PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062412

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062412

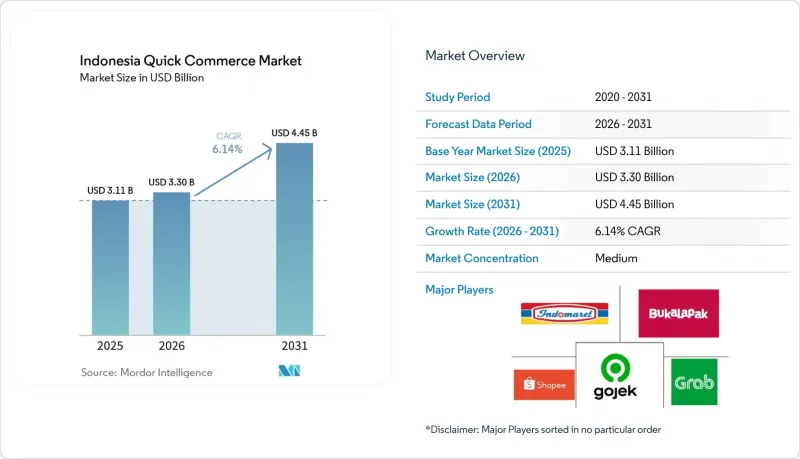

Indonesia Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia quick commerce market size is expected to increase from USD 3.11 billion in 2025 to USD 3.30 billion in 2026 and reach USD 4.45 billion by 2031, growing at a CAGR of 6.14% over 2026-2031.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Quick Commerce Market Trends and Insights

E-Commerce Platforms Integrating 15-Minute Fulfillment Options

The Indonesia quick commerce market is changing because leading super-apps are now placing fast fulfillment inside the main checkout flow instead of treating it as a separate service. Shopee's instant delivery rollout was available in more than 50 cities, and orders using faster delivery options rose by more than 35% year over year in Q3 2025. GrabMart also expanded quickly, with management stating that the business grew 1.7x faster than GrabFood in 2025 and increased its user base by 30% year over year. Grab also stated that users who bought groceries and food within the same ecosystem showed 1.5x higher frequency and 1.5x higher spend, which shows why platform bundling matters in the Indonesia quick commerce market. This changes competition because the main fight is moving toward the app interface, where one wallet, one rider pool, and one cart can lift order values without adding a separate customer acquisition burden. Smaller stand-alone operators therefore have less room to win on breadth and are more likely to focus on narrower needs such as fresh, specialty care, or fast pharmacy delivery.

Accelerated Urban Middle-Class Adoption of Digital Payments

The Indonesia quick commerce market is also benefiting from a payment system that is becoming easier to use at both the consumer and merchant levels. Bank Indonesia reported that QRIS transactions reached 13.66 billion in 2025, and total digital payment transactions rose by 39.2% year over year to 14.26 billion transactions. Bank Indonesia also reported 59.53 million QRIS users and 42.75 million merchants at the end of 2025, with around 90% of those merchants classified as micro, small, and medium enterprises. This wider merchant base gives the Indonesia quick commerce market a denser network for local sourcing, vendor settlement, and repeat neighborhood fulfillment. It also strengthens wallet-led loyalty loops, because consumers who keep payments, rewards, and delivery inside the same app usually reorder faster and with less friction. Bank Indonesia's 2026 payment growth outlook remained strong, with one widely cited estimate pointing to 29.7% growth, which supports further cashless use in the Indonesia quick commerce market.

High Rider Churn Due to Gig-Economy Competition

Rider churn remains one of the clearest operating risks in the Indonesia quick commerce market because service quality depends on rider availability at the exact hour and location where demand spikes. A Kompas Research and Development survey covering 482 drivers across 17 provinces found that 57.5% saw partner status as financially harmful, and 83.6% said revenue-sharing arrangements felt unfair. The same survey also found that many active drivers were thinking about exit, which shows why retention remains unstable even when platform demand is strong. This puts the Indonesia quick commerce market in a difficult position, because higher incentives protect fulfillment levels but weaken margins, while lower incentives reduce cost pressure but raise the risk of late delivery and canceled orders. Indonesia's regulatory approach is also tightening, and the 8% commission cap referenced in discussions around Presidential Regulation No. 27/2026 limits how platforms balance payouts and take rates. Platforms are trying to respond with better dispatch tools, incentive redesign, and seasonal bonuses, but those steps do not fully remove the income instability that drives churn in the Indonesia quick commerce market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Dark Store Networks Across Tier II Cities

- On-Demand Grocery Partnerships with Modern Trade Chains

- Rising Last-Mile Labor Costs from Minimum-Wage Hikes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and staples held 51.72% of the Indonesia quick commerce market share in 2025, which made staple replenishment the clearest repeat-use case for daily ordering. This category remains the core of the Indonesia quick commerce market because households reorder rice, cooking oil, eggs, packaged foods, and other basics more often than discretionary goods. That repeat cycle gives scaled operators better visibility into basket patterns, which helps them place inventory closer to demand and improve rider routing over time. Fresh produce and dairy, snacks and beverages, and personal care and OTC pharma sit in the next operating tier, but each one places a different burden on storage, picking, and compliance. Home and cleaning supplies and electronics and accessories remain smaller within the Indonesia quick commerce market because they are bought less often and usually do not carry the same urgency as food and everyday essentials.

Pet care is projected to expand at a 6.45% CAGR from 2026 to 2031, making it the fastest-growing product line in this part of the Indonesia quick commerce industry. The growth case is tied to rising urban pet ownership, especially among younger households in tier I metros that already use app-based delivery for routine household needs. This creates a useful overlap for the Indonesia quick commerce market, because recurring pet food orders can be bundled with staple baskets and then supported by automatic reminders or subscription-style offers. Flowers and gifts remain smaller in absolute value, but they can produce stronger order values during seasonal peaks such as Lebaran, Christmas, and Valentine's Day. Personal care and OTC pharma also offer growth, but operators that want to scale these categories in the Indonesia quick commerce market need stronger compliance discipline, cleaner sourcing, and tighter storage controls than standard grocery-led models require.

List of Companies Covered in this Report:

- PT GoTo Gojek Tokopedia Tbk

- PT Grab Teknologi Indonesia

- PT Shopee International Indonesia

- PT Bukalapak.com Tbk

- PT Global Digital Niaga Tbk

- PT Icart Group Indonesia

- PT Kreasi Nostra Mandiri

- PT Astro Technologies Indonesia

- PT Sayur Digital Indonesia

- PT Allo Fresh Indonesia

- KitaBeli Pte. Ltd.

- PT Sooplai Indonesia

- PT Arkadia Digital Media Tbk

- PT Indomarco Prismatama

- PT Indomarco Prismatama

- PT Sumber Alfaria Trijaya Tbk

- PT Hero Supermarket Tbk

- PT Matahari Putra Prima Tbk

- PT Social Bella Indonesia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Urban Middle-Class Adoption of Digital Payments

- 4.2.2 Expansion of Dark Store Networks Across Tier II Cities

- 4.2.3 Mobile Data Costs Falling Below IDR 5,000 (USD 0.28)/GB

- 4.2.4 On-Demand Grocery Partnerships with Modern Trade Chains

- 4.2.5 Growing Investor Appetite for Hyperlocal Logistics Start-ups

- 4.2.6 E-commerce Platforms Integrating 15-Minute Fulfillment Options

- 4.3 Market Restraints

- 4.3.1 High Rider Churn Due to Gig-Economy Competition

- 4.3.2 Limited Cold-Chain Infrastructure Outside Java

- 4.3.3 Regulatory Uncertainty on Instant Delivery Traffic in Residential Zones

- 4.3.4 Rising Last-Mile Labor Costs from Minimum-Wage Hikes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PT GoTo Gojek Tokopedia Tbk

- 6.4.2 PT Grab Teknologi Indonesia

- 6.4.3 PT Shopee International Indonesia

- 6.4.4 PT Bukalapak.com Tbk

- 6.4.5 PT Global Digital Niaga Tbk

- 6.4.6 PT Icart Group Indonesia

- 6.4.7 PT Kreasi Nostra Mandiri

- 6.4.8 PT Astro Technologies Indonesia

- 6.4.9 PT Sayur Digital Indonesia

- 6.4.10 PT Allo Fresh Indonesia

- 6.4.11 KitaBeli Pte. Ltd.

- 6.4.12 PT Sooplai Indonesia

- 6.4.13 PT Arkadia Digital Media Tbk

- 6.4.14 PT Indomarco Prismatama

- 6.4.15 PT Indomarco Prismatama

- 6.4.16 PT Sumber Alfaria Trijaya Tbk

- 6.4.17 PT Hero Supermarket Tbk

- 6.4.18 PT Matahari Putra Prima Tbk

- 6.4.19 PT Social Bella Indonesia

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment