PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062305

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062305

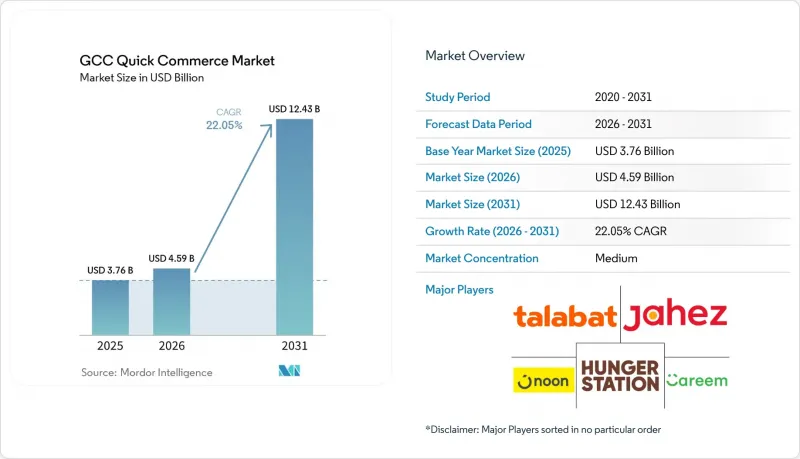

GCC Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gCC quick commerce market size is projected to expand from USD 3.76 billion in 2025 and USD 4.59 billion in 2026 to USD 12.43 billion by 2031, registering a CAGR of 22.05% between 2026 and 2031.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Flowers and Gifts, and More), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and More), and Country (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

GCC Quick Commerce Market Trends and Insights

Surge in Smartphone Penetration and Digital Payments

Mobile use in the Gulf Cooperation Council (GCC) has moved beyond an adoption story and into a condition that supports constant app-based buying. The UAE had 21.9 million active mobile connections by early 2025, and Saudi Arabia had 48.1 million, while smartphone adoption exceeded 95% in both markets. Consumer behavior matched that level of access, with 67% of UAE consumers using mobile devices for their most recent retail purchase in 2025, the highest rate recorded in Visa and PYMNTS Intelligence tracking. For the GCC quick commerce market, this means discovery, checkout, and reorder behavior increasingly happen inside the same device session, which shortens decision time and supports higher order frequency. It also helps the GCC quick commerce market because digital payment habits remove friction from low-ticket and impulse baskets that might otherwise be abandoned. As a result, the GCC quick commerce market benefits from a customer base that is already comfortable with app navigation, stored cards, and repeat digital purchases.

High Disposable Income and Demand for Convenience

Household spending power in the richer GCC markets supports a delivery model built on urgency rather than large planned baskets. Consumers in the UAE, Saudi Arabia, Qatar, and Kuwait are more willing to pay for time savings, which gives fast delivery a daily use case instead of an occasional premium service. The region also has a young urban population profile, and that keeps app-led shopping tied closely to convenience, immediacy, and routine top-up behavior. Climate reinforces this pattern because extreme summer heat makes physical grocery trips less attractive and pushes more replenishment orders into digital channels. That effect is especially visible when households need staples, snacks, beverages, or care products without delaying until a weekly stock-up trip. In practice, the GCC quick commerce market gains from a demand base that values speed, availability, and low-effort ordering as part of normal city life.

High Customer Acquisition Costs Eroding Unit Economics

Customer acquisition remains a core financial pressure point because most major operators are still trying to defend frequency, retention, and visibility at the same time. In large GCC cities, several platforms target the same consumer base, which keeps discounting and loyalty incentives active even when operators want to improve margins. That makes it harder for smaller firms to match delivery fee promotions, free trials, and membership perks without weakening their economics. The strongest response has been a shift toward subscription programs and ecosystem-led retention, where recurring fees can offset part of the pressure from order-level promotions. Even so, the burden falls unevenly across the field, and the GCC quick commerce market increasingly rewards platforms that already have scale and repeat-use households. This is one of the clearest reasons the GCC quick commerce market is consolidating around fewer well-funded ecosystems.

Other drivers and restraints analyzed in the detailed report include:

- Government Investments in Logistics Infrastructure

- Expansion of Dark-Store Networks by Retail Conglomerates

- Regulatory Caps on Delivery Riders' Working Hours

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and staples held 53.48% of the GCC quick commerce market share in 2025, which kept the category at the center of platform traffic and repeat use. This position reflects how closely immediate delivery fits household replenishment for food, beverages, and everyday essentials. Talabat reported that its grocery and retail GMV grew 45% year over year in Q4 2025 and rose from 27% to 32% of total platform GMV, which showed that leading operators were still widening their retail mix rather than defending a fixed grocery base. Fresh produce and dairy, snacks and beverages, and personal care and OTC pharma remain important because each serves a separate mission, with planned restocking, impulse use, and urgent need all feeding order volume. The GCC quick commerce market therefore continues to rely on grocery as the anchor that brings users back often enough for broader cross-category monetization.

Pet care is forecast to grow at a 22.45% CAGR through 2031, making it the fastest product segment in the GCC quick commerce market size outlook. Growth in this category is tied less to a sudden jump in pet ownership and more to a stronger preference for premium food, hygiene, and care products that consumers want replaced quickly when stock runs low. Electronics and accessories also matter because they bring higher basket values and fit urgent replacement or gift-led buying occasions. Flowers and gifts serve a similar event-driven role, especially in business-heavy markets such as Dubai and Doha where professional and social gifting is more frequent. Home and cleaning supplies remain smaller in basket value, but they support steady reordering between larger grocery missions, which helps the GCC quick commerce industry deepen customer retention across routine household needs.

List of Companies Covered in this Report:

- Talabat UAE Company LLC

- HungerStation LLC

- Nana Direct Company

- Careem Networks FZ-LLC

- Noon UAE Grocery Delivery LLC

- Deliveroo Dubai LLC

- Jahez International Company

- Baqala Grocery Delivery Marketplace LLC

- Quiqup Delivery LLC

- elGrocer DMCC

- Amazon Technologies Inc.

- BARQ Fleet IT Company

- Yalla Market Delivery Services LLC

- Rabbit Mart For E-Commerce LLC

- Snoonu Trading and Services W.L.L.

- Send Logistics Pty Ltd

- Meituan Keeta HK Limited

- Fodel Delivery Services FZ-LLC

- iMile Delivery Services LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Smartphone Penetration and Digital Payments

- 4.2.2 High Disposable Income and Demand for Convenience

- 4.2.3 Government Investments in Logistics Infrastructure

- 4.2.4 Expansion of Dark-Store Networks by Retail Conglomerates

- 4.2.5 Integration of High-Temperature Delivery Robots

- 4.2.6 Cross-Border Digital Nomad Inflow Boosting On-Demand Consumption

- 4.3 Market Restraints

- 4.3.1 High Customer Acquisition Costs Eroding Unit Economics

- 4.3.2 Regulatory Caps on Delivery Riders' Working Hours

- 4.3.3 Limited Cold-Chain Capacity for Extreme Heat Deliveries

- 4.3.4 Dependence on Expatriate Labor Vulnerable to Visa Reforms

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

- 5.3 By Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Qatar

- 5.3.4 Kuwait

- 5.3.5 Oman

- 5.3.6 Bahrain

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Talabat UAE Company LLC

- 6.4.2 HungerStation LLC

- 6.4.3 Nana Direct Company

- 6.4.4 Careem Networks FZ-LLC

- 6.4.5 Noon UAE Grocery Delivery LLC

- 6.4.6 Deliveroo Dubai LLC

- 6.4.7 Jahez International Company

- 6.4.8 Baqala Grocery Delivery Marketplace LLC

- 6.4.9 Quiqup Delivery LLC

- 6.4.10 elGrocer DMCC

- 6.4.11 Amazon Technologies Inc.

- 6.4.12 BARQ Fleet IT Company

- 6.4.13 Yalla Market Delivery Services LLC

- 6.4.14 Rabbit Mart For E-Commerce LLC

- 6.4.15 Snoonu Trading and Services W.L.L.

- 6.4.16 Send Logistics Pty Ltd

- 6.4.17 Meituan Keeta HK Limited

- 6.4.18 Fodel Delivery Services FZ-LLC

- 6.4.19 iMile Delivery Services LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment