PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061778

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061778

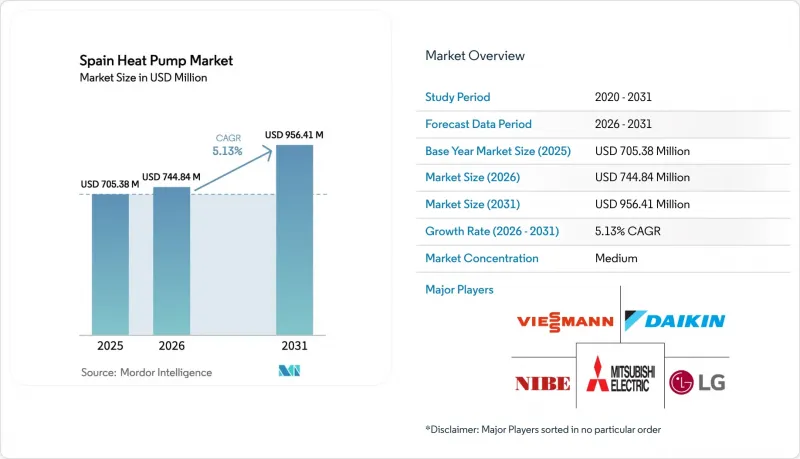

Spain Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spain heat pump market size is expected to increase from USD 705.38 million in 2025 to USD 744.84 million in 2026 and reach USD 956.41 million by 2031, growing at a CAGR of 5.13% over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Spain Heat Pump Market Trends and Insights

Government Incentives and Environmental Subsidies

Spain's tiered funding stack blends national recovery grants with autonomous-community top-ups, delivering household rebates of EUR 3,000-5,000 (USD 3.39-5.65 thousand) and, in Barcelona, project support worth up to EUR 18,800 (USD 21.24 thousand). Catalonia's 40% capital grants and Andalusia's new EUR 61.9 million (USD 69.95 million) thermal-storage line have pulled installer capacity toward high-incentive regions, leaving lower-subsidy provinces underserved. Grant intensity that reaches 75% for public entities under the 2026 RENORED program extends electrification into district energy schemes. While incentives shorten payback periods to as little as five years, they also create regional labor imbalances and accelerate the need for installer upskilling.

EU Green Deal and EPBD Compliance Deadlines

The May 2026 transposition of the recast Energy Performance of Buildings Directive forces developers and owners to lock in zero-emission solutions before fossil boiler bans cascade through regional codes. Buildings rated below class D must be upgraded by 2033, concentrating retrofit activity in Spain's pre-1980 housing stock that lacks insulation or low-temperature radiators. Commercial property owners are pivoting toward air-to-water and hybrid systems to retain eligibility for green finance, a trend reflected in large pre-order backlogs with installers in Madrid and Barcelona.

Skilled Labor Shortage for Installations

Spain must train thousands more technicians to reach its proportional share of the EU-wide 500,000-installer goal by 2030. Current certification pipelines graduate fewer than 8,000 specialists yearly, inflating lead times from four to 12 weeks in major cities. Hydronic retrofits require hydraulic balancing and low-temperature radiator sizing skills rare among crews focused on cooling splits, pushing labor premiums 15-25% higher for complex jobs. Corporate buyers are acquiring installer teams outright to lock in scarce capacity.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity-to-Gas Price Ratio Boosting TCO

- Advancements in Low-GWP Propane-Based Heat Pumps

- High Up-Front Equipment and Retrofit Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid units, though a small base today, are projected to post a 5.49% CAGR and draw on Spain's five-million-unit cooling fleet to minimize incremental investment. They allow operators to retain gas boilers for sparse peak-load hours, delivering 60% emissions cuts without straining winter grid capacity. In contrast, air source equipment dominates the Spain heat pump market with an 84.73% 2025 share, buoyed by benign winter temperatures that support seasonal COP above 3.5.

Hybrid momentum aligns with power-to-gas price spreads and policy uncertainty over near-term grid upgrades. Manufacturers bundle predictive controls that switch fuels dynamically, creating a cost-optimized pathway into full electrification once network reinforcement arrives. The Spain heat pump market therefore shows a bifurcated profile in which pure electrification leads coastal regions, while hybrids anchor northern provinces still wary of cold-spell reliability.

Air-to-water platforms are winning share thanks to their compatibility with underfloor heating and domestic hot water loops required by zero-carbon building codes. Holding 38.31% share in 2025, this cohort is projected to grow at 5.69% CAGR, gradually eroding the air-to-air installed base. Schools, hotels, and hospitals are standardizing on hydronics to secure taxonomy-aligned finance, a trend reinforcing the Spain heat pump market pivot away from cooling-only solutions.

The transition also affects supply chains; compressors and circulators rated for 55-60 °C delivery temperatures face rising demand, and installers retrain on hydraulic balancing. Digital commissioning tools now streamline flow-rate optimization, cutting start-up time by one-third. As such, the Spain heat pump market size allocated to hydronic retrofits is expected to eclipse EUR 300 million (USD 340 million) annually by 2031.

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Fujitsu General Ltd.

- Midea Group Co., Ltd.

- LG Electronics Inc.

- NIBE Industrier AB

- Viessmann Werke GmbH & Co. KG

- Vaillant Group

- Bosch Thermotechnology (Robert Bosch GmbH)

- Stiebel Eltron GmbH & Co. KG

- Carrier Global Corporation

- Trane Technologies plc

- Johnson Controls International plc (York)

- Lennox International Inc.

- Aermec S.p.A.

- Ariston Group

- Clivet S.p.A.

- Hitachi Air Conditioning Europe SAS

- Danfoss A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Incentives and Environmental Subsidies

- 4.2.2 EU Green Deal and EPBD Compliance Deadlines

- 4.2.3 Rising Electricity?to?Gas Price Ratio Boosting TCO

- 4.2.4 Advancements in Low-GWP Propane-Based Heat Pumps

- 4.2.5 Uptake of Hybrid Heat Pumps Leveraging Cooling Base

- 4.2.6 Hospitality Decarbonization Driven by Tourism Boom

- 4.3 Market Restraints

- 4.3.1 Skilled Labor Shortage for Installations

- 4.3.2 High Up-Front Equipment and Retrofit Costs

- 4.3.3 Grid Capacity Limits in Urban Districts

- 4.3.4 Limited Roof/Riser Space in Multi-Family Buildings

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Industry Value Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 Panasonic Corporation

- 6.4.4 Fujitsu General Ltd.

- 6.4.5 Midea Group Co., Ltd.

- 6.4.6 LG Electronics Inc.

- 6.4.7 NIBE Industrier AB

- 6.4.8 Viessmann Werke GmbH & Co. KG

- 6.4.9 Vaillant Group

- 6.4.10 Bosch Thermotechnology (Robert Bosch GmbH)

- 6.4.11 Stiebel Eltron GmbH & Co. KG

- 6.4.12 Carrier Global Corporation

- 6.4.13 Trane Technologies plc

- 6.4.14 Johnson Controls International plc (York)

- 6.4.15 Lennox International Inc.

- 6.4.16 Aermec S.p.A.

- 6.4.17 Ariston Group

- 6.4.18 Clivet S.p.A.

- 6.4.19 Hitachi Air Conditioning Europe SAS

- 6.4.20 Danfoss A/S

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment