 Cavco Industries, Inc.

- 6.4.4 Cosmic Buildings

- 6.4.5 Entekra LLC

- 6.4.6 Factory OS

- 6.4.7 Blokable

- 6.4.8 Plant Prefab

- 6.4.9 Prescient Co.

- 6.4.10 Guerdon, LLC

- 6.4.11 FullStack Modular

- 6.4.12 ICON Technology, Inc.

- 6.4.13 BMarko Structures

- 6.4.14 Turner Construction (Modular Services)

- 6.4.15 Whitley Manufacturing

- 6.4.16 Nucor Building Systems

- 6.4.17 Wikkelhouse USA

- 6.4.18 Champion Modular Inc.

- 6.4.19 Z Modular (Zekelman Industries)

- 6.4.20 Safe & Green Holdings Corp.

- 6.4.21 Modular System Sp. z o.o.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment