PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062409

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062409

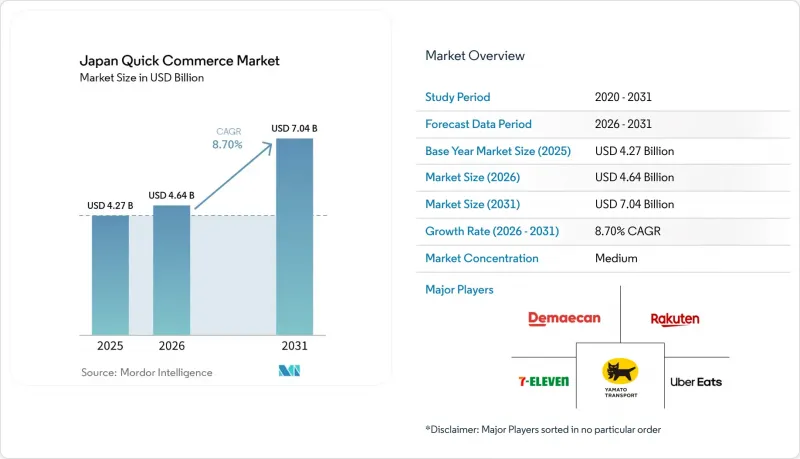

Japan Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan quick commerce market was valued at USD 4.27 billion in 2025 and is forecast to reach USD 7.04 billion by 2031, expanding at a CAGR of 8.70% over the 2026-2031 period.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Pet Care, and Flowers and Gifts), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are Provided in Terms of Value (USD).

Japan Quick Commerce Market Trends and Insights

Shift Toward Convenience-First Purchasing Behavior

Urban households in Japan increasingly use fast delivery for daily needs rather than only for restaurant meals. A February 2026 survey of single-person households in the Tokyo metropolitan area found that 34.5% used delivery services multiple times per month, and daily necessities made up 51.8% of ordered categories while food delivery accounted for 14.1%. That buying pattern matters for the Japan quick commerce market because it favors platforms that can carry bulky, routine, and top-up items with dependable availability instead of only meal orders. METI reported that household expenditure on food, beverages, and alcohol rose 2.6% year over year in 2024 and was 5.7% above 2022 levels, which supports steady replenishment demand in the categories most suited to rapid delivery. Operators that match assortment to top-up grocery, household essentials, and personal care are better placed to capture repeat orders in the Japan quick commerce market than those that treat grocery as an add-on to food delivery.

Rapid Expansion of Dark Stores in Urban Japan

Dark stores are becoming more important in the Japan quick commerce market because speed alone is not enough if stock accuracy is weak. Purpose-built fulfillment sites can hold broader assortments and maintain tighter inventory visibility than a live retail floor, which improves order completion and lowers substitution risk. AEON and Ocado announced a third automated customer fulfillment center in Kuki-Miyashiro, following the first site in Chiba and a second center planned for Hachioji, which shows continued investment in automation-led grocery fulfillment. That build-out supports a model in which labor productivity and pick accuracy improve as volume scales across dense urban catchments. The Japan quick commerce market therefore gives an advantage to operators that secured logistics assets early and can connect fulfillment speed with reliable SKU depth.

High Last-Mile Logistics Cost Per Order

Last-mile economics remain one of the main limits on the Japan quick commerce market. The Japan Institute of Logistics Systems reported that the retail sector logistics cost ratio rose to 6.38% of sales in 2024, the highest level in at least 20 years for that category. The burden is heavier for quick delivery because order values are smaller, pick cycles are shorter, and the service promise leaves less room to spread cost across routes. METI also reported an urban redelivery rate of 11.6% in October 2024, which shows that failed or repeated delivery attempts still add cost in dense areas. This means the Japan quick commerce market rewards operators that can raise route density, improve forecasting, and limit failed handoffs rather than those that compete only on discounting.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Demanding Home Delivery Solutions

- Rising Cashless Payment Adoption Enabling Seamless Checkout

- Intensifying Competition Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and staples held 57.61% of the market in 2025, which made the category the core volume engine of the Japan quick commerce market. That leadership came from repeat purchase behavior rather than premium pricing, because households use fast delivery for top-up missions that happen several times a week. Single-person households and working couples rely on grocery for urgent replenishment, and that steady cadence supports the route density needed to keep fulfillment costs under control. Fresh produce and dairy, snacks and beverages, and home and cleaning supplies all add natural basket extensions that make a grocery-led order more viable for operators.

Electronics and accessories is forecast to grow at a 7.96% CAGR through 2031, which makes it the fastest-rising product category in the Japan quick commerce market. METI reported that household expenditure on home appliances, AV equipment, and computer peripherals rose 3.5% year over year in 2024 and stood 15.7% above 2019 levels. That pattern supports demand for replacement items such as cables, chargers, and small accessories, where delivery speed can matter more than price. METI also showed growth in cosmetics and pharmaceutical spending, which supports adjacent expansion into personal care and OTC products that can lift order value without moving far from the Japan quick commerce industry's daily-need mission.

List of Companies Covered in this Report:

- Rakuten Group, Inc.

- Kuroneko Yamato Logistics Co., Ltd.

- 7-Eleven Japan Co., Ltd.

- Uber Eats Japan, Inc.

- Wolt Enterprises Oy

- Demae-can Co., Ltd.

- Amazon Japan G.K.

- Lawson, Inc.

- Aeon Co., Ltd.

- Seiyu GK

- Mercari, Inc.

- Coca-Cola Bottlers Japan Inc.

- Panasonic Retail Service Co., Ltd.

- Foodpanda Japan K.K.

- Postmates Japan K.K.

- Z Holdings Corporation

- 7NOW Delivery Japan K.K.

- DoorDash Technologies Japan K.K.

- SoftBank Corp. (Quick Commerce Initiatives)

- Ministop Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Convenience-First Purchasing Behavior

- 4.2.2 Rapid Expansion of Dark Stores in Urban Japan

- 4.2.3 Aging Population Demanding Home Delivery Solutions

- 4.2.4 Rising Cashless Payment Adoption Enabling Seamless Check-Out

- 4.2.5 Deployment of Sidewalk Delivery Robots in Pilot Zones

- 4.2.6 Retail Media Monetization Within Quick Commerce Apps

- 4.3 Market Restraints

- 4.3.1 High Last-Mile Logistics Cost Per Order

- 4.3.2 Intensifying Competition Compressing Margins

- 4.3.3 Labor Shortages in Urban Logistics

- 4.3.4 Municipal Restrictions on Micro-Fulfillment Center Zoning

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Rakuten Group, Inc.

- 6.4.2 Kuroneko Yamato Logistics Co., Ltd.

- 6.4.3 7-Eleven Japan Co., Ltd.

- 6.4.4 Uber Eats Japan, Inc.

- 6.4.5 Wolt Enterprises Oy

- 6.4.6 Demae-can Co., Ltd.

- 6.4.7 Amazon Japan G.K.

- 6.4.8 Lawson, Inc.

- 6.4.9 Aeon Co., Ltd.

- 6.4.10 Seiyu GK

- 6.4.11 Mercari, Inc.

- 6.4.12 Coca-Cola Bottlers Japan Inc.

- 6.4.13 Panasonic Retail Service Co., Ltd.

- 6.4.14 Foodpanda Japan K.K.

- 6.4.15 Postmates Japan K.K.

- 6.4.16 Z Holdings Corporation

- 6.4.17 7NOW Delivery Japan K.K.

- 6.4.18 DoorDash Technologies Japan K.K.

- 6.4.19 SoftBank Corp. (Quick Commerce Initiatives)

- 6.4.20 Ministop Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment