PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061771

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061771

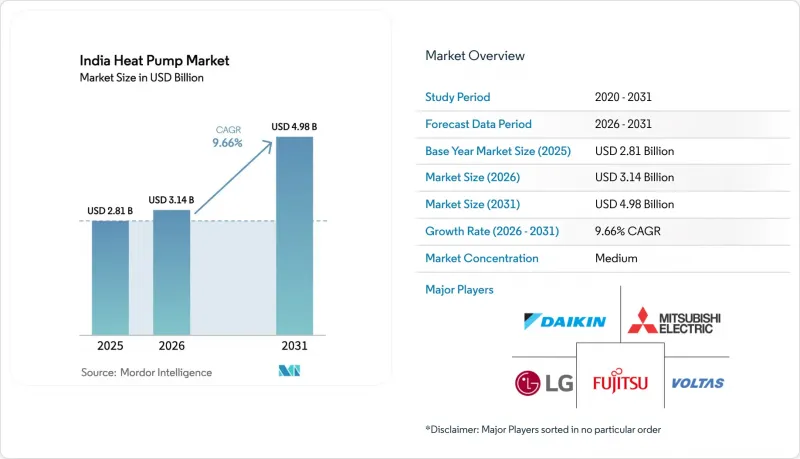

India Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india heat pump market size is expected to increase from USD 2.81 billion in 2025 to USD 3.14 billion in 2026 and reach USD 4.98 billion by 2031, growing at a CAGR of 9.66% over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

India Heat Pump Market Trends and Insights

Implementation of Government Incentives such as PLI Scheme and GST Reductions for Energy-Efficient HVAC

Financial support under the Production Linked Incentive framework lowers component import dependence, giving local compressor and heat-exchanger production a cost edge. The September 2025 Goods and Services Tax cut reduced retail prices by up to 12%, shortening payback periods for first-time residential buyers. Stricter Bureau of Energy Efficiency star-rating norms that took effect in January 2026 raised efficiency thresholds, benefitting firms with strong R&D capability but squeezing smaller assemblers. State policies layer additional incentives: Gujarat offers capital subsidies of up to INR 2 million (USD 0.02 million), while Tamil Nadu mandates district-cooling studies in new urban zones, creating uneven regional uptake. Combined, these measures tilt the India heat pump market toward premium, high-efficiency models that comply with new labeling rules.

Rapid Urbanization, Rising Disposable Income and Residential Construction Boom

India adds roughly 10 million urban residents each year, and housing launches grew 21% in 2024, reinforcing demand for compact, plug-and-play air-to-water units. Per-capita income climbed to INR 185,000 (USD 1,985) in FY 2024, enlarging the middle-class cohort that can finance efficient cooling and hot-water solutions. While dense city plots favor air source systems, marquee geothermal projects at Leh Airport and an Indian Army net-zero facility signal that developers of premium projects are testing ground source designs. Urban consumers value quiet operation and smart-controls integration, nudging brands to bundle Internet of Things features even in sub-10 kW offerings. As a result, the India heat pump market continues to shift from basic comfort appliances toward connected, high-efficiency solutions.

High Upfront Installation Costs and Limited Financing Options

Industrial-grade systems cost INR 1.5-12 million (USD 0.016-0.13 million) depending on capacity, with integration adding up to 30% extra outlay. Drilling 110-120 m boreholes for ground source projects, such as the 457 holes at Leh Airport, can push project budgets beyond the comfort zone of most developers. Banks classify heat pumps as specialized equipment, sidelining them from standard working-capital credit lines, and subsidized loans remain scarce despite pilot programs by Energy Efficiency Services Limited. Payback periods of 18-48 months exceed the 12-month horizon preferred by small manufacturers, delaying broader penetration of the India heat pump market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions

- National Renewable-Energy and Decarbonization Targets Promoting Electrification of Heating

- Shortage of Certified Heat-Pump Installers and Service Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air source systems held 70.31% of the India heat pump market share in 2025 thanks to lower upfront costs and installer familiarity. Water source units cater to niche district-cooling and industrial loops, whereas hybrids provide backup resiliency but dilute decarbonization gains. Ground source units, however, are projected to grow at an 11.31% CAGR, buoyed by fiscal incentives and headline projects like the 2,500 kW Leh Airport installation that drilled 457 boreholes to maintain stable efficiency in sub-zero winters. The technology's ability to operate efficiently at ambient extremes positions it well for institutional buyers across high-altitude and high-heat regions.

While air source products dominate residential retrofits, their coefficient of performance drops 2-3% for every 1 °C rise beyond design conditions, challenging operations when summer peaks top 47 °C in the northern plains. Regulatory water-extraction limits in drought-prone states curb wider use of water source designs. Hybrid setups switch to fossil burners during outages, complicating emissions accounting under the carbon-credit framework. Despite higher drilling expenses, accelerated depreciation under the geothermal policy is persuading airports, defense campuses, and premium real-estate developers to opt for ground source solutions, expanding the strategic canvas of the India heat pump market.

Air-to-water designs captured 62.29% share in 2025 by supplying domestic hot water and hydronic heating from compact packages. Air-to-air variants remain common in retail and office cooling, whereas water-to-water units serve closed-loop industrial processes. Ground-to-water solutions are forecast to expand at an 11.52% CAGR, aided by stable ground temperatures that keep coefficients of performance above 4 while delivering up to 65 °C without backup heat. The India heat pump market is also witnessing a pivot to high-temperature carbon-dioxide systems: Triveni Turbines' 122 °C unit shows a coefficient of performance of 6 for pharmaceutical and food-processing lines.

Residential buyers favor plug-and-play 200-500 L air-to-water cylinders such as Racold's range, priced between INR 199,999 (USD 2,147) and INR 299,000 (USD 3,220), delivering coefficients of performance above 4.4. In contrast, ground-to-water installations like Nagpur Metro Bhavan's 175-ton system cut power demand from 1.6 kW/ton for conventional chillers to 0.6 kW/ton, achieving payback in 4.3 years. Water-to-water retrofits in Gujarat's chemical sector have slashed energy by 38% with 18-month returns, proving that industrial users are ready to adopt once financing hurdles ease. Together, these developments reinforce the upward trajectory of the India heat pump market across diversified technologies.

List of Companies Covered in this Report:

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- NIBE Industrier AB

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- Blue Star Limited

- Voltas Limited

- LG Electronics India Pvt. Ltd.

- Thermia Heat Pumps AB

- Bosch Thermotechnology GmbH

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- Danfoss A/S (Heating Segment)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of Government Incentives Such as PLI Scheme and GST Reductions for Energy-Efficient HVAC

- 4.2.2 Rapid Urbanization, Rising Disposable Income and Residential Construction Boom

- 4.2.3 Increasing Electricity Costs Driving Demand for High-COP Heating and Cooling Solutions

- 4.2.4 National Renewable Energy and Decarbonization Targets Promoting Electrification of Heating

- 4.2.5 Micro-Utility Heat Pump Projects in Smart Cities Creating Demonstration Effect

- 4.2.6 Expansion of Data Centers Requiring Low-PUE Thermal Management Using Process Heat Pumps

- 4.3 Market Restraints

- 4.3.1 High Upfront Installation Costs and Limited Financing Options

- 4.3.2 Shortage of Certified Heat Pump Installers and Service Technicians

- 4.3.3 Grid Congestion Penalties Limiting Large-Scale Heat Pump Adoption in Industrial Clusters

- 4.3.4 Performance Degradation in High-Ambient Dusty Conditions Increasing Maintenance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 NIBE Industrier AB

- 6.4.4 Stiebel Eltron GmbH & Co. KG

- 6.4.5 Vaillant Group

- 6.4.6 Viessmann Climate Solutions SE

- 6.4.7 Glen Dimplex Group

- 6.4.8 Blue Star Limited

- 6.4.9 Voltas Limited

- 6.4.10 LG Electronics India Pvt. Ltd.

- 6.4.11 Thermia Heat Pumps AB

- 6.4.12 Bosch Thermotechnology GmbH

- 6.4.13 Panasonic Heating and Cooling Solutions

- 6.4.14 Fujitsu General Ltd.

- 6.4.15 Carrier Global Corp.

- 6.4.16 Trane Technologies plc

- 6.4.17 Johnson Controls-Hitachi Air Conditioning

- 6.4.18 Danfoss A/S (Heating Segment)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment